- GBP/EUR testing major support on charts

- As broad losses follow BoE policy decision

- Bank Rate lifted to a post-2008 high of 1%

- Pace & scale of further increases uncertain

- Inflation to fall on BoE policy, other factors

© Bank of England

The Pound to Euro rate slumped and was left testing a notable level of technical support on charts after the Bank of England (BoE) appeared to stoke doubt in the market about widely held assumptions relating to its interest rate.

The BoE decided in line with market expectations when it raised Bank Rate to a post-financial crisis high of 1% from 0.75% previously on Thursday, although its accompanying statement and economic forecasts threw in effect a bucket of cold water over Pound Sterling.

“My sense is that the two members’ suggestion that further hikes are not appropriate is resonating,” says Niel Jones, head of FX sales for financial institutions at Mizuho in London.

Thursday’s updated forecasts assumed the BoE would follow the financial market implied path for Bank Rate, which envisages a further increase from 1% to 2.5% by the early morning of 2023, and suggested strongly that taking this path would lead inflation to fall back substantially.

Forecasts modeled on the market's assumed pathway for interest rates had inflation sliding to 1.3% by the end of the BoE’s multi-year forecast horizon, and a level that is meaningfully below the bank’s two percent target.

Pound Sterling slumped broadly in the wake of the decision while UK government borrowing costs tumbled in what was a double barrelled indication that investors and traders either no longer believe Bank Rate would eventually be lifted to 2.5%, or that they increasingly doubt such levels are sustainable.

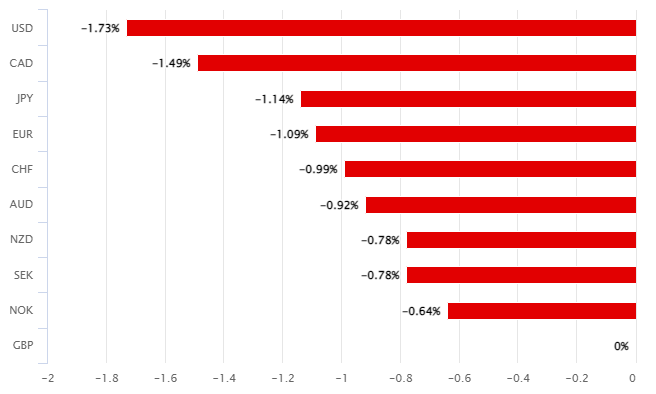

Above: Pound Sterling Vs G10 counterparts on Thursday. Source: Pound Sterling Live.

“With monetary policy acting to ensure that longer-term inflation expectations are anchored at the 2% target, upward pressure on CPI inflation is expected to dissipate over time. Global commodity prices are assumed to rise no further in the central projection, global bottlenecks ease over time, and the weakening in demand growth and building excess supply lead domestic inflationary pressures to subside,” the BoE’s statement says.

“Conditioned on the rising market-implied path for Bank Rate and the MPC’s current forecasting convention for future energy prices, CPI inflation is projected to fall to a little above the 2% target in two years’ time, largely reflecting the waning influence of external factors, and to 1.3% in three years, well below the target and mainly reflecting weaker domestic pressures,” it adds.

Minutes of the May Monetary Policy Committee meeting suggest it’s more likely that financial markets doubted on Thursday that Bank Rate would eventually reach 2.5%, given that they reveal “some members“ felt it “was not appropriate at this juncture” to entertain such a path for Bank Rate.

Thursday’s decision from the BoE is a response to inflation that has surged in recent months, taking it to 7% in March, and the risk of above-target inflation pressures becoming entrenched over the medium and longer-term.

“Based on their updated assessment of the economic outlook, most members of the Committee judged that some degree of further tightening in monetary policy might still be appropriate in the coming months. There were risks on both sides of that judgement and a range of views among these members on the balance of risks,” minutes of the May policy meeting state.

Above: Pound to Euro exchange rate at daily intervals with Fibonacci retracements of April 2021 uptrend indicating possible areas of short and medium-term technical support for Sterling and resistance for the Euro. Click image for closer inspection.

Above: Pound to Euro exchange rate at daily intervals with Fibonacci retracements of April 2021 uptrend indicating possible areas of short and medium-term technical support for Sterling and resistance for the Euro. Click image for closer inspection.

“Some members of the Committee judged that the risks around activity and inflation over the policy horizon were more evenly balanced and that such guidance was not appropriate at this juncture. The MPC would continue to review developments in the light of incoming data and their implications for medium-term inflation,” the meeting record subsequently stated.

The BoE’s signals of caution and hesitancy when it comes to the outlook for Bank Rate are rooted in concerns about how the UK economy will fare as it contends with the present day effects of extraordinarily elevated levels of inflation including the resulting fall in the real value of household incomes.

Falling incomes are most poignantly illustrated by the reduction of purchasing power that has followed the increases in energy and food costs seen during recent months, and especially in the wake of Russia’s invasion of Ukraine.

“The MPC’s remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework also recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. The economy has recently been subject to a succession of very large shocks. Russia’s invasion of Ukraine is another such shock,” the BoE said on Thursday.

“In particular, should recent movements prove persistent as the central projections assume, the very elevated levels of global energy and tradable goods prices, of which the United Kingdom is a net importer, will necessarily weigh further on most UK households’ real incomes and many UK companies’ profit margins. This is something monetary policy is unable to prevent,” the BoE added in the statement announcing its policy decision.

Above: Pound to Euro exchange rate at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible areas of medium and long-term technical support for Sterling and resistance for the Euro. Includes selected weekly moving-averages. Click image for closer inspection.

Above: Pound to Euro exchange rate at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible areas of medium and long-term technical support for Sterling and resistance for the Euro. Includes selected weekly moving-averages. Click image for closer inspection.