Image © Adobe Images

- GBP/EUR showing both positive and negative signs

- Possibility of a sideways trend evolving

- Pound to be moved by Brexit sentinent, BOE, PMIs

- Euro to take cue from GDP data

Pound Sterling will start the new week trading at around €1.1107 at the start of the new week, after completing 12 weeks of successive losses: the broader trend is certainly a negative one.

Studies of the charts suggest the pair could either go higher or lower in the coming days, with a possible resolution to the mixed outlook lying in the evolution of a sideways trend.

However, we are wary that weekend reports that suggest the UK government is doubling-down on preparations for a 'no deal' Brexit could send the currency lower when markets open.

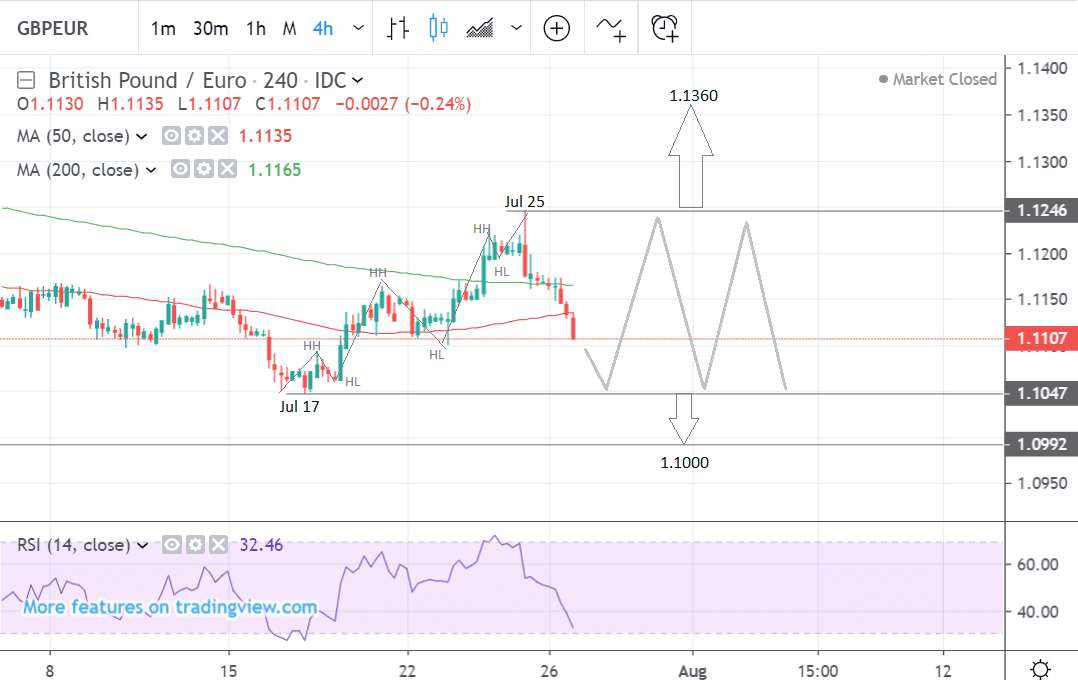

Looking at the technical indicators first, we see the 4-hour chart - used to determine the short-term outlook, which includes the coming week or next 5 days - shows how the pair bounced substantially higher after bottoming at the 17 July lows, 10 days ago.

After peaking at the 25 July 1.1245 highs the pair then rolled over and fell back down, ending the week at 1.1107.

The decline since the highs of the 25th has been steep and accompanied by a sharp fall in momentum which is indicative of more downside still to come, so there is a chance it could continue all the way down to the 1.1048 lows and then perhaps even the longer-term range lows at 1.1000.

This would also be in line with the longer-term downtrend.

Equally, however, the July 17 bounce has established three sets of higher highs (HH) and higher lows (HL), which is a sign a new uptrend may have started, and given the old adage ‘the trend is your friend’, it will probably extend higher.

For confirmation of more upside, a break above the 1.1245 highs would be required. Such a break would probably lead to a continuation of the uptrend to a target at 1.1360.

Alternatively, a break below the July 17 lows at 1.1048 would signal a probable continuation down to the 1.1000-1.0990 range lows.

