Image © Adobe Images

Is the cash sitting on balance sheets actually working hard enough?

I recently wrote about something that rarely features in discussions around interest rates: what UK businesses are actually earning on the cash sitting in their bank accounts.

At the time, some business banking balances were yielding close to 4%. For many companies, this quietly became a meaningful contributor to profitability. Not through financial engineering or risk-taking, but simply by paying attention to where surplus cash was held and on what terms.

Since then, the Bank of England’s Monetary Policy Committee cut base rates by 0.25% at the December policy meeting.

For business owners and finance leaders, this inevitably prompts the question: does this change the picture?

In headline terms, yes. Deposit rates will ease over time. The peak yields available on business cash are likely behind us.

But in more practical terms, the decision doesn’t alter the more important issue that the higher-rate environment exposed in the first place.

That issue is not the level of rates themselves, but how unevenly businesses engage with their banking arrangements.

A quarter-point cut does not remove the significant variation between banks, products and customers.

Even as rates come down, some businesses will continue to earn a reasonable return on surplus cash, while others will earn very little at all.

📍I am here to assist with a no-obligation consultation on how we can put your business's cash pile to work, you can sign up here.

The gap between headline rates and effective rates will persist, as will differences driven by negotiation, scale, and awareness.

In that sense, a falling-rate environment can actually make the problem harder to spot.

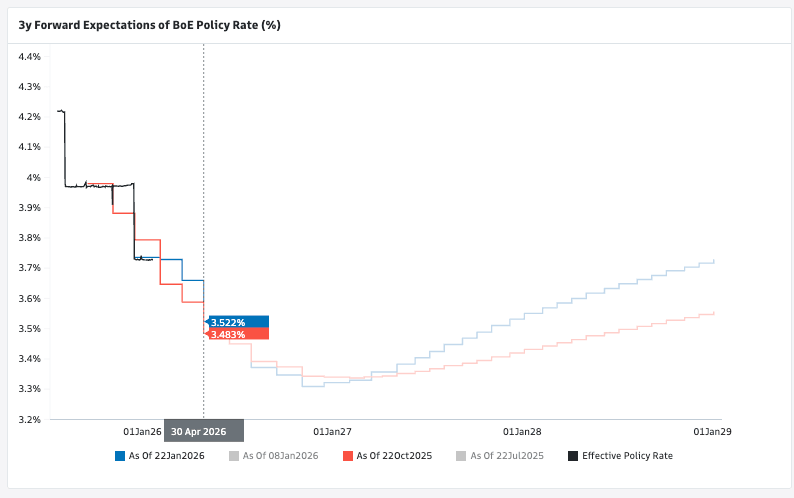

Above: Bank Rate expectations based on the markets forwards curve.

When rates were rising, poor returns on cash were more visible. Businesses could see, often for the first time, that meaningful interest was available elsewhere. As rates drift lower, that contrast becomes less obvious, increasing the risk that cash management slips back into autopilot.

It is also worth addressing a misconception that crept in over the past year: the idea that higher deposit rates represented a temporary windfall.

In reality, what higher rates really did was expose how passive many businesses had become about their banking relationships.

For years, ultra-low rates meant the opportunity cost of inattention was minimal.

That changed quickly, and many organisations discovered they had never properly reviewed how much cash they held, what was genuinely surplus, or what return they were receiving.

The MPC’s decision does not invalidate those lessons. If anything, it reinforces them.

The strategic question for finance leaders remains exactly the same as it was before the rate cut:

Is our cash working as hard as the rest of the business?

That question goes beyond interest earned. It touches on governance, liquidity

management and financial visibility.

It requires clarity over what cash is operational, what is genuinely surplus, and how balances are distributed across accounts and institutions.

For businesses with international exposure, it also links directly to wider considerations around currency, payments and treasury positioning.

Importantly, this is not about chasing yield for its own sake. It is about understanding that cash is an asset, and like any other asset on the balance sheet, it deserves deliberate management rather than benign neglect.

The Bank of England’s rate cut is a signal, not a solution.

Borrowing remains expensive, margins remain tight, and complacency remains costly. Cash is often the largest asset on a balance sheet, and the least actively managed.

Allowing it to sit idle or poorly rewarded is no longer benign; it is a quiet erosion of value.

📍I am here to assist with a no-obligation consultation on how we can put your business's cash pile to work, you can sign up here.