Above: Federal Reserve Governor Jerome Powell. File photograph. Image © European Central Bank

- Easing global growth fears to impact central bank settings

- Impending shift by central banks to impact currencies

- Change of hawkish shift from Federal Reserve

Global growth fears have eased on the back of strong data from China this week. This has paused - for now at least - the multilateral retreat undertaken by almost every major central bank fears a slowing global economy will infect growth in their own backyard.

Given fears are easing, the question is how much this will affect central bank policy settings going forward.

Certainly, the impact will have repercussions for the global currency market which is heavily dependent on central bank policy settings.

Will central bankers row back from their dovish tilt (dovish meaning in favour of lower interest rates) and start to adopt progressively more optimistic hawkish stances (hawkish meaning in favour of higher rates)?

Central bank monetary policy is one of the most important drivers of exchange rates. When interest rates rise it is generally supportive of the local currency and vice versa when rates fall. Any adjustments in monetary stances, therefore, are likely to impact on FX markets.

It is the interest rate differential between two currencies which determines the direction of capital flow, with money tending to go from lower to higher interest rate jurisdictions, and therefore supporting the currency bearing the higher interest rate.

Chinese data showed substantial gains in broad growth in Q1, in exports and in retail sales. The data appeared to be something of a game-changer for markets. It boosted the country’s economic prospects and deferred hard-landing fears. Along with increased hopes of a trade detente between the U.S. and China, this has boosted the outlook for global growth entire.

The currencies most likely to be impacted by the change are the commodity currencies which rely the most on global trade; these include AUD, CAD, and NZD, followed by the large currencies USD, EUR and GBP.

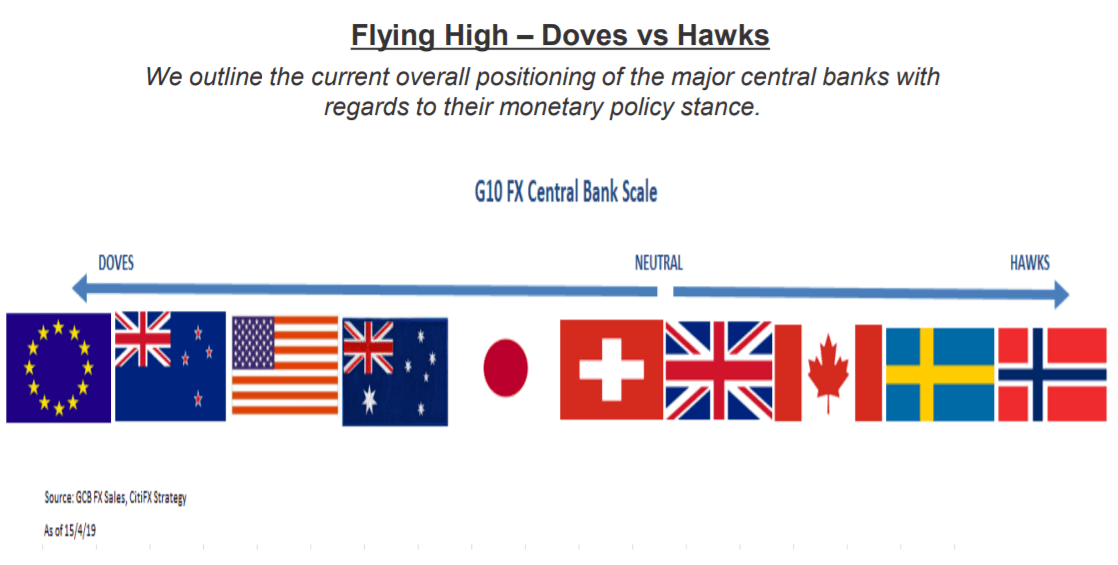

Citibank has come up with a graphic to illustrate where they think major central banks are now positioned on a scale of dovish to hawkish. The graphic below shows the European Central Bank (ECB) is currently the most dovish and the Norwegian Riksbanks the most hawkish.

Citi’s more specific views on each central bank are as follows:

The U.S Federal Reserve

There is a chance of a hawkish shift for the Fed. Recent data has been strong, revealing a robust economy. March inflation came out at 1.9%, above expectations of 1.8%. Initial jobless claims came in at sub 200k (196k), again another positive. Normally this would point to higher interest rates to cool things down.

