- GBP/EUR vulnerable to more resilient Euro

- BoE decision also a possible downside risk

- If MPC caution grows over Ukraine conflict

- GBP/EUR could slip near to 1.18 or below

- Any Russia-Ukraine turbulence supportive

Image © Adobe Images

The Pound to Euro exchange rate reversed much of its early-March gain last week but its corrective setback could extend toward 1.18 this week if Russia's war on Ukraine leads the Bank of England (BoE) to signal on Thursday that it could be more cautious about lifting interest rates going forward.

Pound Sterling rose against only the safe-haven Japanese Yen and Swiss Franc last week while ceding ground to European counterparts in price action that left it among the bigger fallers within the G10 contingent of major currencies for a third week running.

European currencies were bought widely in a global market rally that many analysts attributed to an optimistic view that talks between Ukrainian and Russian representatives would soon create scope for an end to the invasion of Ukraine.

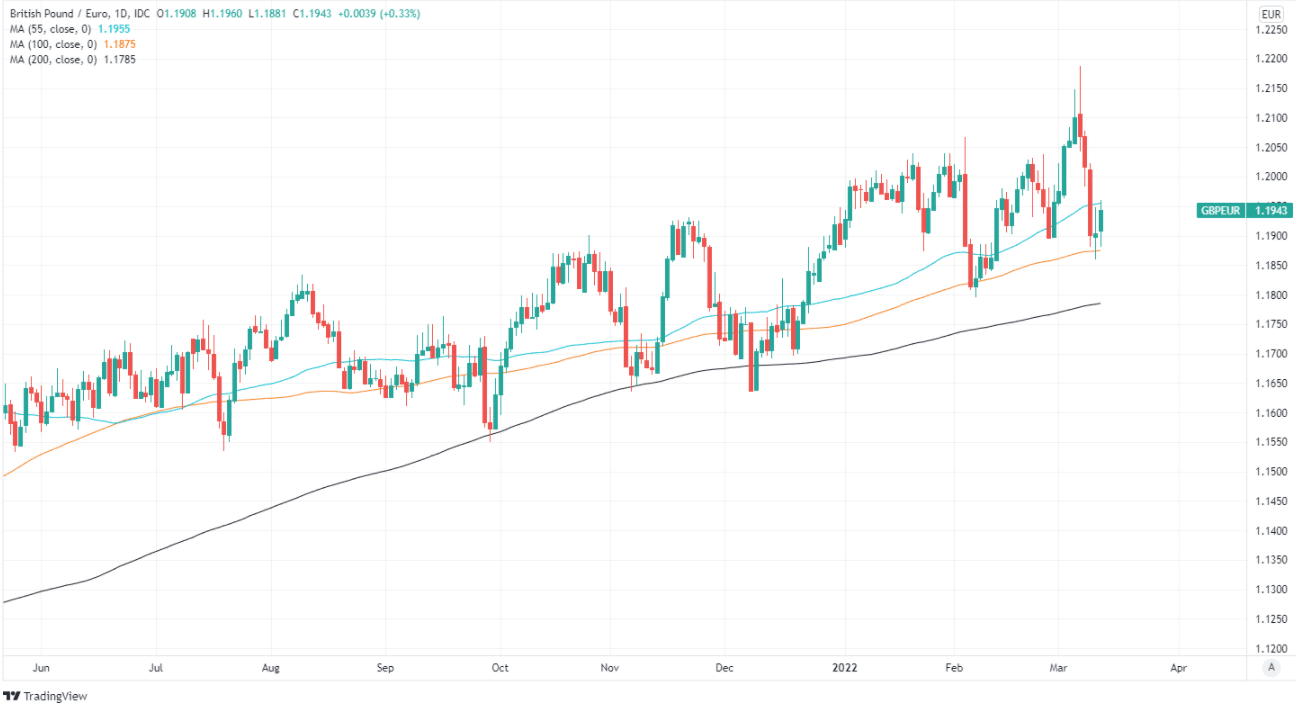

Sterling-Euro fell from a Monday high of 1.2190 before closing near 1.19 on Friday, marking a substantial reversal of gains made in the prior week when Russia’s intensifying attack on Ukraine placed all continental European currencies under significant pressure.

“Is the prospect of further increases in Bank Rate helping to support the GBP to an extent? Yes. If the BoE were to pause its tightening cycle while other central banks proceed with their own tightening, the GBP will depreciate,” says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

Above: Pound to Euro exchange rate shown at daily intervals. Click image for closer inspection.

- Reference rates at publication:

GBP to EUR: 1.1924 - High street bank rates (indicative): 1.1590 - 1.1607

- Payment specialist rates (indicative): 1.1841 - 1.1890

- Find out more about specialist rates and service, here

- Set up an exchange rate alert, here

The rub for Sterling this week is that Thursday’s BoE decision could potentially encourage the nascent retreat if uncertainty about the economic impact of the war in Ukraine leads the BoE to stoke doubt among investors and traders about their expectations of when and where Bank Rate could be likely to rise to over the coming months.

The BoE is widely expected to lift Bank Rate from 0.5% to 0.75% on Thursday in what would be its third increase since December, but pricing in the overnight-indexed-swap market indicates that investors and traders are anticipating it will rise to 2% by year-end.

“I was just going to repeat the words that we used in the monetary policy statement, which is that further modest tightening is likely to be appropriate in the coming months. That’s the position,” Governor Andrew Bailey told the Treasury Select Committee in a late February parliamentary hearing.

