Image © SlayStorm, Adobe Stock

- Charts indicate GBP/EUR to continue falling

- Possibility of decline into 1.11s

- Pound dominated by Brexit headlines; Euro by retail sales data

Pound Sterling is seen holding a mildly bearish tone in the coming week, however we don't see the prospect of any major directional move in the currency owing to the chronic uncertainty over Brexit.

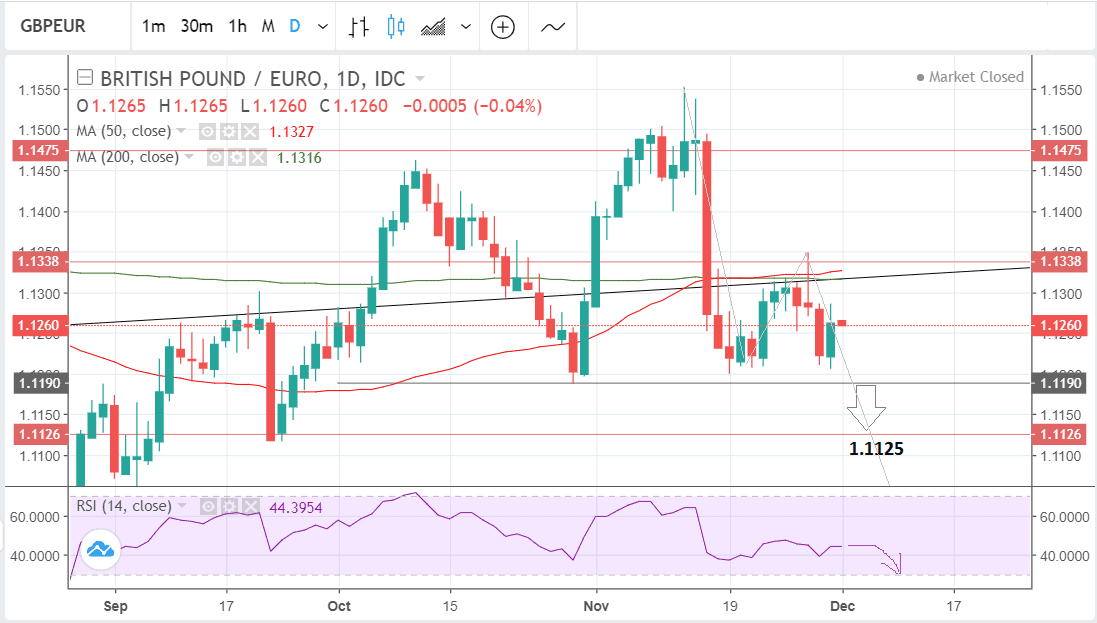

The Pound-to-Euro exchange rate ended the previous week trading at 1.1260, a fall from the 1.1301 close of the previous week.

Brexit uncertainty continues to take its toll whilst the broader Euro gained at the expense of a weakening Dollar. In the week ahead, charts suggest the pair will trade with a negative bias.

The pair rose during most of September and October and then peaked on November 13 at 1.1551, since then the exchange rate has been in decline and has established a short-term downtrend.

Given the market dictum that “the trend is your friend...” this short-term downtrend is more likely to extend than not, although we would ideally wish to see confirmation from a break below the key October 30 lows at 1.1187 for added confidence.

Such a break would open the way for more declines down to a target at 1.1125, where the S1 monthly pivot is situated and likely to break the fall. Pivots - as the name suggests - are levels on charts which show a greater propensity for turnarounds in the trend.

The initial steep decline since the Nov 13 highs looks like the first leg of a three-part move which will end with another leg lower reaching the aforesaid target in the 1.11s.

The RSI momentum indicator in the bottom panel is mirroring the exchange rate as it unfolds sideways after the initial decline and also looks poised to begin a second leg lower. This adds confirmation to the bearish forecast for the underlying instrument.

Sterling is tipped to open the new week around the 1.1276 mark on the interbank markets. This means the rate on offer at high-street banks should be in the 1.0980-1.1060 bracket while independent specialist providers are expected to offer currency in the 1.1170-1.1190 bracket.

The Pound: What to Watch

Brexit politics will probably dominate the Pound in the coming week as Theresa May tries to woo as many MPs as possible to vote for her withdrawal deal.

