Image © Pound Sterling Live, Still Courtesy of Bloomberg TV.

The Bank of England must hike more than any other G10 central bank over the remainder of 2022 if it is to satisfy market expectations.

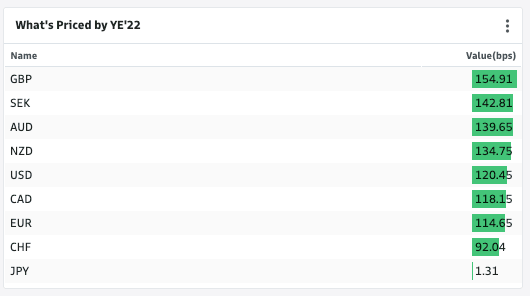

Following this week's UK data releases money market pricing now shows investors to be priced for 154 basis points of hikes by the end of the year.

That is more than is asked of the two typically hawkish antipodean central banks and the pace setting Federal Reserve.

Above: Market expectations for the major central banks, image courtesy of Goldman Sachs.

It implies three 50 basis point hikes are required at the three remaining meetings in September, November and December.

Given the Bank has already raised 50bp in August there is now a precedent and Threadneedle Street could deliver.

The implications for Pound Sterling are significant: if it meets this target the currency would likely remain supported, but another 'dovish' pivot from the Bank that disappoints against expectations could send it lower.

A look at the following pricing shows investors have ramped up their expectations from the Bank through August:

Image courtesy of Goldman Sachs.

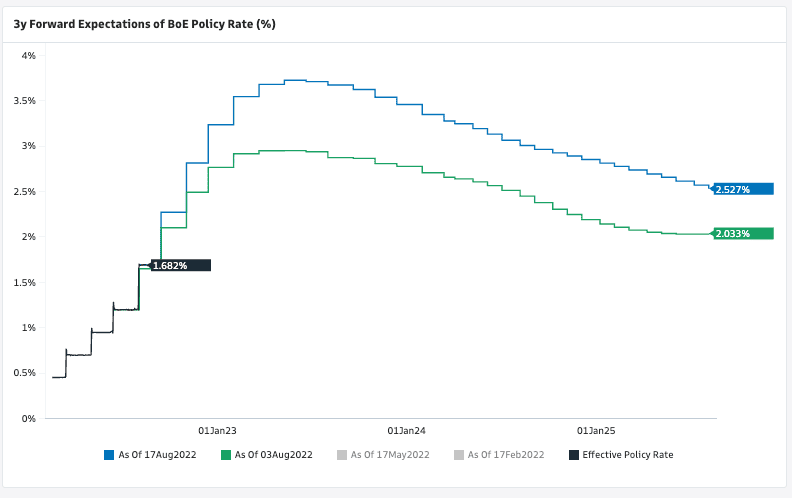

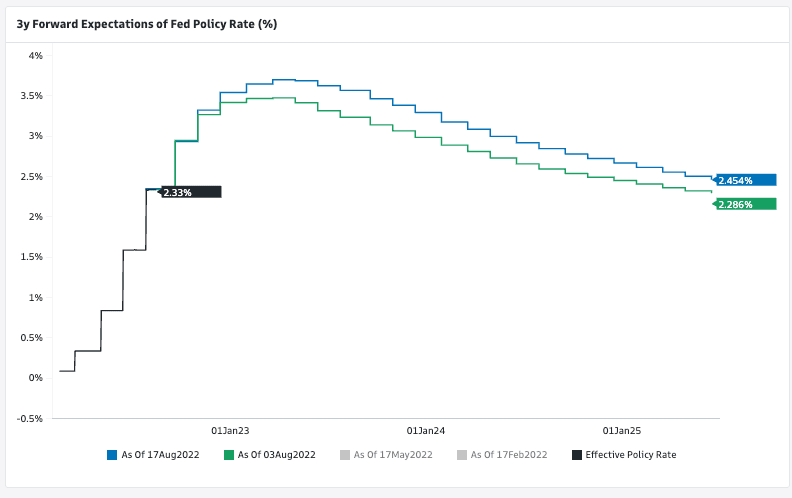

As can be seen in the below, Bank of England expectations have risen more than those in the U.S.:

image courtesy of Goldman Sachs.

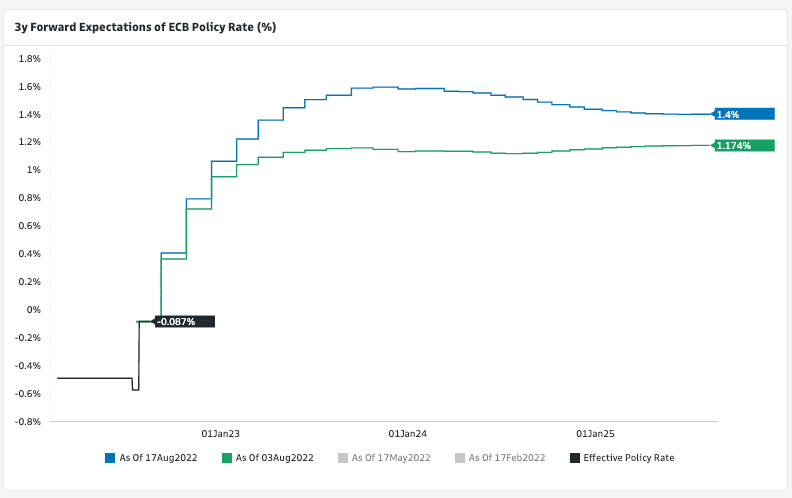

And more than in the Eurozone:

image courtesy of Goldman Sachs.

The need to raise rates further than the Bank had expected as recently as the August 04 policy update comes on the back of this week's solid labour market data that showed wages increased by a greater amount than markets were expecting.

But it was inflation data which revealed annual inflation had reached 10.1% growth that pumped expectations.

The Bank itself projects inflation will peak at around 13% later in the year following the next round of energy price rises and has committed to tackling inflation "no ifs, no buts", in the words of Governor Bailey.

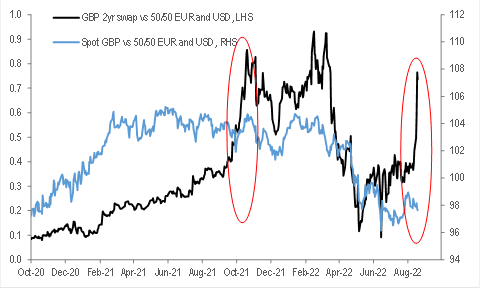

Adam Cole, Senior Currency Strategist at RBC Capital Markets, also observes a rise in rate hike expectations, but using a different measure that charts against the Pound's value:

image courtesy of RBC Capital Markets.

He notes however that this pick up in expectations has not benefited the Pound against the Euro and Dollar to any meaningful degree.

It suggests GBP exchanges rates have decoupled from rate expectations.

Of course the Pound might play catch up and go higher over coming days and close the gap.

However, expectations for a marked slowdown in UK economic growth is likely keeping buyers at bay for now and the gap between interest rate expectations and GBP exchange rates could remain large.

It is also worth noting in the above charts that the downslope on the Bank of England chart (2nd chart) is bigger than any of the others, therefore the Bank will likely cut more in 2023 than its peers.

Perhaps, that is what matters most for forward-looking markets and therefore the Pound is finding little benefit to the sharp rise in near-term money markets.