“I said in the press conference when we issued the report, and I would just repeat those words. You know, it is a message to markets not to get carried away and I mean, it’s the same message that Dave Ramsden gave in his speech yesterday,” the Governor added.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Even before the Russian military crossed into Ukraine in late February, BoE Governor Andrew Bailey had warned markets “not to get carried away” with their expectations for interest rates, although since those February 23 remarks and Russia's first move into Ukraine the market-implied expectations for Bank Rate at year-end have risen further from 1.80% to 1.99%.

"It's not clear at this stage if those recent developments have any effects on the outlook for inflation two and three years out," Monetary Policy Committee member Michael Saunders was quoted saying at the University of East Anglia on March 01.

This could all mean there's a chance - if not a likelihood - that Thursday’s statement would rebuke the market's latest assumptions or perhaps even signal that the BoE intends to sit on its hands for a few months so that it can observe how the economy contends with the fallout from events in Ukraine and the interest rate rises announced thus far.

"Q1 GDP looks set to increase by nearly 1% quarter-on-quarter, not merely hold steady, as the MPC anticipated last month. CPI inflation in January also overshot the MPC's 5.4% forecast by 0.1pp. What's more, CPI inflation now looks set to rise to 8.7% in April, well above the 7.3% rate forecast by the MPC last month, in response to the recent surge in energy prices," says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

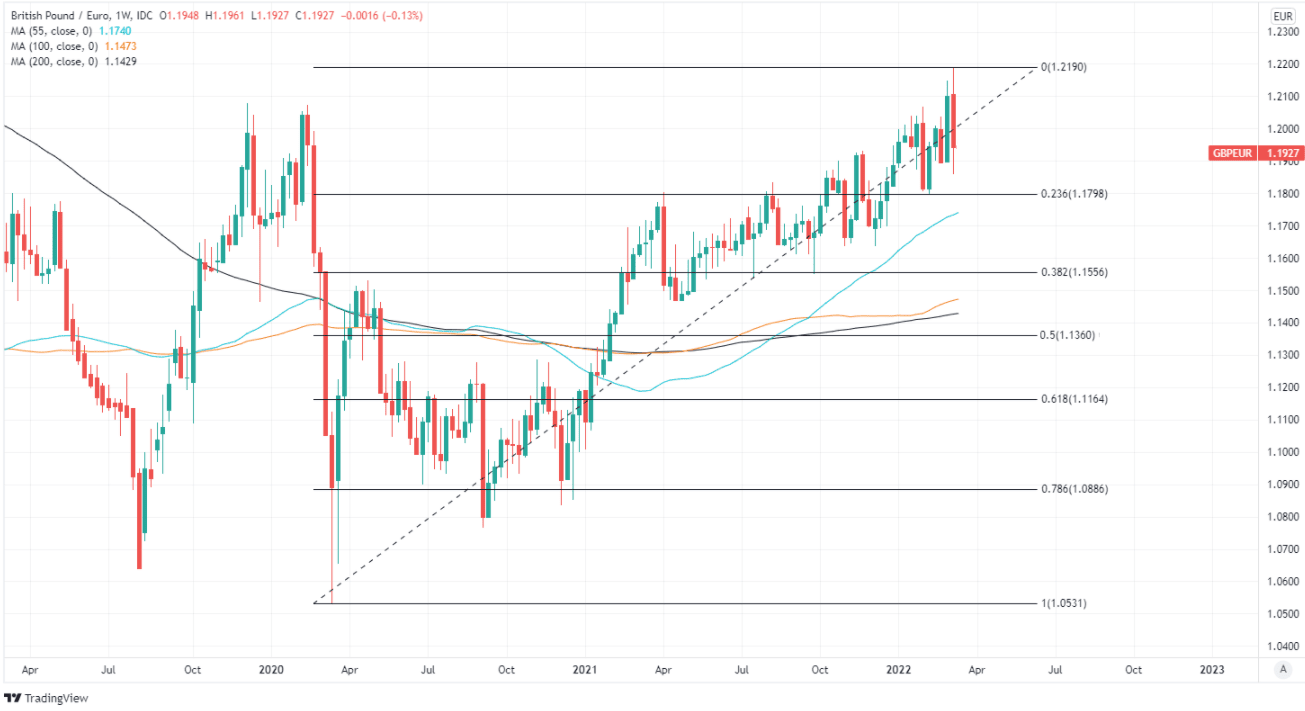

Above: Pound to Euro exchange rate at weekly intervals with Fibonacci retracements of 2020 recovery indicating possible areas of medium-term support. Selected moving-averages also denote possible areas of support. Click image for closer inspection.

"As a result, it is a safe bet to assume that the MPC will raise BankRate by 25bp, to 0.75%. But we think the economy’s sluggishness from Q2 likely will persuade the MPC to refrain from raising Bank Rate further in the second half of this year, after increasing it to 1.00% in May," Tombs and colleagues wrote in a Friday research briefing

When testifying in parliament on February 23 Governor Bailey reiterated a view already expressed in last month's Monetary Policy Report press conference, which was that it could soon make sense for the BoE to pause its cycle of interest rate rises for a period of time in order for the Monetary Policy Committee to observe the economy’ response to the steps it has taken so far.

To the extent that Thursday’s statement suggests this is the approach the BoE will take, it could leave the Pound to Euro exchange rate at risk of a further setback in the short-term, and especially if continental European currencies continue to stabilise in the wake of the steep losses sustained at the onset of Russia’s invasion of Ukraine.

“We think GBPUSD and EURGBP will be sensitive to any meaningful shifts in the outlook for BoE rate hikes. Markets are currently pricing in 5+ hikes over the coming 6m. The worrying growth and inflation backdrop reveals downside risks to that outlook,” says Mark McCormick, global head of FX strategy at TD Securities, who recently advocated that clients sell the Pound-Euro rate.