As things stand, however, it looks increasingly unlikely she will be successful and there is significant uncertainty as to what will happen following the defeat with a number of potential scenarios likely to play out.

The uncertainty is likely to ensure Sterling trades recent ranges with traders unwilling to take a big directional punt on the currency until such a time as they know what the future EU-UK relationship will look like.

At the weekend Sam Gyimah, the Science and Universities minister, became the latest member of May’s government to resign after saying leaving the EU risked the UK’s interests being “repeatedly and permanently hammered,” and that the UK was at risk of losing ‘its voice its vote and its veto’.

Gyimah appeared to endorse a second referendum in his resignation note on facebook, saying, “we shouldn’t dismiss out of hand the idea of asking the people again what future they want, as we all now have a better understanding of the potential paths before us”. His voice added to the growing number now calling for a second referendum.

Prime Minister May only has a majority of 5 seats in Parliament including her DUP allies who number 10 and all of them have said they will vote against her deal because it leaves Northern Ireland vulnerable to being treated differently to the rest of the British Isles.

Further opponents include 'brexiteer' rebels and 'remainers' from with her own party. Labour and other opposition MPs will also be encouraged to vote against her by their party whips.

This leaves the most likely outcome of the December 11 vote a defeat for the government. Experts say this would be most likely followed by either a general election or a second referendum, both causing further uncertainty, and probably keeping Sterling pressured.

On the 'hard' data front, the main releases for the Pound in the coming week are the three Purchasing Manager Index (PMI) surveys for November.

The first PMI to be released is Manufacturing, on Monday, at 9.30 GMT. It is forecast to show a recovery to 51.5 from 51.1 previously.

Construction PMI is out on Tuesday at the same time and is expected to show a fall to 52.6 from 53.2 in the previous month.

Services PMI - the more important of the three - is released on Wednesday and is forecast to rise to 52.5 from 52.2 previously.

PMI’s are often used by economists as a leading indicator of economic growth as the results often signal changes taking place in the broader economy before they are revealed in hard data such as GDP.

A result of over 50 signals an expanding economy whilst below 50 contraction.

Another key event in the week ahead is a speech from Mark Carney the governor of the Bank of England (BOE) on Tuesday at 9.15. This is followed by a speech from BOE’s Vlieghe on Tuesday at 18.00, and Haldane at 18.00 on Monday. Recently the bank released a worst case scenario of how Brexit would impact on the economy.

New car sales in November are set to be released at 9.00 on Wednesday and are considered a positive barometer of wealth creation.

The Euro: What to Watch this Week

It is a relatively quiet week for the Euro, although there is a risk of continued wrangling over Italy’s budget causing volatility.

Nevertheless, Italian PM Conte and EU Commission president Tusk were said to have made progress at talks at the G20 and the Italian government has now finally made concessions, saying they will consider reducing the deficit by 0.2%. Crucially it has shown ‘willing’ where once there was none and this has soothed markets.

On the 'hard' data front, the main release is probably retail sales for October out on Thursday, which is forecast to show a rise of 0.2% when it is released at 10.00 on Wednesday. If so, this would be an improvement from the 0.0% previous result.

Retail sales is often an early warning of growth so the October rate will be useful in gauging Q4 GDP growth. GDP slowed to only 0.2% in Q3 and if it continues to fall in Q4 it could signal a deeper contraction in the region with more profound implications.

A rebound, on the other hand, would play into the hands of the ECB who have largely underplayed the slowdown in growth the Eurozone has suffered over recent weeks.

The European Central Bank (ECB) president Mario Draghi will be making a speech on Wednesday at 8.30 and this could also generate interest if he mentions the outlook for monetary policy which has dimmed amidst the recent slowdown in growth.

If Draghi makes any hints that the ECB could be reconsidering its current roadmap for normalizing monetary policy, however - unlikely as that still seems - the Euro could plummet.

The other major Eurozone data releases are revisions of flash estimates of manufacturing and services PMIs (on Monday and Wednesday at 9.00 respectively), and the third and final estimate for the Q3 GDP growth rate out on Friday at 10.00.

Advertisement

Bank-beating GBP exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here