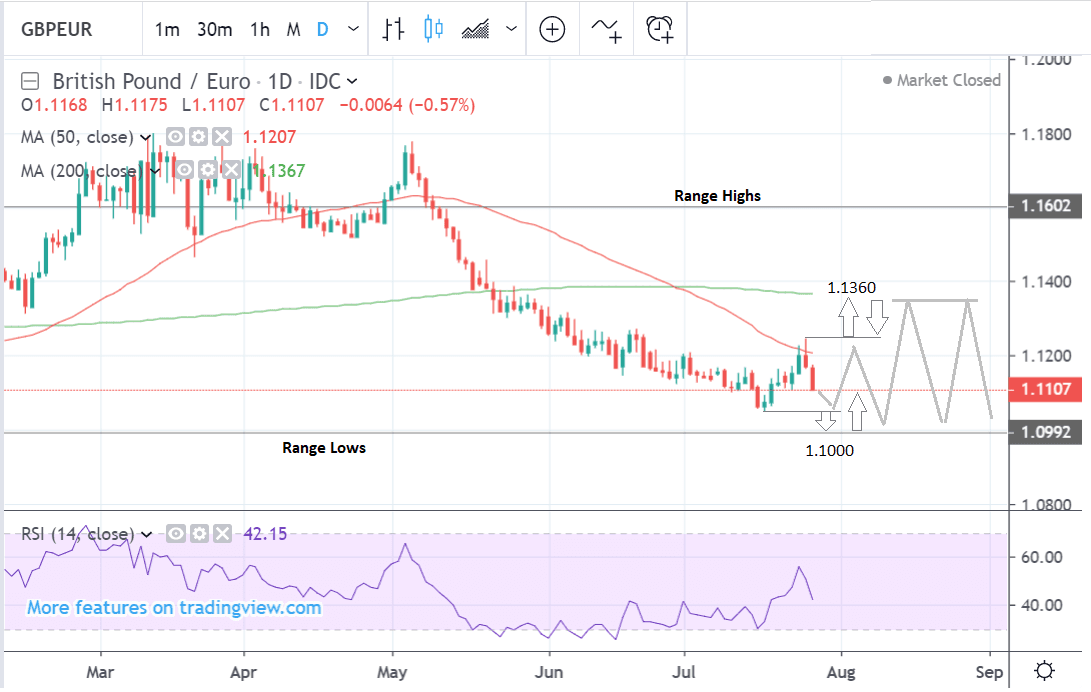

The daily chart - used to analyse the outlook in the medium-term which is defined as the next week to a month - shows the pair in a long-term downtrend.

The pair bounced at the July 17 lows and rose up to peak on July 25 when it connected with the 50-day Moving Average (MA) - then after that, it fell in two quite bearish bars.

Much like the 4-hr chart we see a possible continuation either higher, lower, or sideways. A range-bound market would probably trade between a 1.1360 ceiling at the level of the 200-day moving average (MA) and a floor at 1.1000.

We do not see a strong chance of a breakout from this range in the medium term as Sterling’s main drivers relating to Brexit will be largely absent during the summer recess when Parliament is on holiday.

The Euro may drive volatility but it looks unlikely during the quiet summer too.

