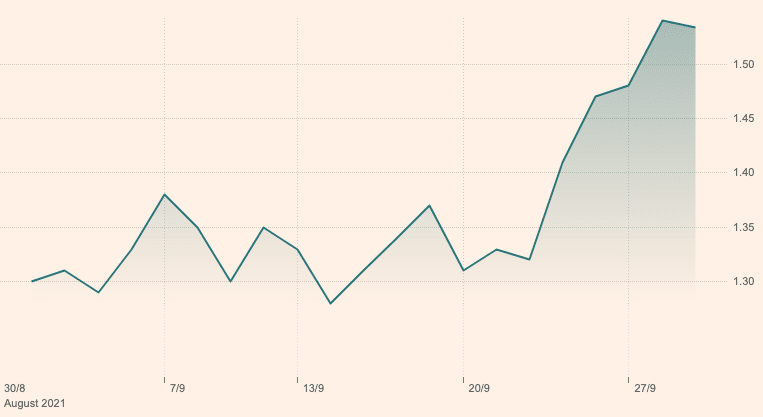

Above: U.S. ten year bond yields. Source: FT.

Surging bond yields and falling markets are telling us that investors are fearful that rising inflation will become enduring and that central banks will inevitably have to raise interest rates.

The sweet spot for global markets that has seen rising growth and low inflation could therefore be over, however some analysts we follow say this spell of investor unease will prove to be temporary.

"You know something’s wrong when stocks and bonds sell off in lockstep. The simple answer is fear that structurally higher inflation risks weighing on growth," says Mathias Van der Jeugt, analyst with KBC Markets.

This observation applies to the UK and the Pound in particular where rising inflation linked to an energy crisis looks more acute than in Europe, the U.S. and other nations.

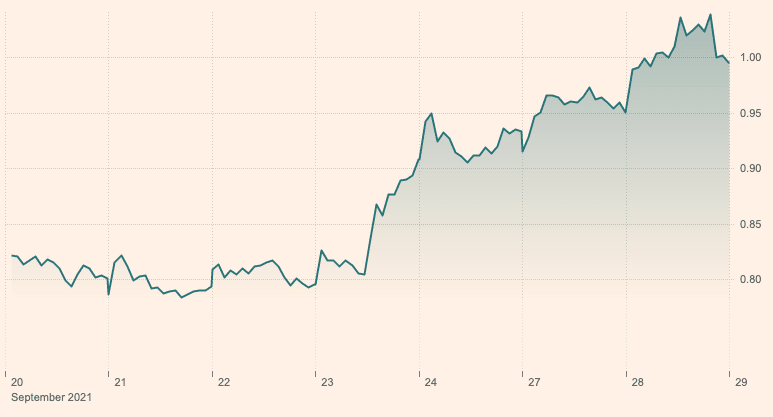

The U.S. ten-year bond yield went above 1.52% while the UK ten-year bond yield pierced 1.0%.

Above: UK ten year bond yields, source: FT.

Stock markets sank and the Dollar proved to be the main beneficiary.

Inflation risks becoming structural when the consumers and businesses react to persistently high inflation caused by the kind of supply shocks we are currently seeing.

Fears of such a development were expressed by the Bank of England's Governor Andrew Bailey in a speech delivered this week where he said inflation could become self sustaining and therefore require central bank intervention.

Delivering testimony to the Senate Banking Committee on Tuesday, U.S. Federal Reserve Chair Jerome Powell said:

"Bottlenecks, hiring difficulties, and other constraints could again prove to be greater and more enduring than anticipated, posing upside risks to inflation. If sustained higher inflation were to become a serious concern, we would certainly respond and use our tools to ensure that inflation runs at levels that are consistent with our goal."

Van der Jeugt says central banks would eventually be obliged to tighten the screws on monetary policy despite the inflation shock being initially supply-side in nature.

"End result: stagflation," he says.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Michael Brown, Senior Market Analyst at CaxtonFX says the bond market's behaviour "is a classic sign of the market pricing in tighter monetary policy, both through tapering and, eventually, rate hikes".

But Brown says he remains of the view that the surge in inflation will ultimately still prove temporary in nature, a view echoed by Federal Reserve Chairman Jerome Powell.

Investors were naturally drawn to Powell's comments on inflation's ability to become more structural, understandably as they were made on a day of falling stock markets and surging bond yields.

But he said:

"These effects have been larger and longer lasting than anticipated, but they will abate, and as they do, inflation is expected to drop back toward our longer-run 2 percent goal."

If this view is indeed proven correct then the greater the likelihood that the current market spasm is temporary.

"Rising US yields in anticipation of a faster-than-expected withdrawal of monetary accommodation, among other factors, contributed to the market decline on Tuesday. Despite the latest setback, we expect market sentiment to recover in line with strong economic and earnings fundamentals," says Mark Haefele, Chief Investment Officer, UBS Global Wealth Management.

UBS says bond yields can still rise further in coming days with the U.S. ten-year reaching 1.8% by the end of the year.

But stocks can recover "as the gradual shift in central bank policy is more reflective of good economic growth than worries over persistent inflation," says Haefele.

The obvious way to pop the stagflation fear is for surging energy prices to come back down as they are a key ingredient of the rising inflation expectations amongst investors.

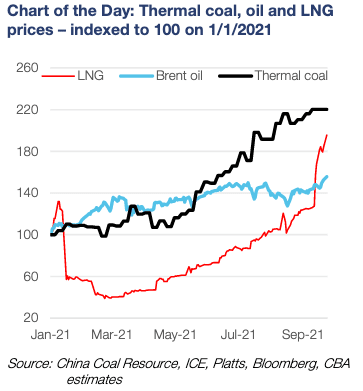

"What is happening on energy markets?" asks Norbert Rücker, Head of Economics & Next Generation Research at Julius Baer.

"The V-shaped recovery overburdens slower-moving and more complex energy supply chains. While this by itself should be known, too many little hiccups finally lead to a fierce upwards spiral," is his explanation.

He says these hiccups include coal supply disruptions in China and elsewhere, natural gas supply disruptions due to maintenance and outages in Norway and Russia, as well as soft wind conditions and drought, curbing wind production in Europe and hydropower in China earlier this year.

Image source: CBA.

"On top, mechanisms such as Europe’s market-based emission trading scheme seem to become an unintended booster of prices under such conditions," says Rücker.

But Rücker says there seems to be too much froth in both natural gas and oil markets.

"A chilly winter could make things worse, but natural gas prices at current levels imply big bets on such a possible outcome. On the oil market, meanwhile, supplies are constrained for political, not structural reasons," he says.

He adds that oil politics is a function of prices, and with oil close to or above $80 per barrel, the pressure from the consumer economies on the petro-nations to ease restrictions more is growing swiftly.

Furthermore, China’s power outages and high fuel prices at the pump in the United States should visibly dent oil demand.

"In our view, the current energy market dynamics rather fit with the excesses and hiccups usually happening at the peak of a cycle, and we do not believe they are the result of more concerning and lasting structural imbalances," says Rücker.

UBS expect oil prices to remain contained as disruptions from Hurricane Ida dissipate and OPEC output picks up through coming months.

Gas and coal markets will likely remain tight says Haefele as demand persists to replenish storage, but should come down next year as Russian and South African supplies pick up.