- GBP/EUR consolidates around short & long-term averages

- Series of technical supports from 1.1820-1.1752 on charts

- Rallies may meet technical resistances & fade above 1.19

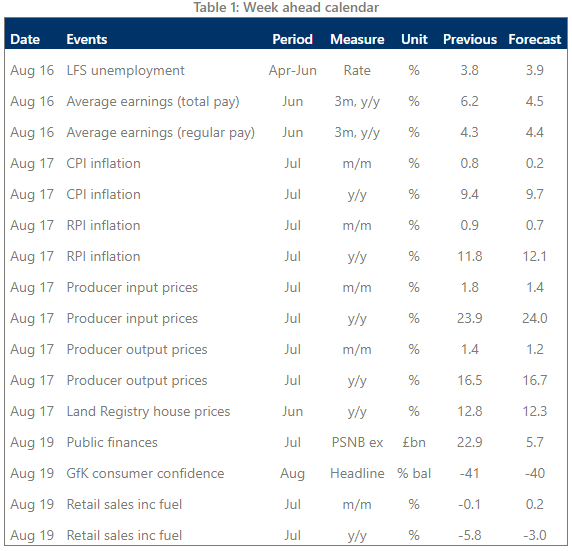

- UK’s jobs & retail data important but July CPI the highlight

- Market's response to an up or down CPI surprise uncertain

Image © Adobe Images

The Pound to Euro exchange rate has hugged its short, medium and long-term averages in recent trade and although this could continue in the days ahead, there is uncertainty over how it would respond to any up or down surprises in July’s inflation numbers due from the UK on Wednesday.

Sterling edged higher against the U.S. Dollar and Swedish Krona last week while falling relative to all other G10 currencies, although it ended the period little changed when compared with the Euro after benefiting when June and second quarter GDP fell less than was expected by the market.

"While today's data painted a slightly better picture of the economy, cracks in the economy are appearing. Consumer facing services flatlined in June – after contracting by 0.3% m-o-m in May. Real government spending is also on the decline," says Sanjay Raja, a senior economist at Deutsche Bank.

Above: Pound to Euro rate shown at hourly intervals with Fibonacci retracements of late July rebound indicating possible areas of technical support for Sterling and selected moving-averages denoting possible shortest-term resistances.

Above: Pound to Euro rate shown at hourly intervals with Fibonacci retracements of late July rebound indicating possible areas of technical support for Sterling and selected moving-averages denoting possible shortest-term resistances.

"The ONS' Monthly Business Survey reported that higher energy and material prices were also starting to hurt manufacturing industries. Moreover, the latest BIC survey noted that a staggering 7% of firms were in the midst of industrial action, which was hampering output. And more worryingly, as of 7 August, the number of firms fully trading was down 2.1pp from its peak on 12 June to 84.8%," Raja wrote in a Friday review of the data.

Friday’s data cast the economy as more resilient than many economists thought it would be in the face of increased business and household energy costs, although if the market found this reason for optimism about the outlook, such optimism could be tested during the week ahead.

“After the weaker than expected CPI print in the US this week, next week the UK, the euro-zone and Canada will release key inflation prints. The euro-zone is a final print so the potential for market moves is greater for the UK and Canada. While US inflation may be peaking, the UK utility cap means a lagged effect and hence higher inflation through until a likely peak in Q4,” says Derek Halpenny, head of research, global markets and international securities at MUFG.

Above: Pound to Euro rate shown at 4-hour intervals with Fibonacci retracements of late July rebound indicating possible areas of technical support for Sterling while selected moving-averages denote various supports and resistances.

Above: Pound to Euro rate shown at 4-hour intervals with Fibonacci retracements of late July rebound indicating possible areas of technical support for Sterling while selected moving-averages denote various supports and resistances.

“In addition, for the UK we will get data on the jobs market and retail sales. More advanced payroll data slowed to just +31k in June matching the gain in January this year which was the weakest since an 8k drop in employment was reported in Feb 2021,” Halpenny also said on Friday.

Employment data will be scrutinised closely on Tuesday for clues about the resilience of the jobs market and trend in wage growth, both of which are influential when it comes to Bank of England (BoE) interest rate policy.

But it’s Wednesday’s inflation figures that will matter most for BoE monetary policy and Pound Sterling in the short-term and this time out there is uncertainty about how the market will be likely to respond to up or downside surprises.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of late July rebound indicating possible areas of technical support for Sterling while selected moving-averages denote various supports and resistances.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of late July rebound indicating possible areas of technical support for Sterling while selected moving-averages denote various supports and resistances.

“UK jobs and CPI inflation data (consensus 9.8% YoY ) could seal a 50bp hike at the 6 Sept BoE meeting, or if weak swing the pricing towards 25bp,” says Chris Weston, chief market analyst at Pepperstone.

“The latter would naturally weaken the GBP – given UK rates markets are already pricing 47bp of hikes for the Sept BoE, and there is a ceiling at 50bp (i.e the BoE won't hike by 75bp),” Weston said on Monday.

Typically, the Pound has responded by rising or falling in the same direction as the data surprise but with the recent trend having placed the BoE in a position where it could have to drive the economy into a recession to bring price pressures under control, such a response is far from assured this week.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of March and June 2016 declines indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of March and June 2016 declines indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

"We expect headline CPI to accelerate further in July to 9.7% y/y, from 9.4% in June, but for core CPI to move sideways at 5.8%, as the sources of inflation move increasingly towards food and energy," says Fabrice Montagne and Abbas Khan, both economists at Barclays.