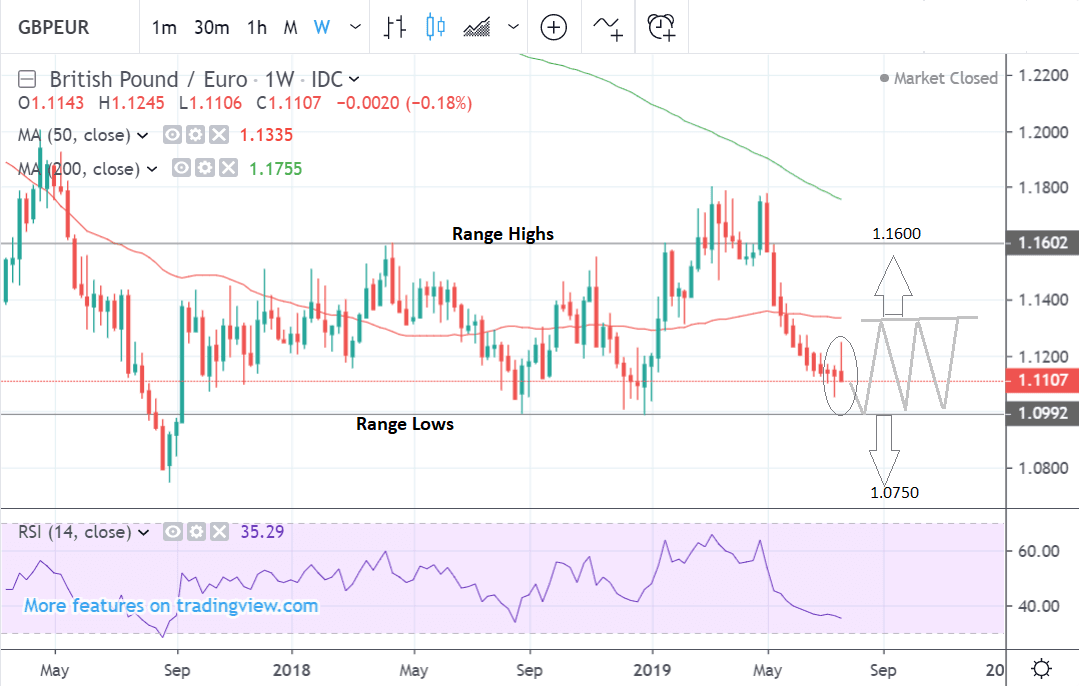

The weekly chart - used to analyse the long-term trend, defined as the next several months of market action - shows the pair trading in a multi-year range.

Given the political risks associated with Brexit over the long-term, there is a chance the pair could break out of this range, especially to the downside given how close it is to the range lows at 1.1000.

A break below 1.0950 would probably confirm a breakout and result in a decline to 1.0750 initially at the September 2017 lows.

Alternatively, there is a chance the pair could rise up within the range and retouch the 1.1600 in the next few months if Brexit risks ease.

A further high probability alternative is that the situation remains uncertain in which case the exchange rate could continue going sideways in the lower half of the range.

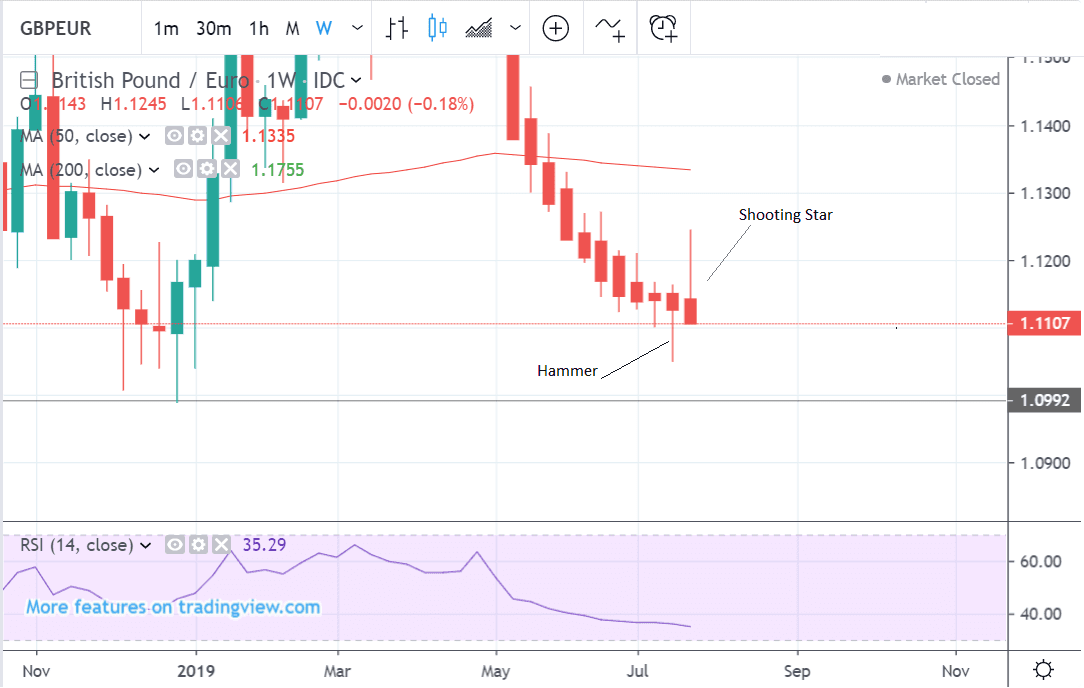

Another thing to note on the weekly chart is how the last two weeks have posted contrary candlestick patterns (circled): the week before last, for example, formed a hammer candlestick which is bullish, and although the price did indeed rise after the hammer, on the following week it formed a bearish shooting star candlestick. For us this symbolises the mixed short-term outlook.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The Pound: Brexit Headlines, Bank of England

Brexit sentiment is easily the most important driver of the Pound at present, and weekend headlines are unsupportive of the currency we belief.

