Latest trade numbers suggest Britain’s Current Account deficit is likely to remain at record levels ensuring the pound’s 'achiles heal' won’t disappear anytime soon.

- Trade deficits hits levels last seen during financial crisis; number one risk for sterling's stability

- IoD believe services hold the key to UK extracting itself from its trade deficit

- "The 9% or so fall in trade-weighted sterling since around mid-November should provide some support to exporters in time as contracts are renegotiated" - Capital Economics.

The UK continues to import more than it exports which will ensure the country’s current account remains in deficit, something that should worry those hoping for a stronger British pound over the longer-term.

Data from the ONS showed the UK’s trade in goods deficit stood at -11.2BN in March, virtually unchanged on the -11.43BN recorded in the previous month.

According to the ONS, the narrowing of the trade in goods deficit between February 2016 and March 2016 reflected an increase in exports of £0.4 billion to £23.7 billion; mainly attributed to a rise in unspecified goods and machinery and transport equipment.

"We have not seen a quarterly trade deficit of this size since the early days of the financial crisis. The Government has a real challenge ahead if it hopes to meet its target to increase the value of exports to £1 trillion and support 100,000 new exporters by 2020," says Mike Cherry, National Chairman at the Federation of Small Businesses.

However, when services are taken into account the overall deficit stood at 3.8BN, down 0.5BN from February.

In fact the trade in services saw its surplus increased from 7.1BN to 7.4BN and according to Allie Renison, Head of EU and Trade Policy at the Institute of Directors it is in services where our best hope of closing the deficit lie:

"Our trade surplus in services continues to grow despite the wider slowdown we’re seeing in the UK services sector overall. High growth markets such as India and China are beginning to mature and focus on consumption and domestic demand, meaning that services hold the key to the UK’s future export success."

Despite some improvements we don’t see enough movement in the data to suggest it will help close the historically significant current account deficit on our Balance of Payments account anytime soon.

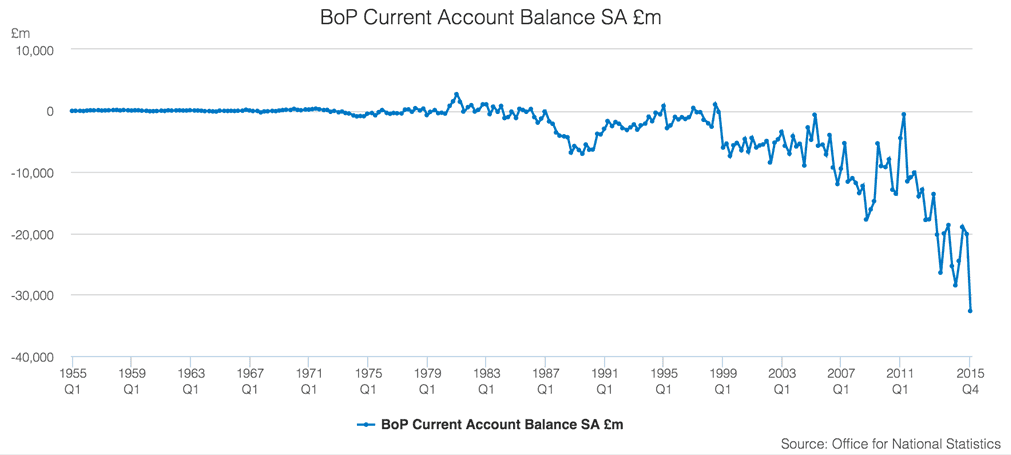

The trade deficit is the reason why the UK is subject to a record deficit in its Balance of Payments current account which stood at 32BN GBP in the final quarter of 2015.

The current account on our Balance of Payments is essentially the UK’s bank account with the world economy based on the trade of goods, services and income. When in deficit we are a ultimately a net debtor to the outside world and this has huge implications for the future value of our currency.

In fact, Scott Bowman at Capital Economics reckons we should be prepared for another record deficit number to be set next time the Balance of Payment data are released.

"The three-month deficit of £13.3bn – the highest since Q1 2008 – suggests that trade will make a larger negative contribution to the current account balance in Q1 than it did in Q4.

"What’s more, goods volumes data suggest that net trade subtracted more from GDP in Q1 than the 0.3 percentage points in Q4, contributing to the slowdown in GDP growth shown in the first estimate of Q1 GDP."

The current account deficit has become increasingly important ahead of the mid-year EU referendum as it is here where sterling is particularly vulnerable.

If sterling were purely valued according to the trade-off between imports and exports, it would be much lower.

However, the level it trades at is dependent on imports, exports AND investment inflows.

Were the UK to vote to leave Europe it is argued that these investment inflows would dry up as investment decisions are withheld.

This would see the pound drop notably lower to levels more in keeping with the import/export balance.

UBS reckon the pound falling to parity against the euro would be a likely occurance.

This could arguably be a good thing though as the weaker pound would make UK produce on the global market a whole lot cheaper than it currently is.

Thus, UK manufacturing and services receive a hefty boost which heals the trade deficit naturally while weaning us off our dependence on the financial account on our Balance of Payments.

Indeed, the pound’s declines through 2016 could be one light spot for the UK economy over coming months.

"The 9% or so fall in trade-weighted sterling since around mid-November should provide some support to exporters in time as contracts are renegotiated. And we think that global growth will pick up this year. But for now, the responsibility for driving GDP growth lays with the domestic services sector," says Capital Economics’ Bowman.