Image © Adobe Stock

- GBP/EUR spot at publication: 1.1434

- Bank transfer rates (indicative guide): 1.1130-1.1214

- FX transfer specialist rates (indicative): 1.1250-1.1350

- More information on accessing specialist rates, here

The British Pound has rallied in value after the Bank of England said there would be no chance of another cut to interest rates in the near-term and a strong economic recovery would soon take hold in the UK, thanks to the country's vaccination programme.

By removing the shadow of negative interest rates from the horizon the Bank of England has triggered an appreciation in the value of Sterling, cementing the currency's 2021 trend higher against all its major rivals.

The Bank did however lower near-term economic forecasts owing to the strict third national lockdown that was called in January, but this move was compensated by a cheery outlook for the second half of the year at which point a vaccine-lead economic rebound is expected to take hold.

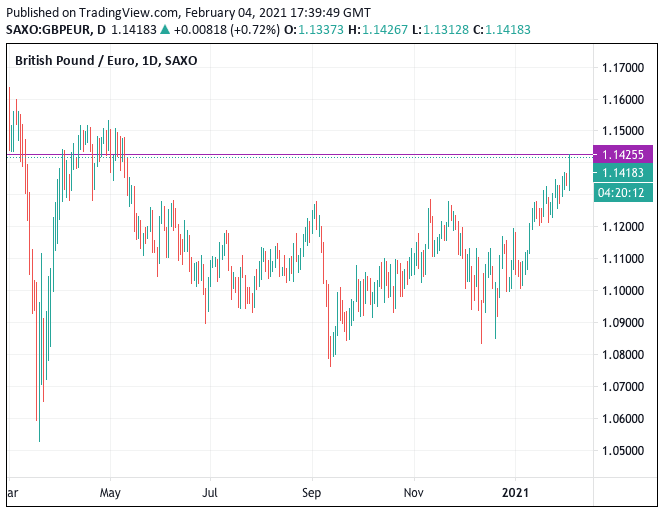

The Pound-to-Euro exchange rate rose steadily in the wake of the 12PM decision from Threadneedle Street, notching up a fresh eight-month best at 1.1443 on Friday.

"Sterling rose to its highest level since last spring against the euro following the BoE update," says Rhys Herbert, an economist at Lloyds Bank.

"Sterling is rising farther here against the single currency in the wake of the BoE meeting, an extension of the recent move," says John Hardy, an analyst at Saxo Bank.

Hardy says the move could open the door to the 1.1627-1.1765 range for the Pound-Euro rate "in the weeks to come".

Hardy says Euro exchange rates are meanwhile liable to stay on the back foot owing to the negative interest rates on offer at the European Central Bank, confirming a real gap in interest rate differentials between the UK and Eurozone is building.

The Bank of England said that while it is not yet willing to cut interest rates to 0% or below, such an outcome could yet happen in the future and such a move is in fact part of their toolkit.

Should the post-pandemic bounce back in economic activity fail to transpire, the Bank would perceivably cut interest rates and boost quantitative easing once more.

As soon as the market starts anticipating such a move the British Pound would be liable to reverse its recent gains, leading to a loss of purchasing power for those looking to buy foreign currencies.

But this appears to be a diminishing risk for now given the Bank of England in fact communicated that it had instructed staff members to work on guidance about the appropriate strategy for tightening monetary policy.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The discussion therefore suggests the next move could in fact be higher rates as opposed to lower rates, an undoubtedly bullish development for Sterling in a world where central banks are trying desperately hard to quell expectations for higher future rates.

The relationship between economic fortunes, the Bank of England, interest rates and exchange rates emphasises just how important the UK's vaccination programme will be going forward.

"The UK may have the luxury of a quicker opening up on its more aggressive vaccine roll-out and a more rapid bounce-back in economic activity on post-Brexit capital inflows and fiscal stimulus," says Hardy.

For now the UK remains a leader in the global vaccination rate, with only Israel having vaccinated a greater proportion of its population.

From a Pound-Euro perspective, the UK has now vaccinated 15% of its population, against the Eurozone's key economies of Germany (3.2%), France (2.63%) and Italy (3.5%).

"Subject to the relaxation of restrictions over the summer, the potential for currently latent forces to propel a strong recovery should see a quiet 2021 for monetary policy. On negative rates, while the BoE judges these are a practical option, they are unlikely to be needed by the time preparations are complete," says Martin Beck, an economist at Oxford Economics.

A central assumption at the Bank of England is that UK economic growth will be fuelled by a complete relaxing of covid-related restrictions by the third quarter of 2021 owing to the UK’s relatively swift pace of vaccinations.