Media reports suggest Prime Minister Boris Johnson has fully committed to a 'no deal' Brexit "by any means necessary".

The Sunday Times reports Johnson has set up a “war cabinet” to deliver Brexit “by any means necessary” by October 31 as a senior cabinet minister warned that there was “now a very real prospect” of no deal.

While markets have ramped up expectations for a 'no deal' Brexit since May, it is likely that there is further 'no deal' risk sentiment to be absorbed and therefore Sterling has the propensity to move lower and trigger fresh multi-month lows.

"Though we still see the risk of a no-deal Brexit at a fairly moderate 20%, we are bearish on Sterling over the short-term amid the expectation that Mr Johnson’s rhetoric towards the EU will remain belligerent and perhaps harden further still in the run-up to 31 October," says George Brown, an analyst at Investec.

On the calendar, the main event for the Pound next week is the Bank of England (BOE) rate meeting, since the BOE sets interest rates which are tier 1 driver of the Pound, however, in reality this may not be the case. Brexit uncertainty has paralysed the BOE and until it is resolved they are highly unlikely to take any action and all their guidance will be conditional on ‘a smooth Brexit’.

The current stance is still marginally hawkish due to upbeat wage growth and this sets the BOE apart from most of its G10 peers, with the exception of the bank of Canada. This should translate into pent up upside potential for the Pound should the UK achieve a managed Brexit.

However, as anyone who has been following developments in the new Boris Johnson administration this is far from certain. Johnson has gathered what looks increasingly like a ‘war cabinet’ of Brexiteer ministers who might be prepared to take the UK out of the EU with a 'no deal' Brexit on October 31.

“The Bank of England (BOE) continued to show a bias towards eventual tightening at its June meeting. This tightening is contingent on an eventual smooth exit from the European Union, however, an effort that has at times looked increasingly like a quixotic journey,” says Wells Fargo in a preview note on the meeting. “Inflation data have been stronger in the U.K. than in Europe, and according to the last statement “growth in unit wage costs has remained at target consistent levels.” “The U.K. economy has looked a bit more wobbly of late, particularly the manufacturing sector, which may be increasingly feeling the pressure from the factory sector struggles in continental Europe.”

The U.S. bank goes on to suggest ‘peer group pressure’ from other central banks turning increasingly dovish could be a further incentive for the BOE to turn dovish itself.

They forecast an eventual BOE rate hike not coming until 2020.

Given Manufacturing could be the weak link in the economy, the spot-light may be more closely trained on UK Manufacturing PMI data for July out on Thursday morning at 9.30 BST which is expected to show a decline to 47.7 from 48.0 previously.

A deeper-than-expected lapse as seen in European figures last week could spark weakness in the Pound, as it could be seen as the crack which could open up a wider slowdown.

The Euro: What to Watch

The main release in the week ahead for the Euro will be GDP data for the second quarter which is expected to have grown by 0.2% in Q2 and 1.0% compared to a year ago. GDP above inflation, that is.

Such a result would be in line with current ‘barely a pulse’ estimates for Eurozone growth. A lower-than-expected result, however, would further solidify expectations the ECB will use its bazooka in September to reflate. Such a move would be detrimental to the Euro.

Although Manufacturing PMIs have fallen to Eurozone debt crisis levels their Services counterparts have remained relatively resilient.

“The advance release for Eurozone real GDP growth in the second quarter is due out next Wednesday, and the data are likely to show that the European economy continues to sputter. Real GDP in Europe has accelerated modestly over the past few quarters, but the year-over-year pace is still just 1.2%, and our expectation is for the quarterly growth rate to downshift back down to 0.2% in Q2. If this forecast proves correct, year-over-year growth would still be stuck around 1%,” says Wells Fargo.

Other key data prints are Eurozone unemployment, retail sales, and CPI.

July inflation is forecast to moderate to 1.1% from 1.3% in June and if so this is likely to keep the pressure on the Euro.

Although inflation is traditionally seen as a bugbear for the economy, in the current perennially low-growth environment higher inflation is actually positive for a currency, as it is a sign of stronger growth and therefore more likely to attract foreign investor inflows.

The unemployment rate is forecast to remain unchanged at 7.5% in July when it is released at 10.00 on Wednesday.

Retail sales are forecast to show a 0.3% rise in June compared to May when it declined -0.3% when it is released at 10.00 on Friday.

* Advertisement