"Our profile sees July as the peak for headline inflation, while we believe that core CPI already peaked in April at 6.2% (we have seen two consecutive prints of falling core CPI since then). However, this assumes that the ONS takes into account the energy bill rebate support scheme from October in its measurement of inflation," the pair wrote in a Friday look at the week ahead.

Individual economists do differ but the average of forecasts looks for inflation to rise from 9.4% to 9.9% this Wednesday and for core inflation - which ignores things like energy and food prices - to edge higher from 5.8% to 5.9%.

Above: Pound to Euro rate shown at weekly intervals with Fibonacci retracements of September 2020 recovery and selected moving-averages indicating possible areas of technical support for Sterling. Click image for closer inspection.

"With fiscal support likely to be scaled up considerably by the next PM and high income households still holding substantial savings, we think that GDP will flatline through the winter, rather than fall," says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

"If, as we expect, the unemployment rate starts to rise as growth in labour supply exceeds demand, and core CPI inflation trends down, then the MPC will be able to stop hiking with Bank Rate closer to 2% than 3%, even if the economy avoids a recession," Tombs said on Monday.

The economic impact of the BoE's interest rate changes so far is mostly limited to a 'signalling effect' which can be understood as the message that its interest rate decisions send to price setters across the economy including companies, workers and all other types of price bargainers.

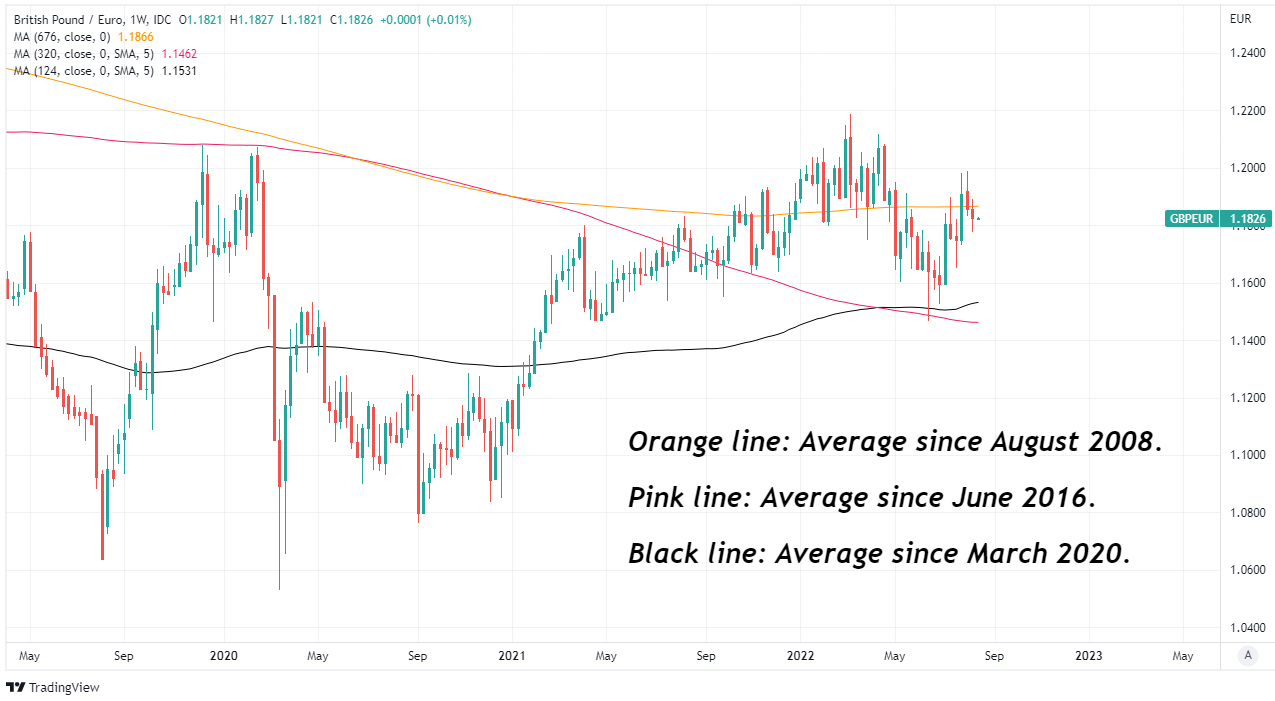

Above: Pound to Euro rate shown at weekly intervals with selected long-term averages. Click image for closer inspection.

But as time goes on increases in Bank Rate can and will have effects that ultimately stifle the economy, and these effects will only grow in size and as a burden for the economy if price setters fail to heed the message embedded in the signal being sent by the BoE as and when it does lift Bank Rate.

Wednesday’s inflation figures are the highlight of the week ahead for the Pound but will be followed on Friday by the release of retail sales numbers for the month of July and these too will also be watched closely for what they might imply about the third quarter economic growth outlook.

“Although anecdotal evidence cited by the ONS suggested the extra public holidays for the Jubilee celebrations in June spurred spending on food, the other major retail sub-sectors all saw sales decline, resulting in total volumes dropping 0.1% m/m,” says Andrew Goodwin, chief UK economist at Oxford Economics.

"However, any boost to sales in July from a return to a full quota of working days will have confronted pressure on households' spending power from rising inflation and record-low consumer confidence. Weighing up these forces, we think retail sales rose 0.2% in July," Goodwin also said on Friday.

Source: Oxford Economics.