Image © Adobe Images

The stock market is not in a bubble and the rally of recent months could yet extend say analysts at a major Wall Street bank.

Bank of America's equity analysts say signs of "froth" in the market suggest to some that equities are in a bubble, but they argue a bubble is a price rise not justified by fundamentals.

U.S. equity markets in particular are under the spotlight, with market participants asking whether their record highs can be justified given that the real economy is struggling.

The concern is that if a bubble is forming, it will inevitably pop, resulting in a shock right across the financial market.

"Market commentators point to increasing signs of froth as evidence that the equity market is in the late stage of a bubble, which is set to burst soon," says Sebastian Raedler, Investment Strategist at Bank of America.

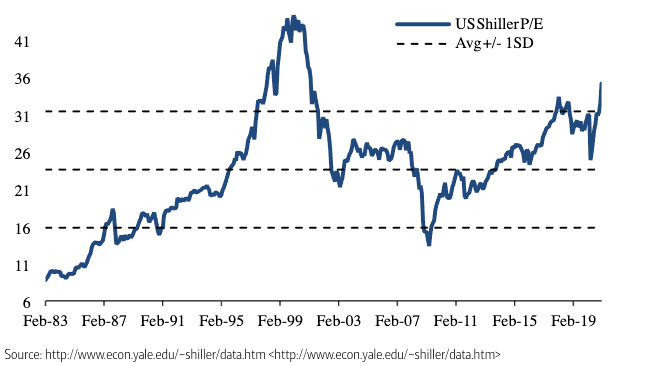

Above: With the Shiller P/E rising to 35x, the highest level in 20 years, concerns are rising that the equity market is in the late stage of a bubble, which is bound to burst soon. Image courtesy of Bank of America.

Given that currencies are highly responsive to investor sentiment, what happens to equity markets over coming months will therefore prove incredibly important for exchange rate movements.

The British Pound will not be left unscathed if markets do tumble, given the observation that it has become increasingly responsive to equity market movements in 2021.

But, economists at Bank of America have sought to allay investor fears that a bubble is expanding.

"The key fundamental driver of equities is growth momentum, which is set to be exceptionally strong this year," says Raedler. "We think this is not a bubble, but the pre-pricing of a growth surge, with our PMI projections implying 10% upside by Q3".

U.S. stocks are leading the charge and climbed further at the start of the week, hitting record levels as investors remained optimistic about further Covid stimulus and a vaccine-lead economic recovery.

The Dow Jones Industrial Average rose 237.52 points, or 0.8%, to a record high of 31,385.76. The S&P 500 gained 0.7% to a fresh closing high of 3,915.59.

This markets the longest winning streak since August for these two flagship indices.

The Nasdaq Composite - the nest of the world's most desirable growth stocks - advanced a further 1% to 13,987.64, also hitting a new record.

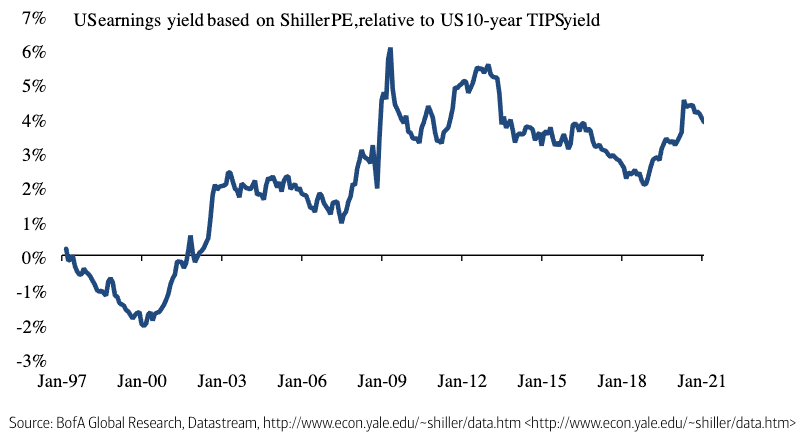

Above: Adjusting the Shiller P/E for the level of real bond yields, i.e. the discount rate for equity multiples, suggests that valuations are not excessive, and are more attractive than they were in the months running up to the Covid crisis and much more attractive than 20-years ago. Image courtesy of Bank of America.

The rally coincides with a rise in the value of the British Pound, which has become increasingly aligned to equity market sentiment ever since the EU and UK agreed a post-Brexit trade deal last December, allowing the currency to focus on other drivers.

Despite the impressive pace of the equity market's rally, the gains are justified says Bank of America.

Bank of America economists expect U.S. GDP growth to rise to 5% this year, the strongest GDP growth in almost 40 years, while Euro area GDP growth is projected to accelerate to 6% annualised in the second quarter and 7.5% in the third quarter.

This is consistent with a rebound in the Euro area composite PMI new orders close to a 20-year high of 60 by early the third quarter.

"This suggests the recent run-up in equity prices is not so much a bubble, but rather the pre-pricing of the extremely strong growth conditions that are likely to materialise this year," says Raedler.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

But this observation does depend on a assumption that the economic rebound will continue, and therein lies a risk to the bullish investor sentiment that has become so pervasive.

Risks eyed by Bank of America include:

(1) The risk of vaccine failure: "early evidence from Pfizer/BioNTech and Moderna suggests that their Covid-19 vaccines offer protection even against the new, more contagious virus strains. However, with the assumption of a sharp growth ramp-up by mid-year predicated on improved vaccine availability from Q2 onwards, any reduction in the vaccines' efficacy or any delay due to required modifications could lead to a feebler recovery, thus weakening the case for further equity market upside".

(2) the risk of a bond market tantrum:

This is defined as a disorderly rise in nominal and real bond yields.

Yields would rise in response to accelerating growth, a rebound in headline inflation and the hand-over from monetary to fiscal stimulus.

"If this materialises, the rise in the discount rate would likely lead to sharp multiple compression, with markets falling by around 10% during the tantrum episodes in 2013 and 2015," says Raedler.

The Federal Reserve's ongoing support for the economy will be key, with stocks likely to decline should markets sense the Fed will start winding down its quantitative easing programme before the economy has fully recovered.

The U.S. Dollar rally of recent days is being attributed by analysts we follow to a rise in expectations that the U.S. Federal Reserve will have to start withdrawing support to the economy at some point in 2021 or early 2020.

"A key theme for 2021, especially later in the year, is the Fed’s policy normalisation plan once we see a significant economic recovery when the vaccination process has come such a long way that restrictions can be lifted permanently," says Mikael Olai Milhøj, Senior Analyst at Danske Bank.

While expectations for an actual move at the Federal Reserve in 2021 is low, investors are preparing for the eventuality that the Fed starts discussions on easing back on the pace of quantitative easing.

The expectation is founded on fears that inflation will start moving higher again thanks to the Fed's current policies. However, the Fed has been in the market for some time, the 'game changer' appears to be the expectation for generous handouts from the Biden administration, which is tipped to deliver a $2TRN stimulus programme, the lion's share of which will end up in the pocket of U.S. consumers.

Uncomfortably high inflation is typically combatted by the withdrawal of monetary support at the Fed, in a process known as 'tapering'.

The developments will ignite memories of 2013's 'taper tantrum', a reactionary panic amongst investors that triggered a spike in U.S. Treasury yields and the Dollar, after investors learned that the Fed was slowly putting the breaks on its quantitative easing programme.