Just before the Chinese data release, Citi said “the US Fed has pivoted to a much more dovish stance over recent weeks,” citing global growth risks as well as growing domestic uncertainty.

With one of these knocked out, it would seem logical to assume a shift to a more hawkish stance. Ostensibly positive for USD.

The European Central Bank

Data out of Europe has been especially poor recently with the exception of the ZEW sentiment gauge and service sector PMI, however, inflation and manufacturing have both disappointed, with the latter falling dramatically.

March PMIs out on April 18 disappointed to the downside, showing the Eurozone is yet to turn a corner after months of lacklustre growth that saw Italy slip into recession and Germany barely dodge recession.

This has been concerning for the ECB and suggests the possibility of a regression back to stimulus measures more fit for crisis-era policy.

Yet despite this, the Euro has remained resilient. One main reason why is that the Euro has now baked in so much bad news that things can only get better. Thus risks now lie to the upside.

If anything this will be enhanced by the positive data from China which will improve the outlook for trade-related growth prospects in Europe.

Citi says: “Following the ECB’s prior meeting, they are placed on the most dovish end of the scale. However, we do see upside for the EURO going forward. Why? The ECB has been on the dovish end to the scale for a long time and so the market has priced in a lot of negative expectations. Should we see the Eurozone flag move to the right of the scale, that is where the upside would be felt.”

Bank of England

The outlook is turning progressively more hawkish for the BOE due to consistently strong wage data releases, indicating the likelihood of robust growth on the back of consumer spending and rising inflation. From previously seeing the BOE as stuck in ‘wait-and-see’ mode Citi now sees risks of a rate hike in one of the 5 remaining meetings this year.

“There are 5 BoE meetings left in 2019. The fresh Brexit extension (to October 31) allows for some breathing space and if UK data holds up, the August meeting might then become more ‘live’ than markets anticipate,” says Citibank.

Reserve Bank of Australia

If any central bank would be expected to shift stance as a result of improved Chinese data it would be the RBA, given the intimate trade ties between the two nations.

Recent commentary from the RBA was positive even before the Chinese data. It already reflected a marked shift from dovish to neutral.

The weak housing market has always been a central hazard for the RBA but officials recently downplayed risks because despite the slowdown actual mortgage defaults have remained low due to the strong labour market.

Overall the Chinese data only solidifies the move of the RBA to centre ground and underpins AUD.

Bank of Canada

Recent strong data, a rise in oil prices and a more benign global backdrop have led to a sea-change in the stance of the BOC, and done wonders for the prospects of the Canadian Dollar in the process.

Most analysts, including Citi’s now see a further interest rate hike from the BOC as a fait accomplis. CAD should keep moving higher if they are right.

“Citi analysts think a more consistent picture of rebounding activity in Canada will likely be seen in data later this year. With Canadian core CPI remaining around the BoC’s 2% target, Citi analysts continue to point to the next move by the BoC as more likely to be a rate hike than a cut,” says the bank.

Reserve Bank of New Zealand

RBNZ is an outlier from the general seismic shift to a more hawkish policy setting, after recent inflation data showed a dramatic slowdown in March CPI which now suggests the next policy move from the Bank will almost certainly be to lower rather than raise rates.

Close trade ties to China will offset some of the damage and some analysts expect the downside to be short-lived as a result but not Citi.

“Citi analysts suspect that yearly NZ CPI will likely undershoot RBNZ’s forecast out till 2020 end and therefore expect RBNZ to cut rates by 25bp in May and again in November,” says the bank.

Prospects for NZD are therefore not great from a domestic sense. However, some analysts are of the view that even if the RBNZ cuts interest rates, the currency should be supported by a more constructive shift in the global economy.

The Scandanavian Banks

![]()

The Norwegian central bank (Norges Bank) is the most hawkish on the Citi scale mainly as a result of the strong rise in crude oil prices since the country is a major producer and exporter of oil.

The Swedish central bank (Riksbank) is also at the hawkish end due to its already extremely easy monetary policy stance, which includes a negative repo rate of -0.25%. A hike is seen as the next move.

“As in December, the forecast for the repo rate indicates that the next increase will be during the second half of 2019, provided that the economic outlook and inflation prospects are as expected,” is the Riksbank’s official view.