© Grecaud Paul, Adobe Stock

- GBPEUR advances after Eurozone PMIs disappoint market in April.

- Growth may have slowed further thus far in Q2 but it's still early days.

- UBS bearish on GBP long-term but eyes support over coming months.

The Euro ceded ground to Pound Sterling Thursday after IHS Markit PMI surveys suggested the Eurozone economy missed out on the first-quarter recovery in China, as the former's industrial recession appears to have deepened during April.

The German manufacturing PMI came in at 44.5 for the month of April, up from a downwardly-revised 44.1 in February when consensus had been for the index to come in at 45.2. February's number was previously reported as 44.7.

It wasn't just the German manufacturing sector that was creaking in April either as the French manufacturing PMI fell to a new low of 49.6 this month, down from 49.7 previously and when markets had looked for it to rise back to 50.0.

"A solid service sector performance in Germany helped sustain the expansion, offsetting a sharp manufacturing downturn. France meanwhile stagnated and the rest of the region saw the worst growth since late-2013," IHS Markit says.

Manufacturing and services sectors from other economies also surprised on the downside too, as was evidenced by the bloc-wide fall in the Eurozone services PMI, which fell from an upwardly-revised 53.3 to 52.5 in April .

That was despite decent numbers from France and Germany. The Eurozone manufacturing PMI rose to 47.8 in April, from 47.5 previously, although consensus had favoured a larger move up to 48.1.

PMI surveys measure changes in industry activity by asking respondents to rate conditions for employment, production, new orders, prices, deliveries and inventories. A number above the 50.0 level indicates industry expansion while a number below is consistent with contraction.

Markets care about PMI data because it is an important indicator of momentum within the economy. And economic growth has direct bearing on consumer price pressures, which dictate where interest rates will go next.

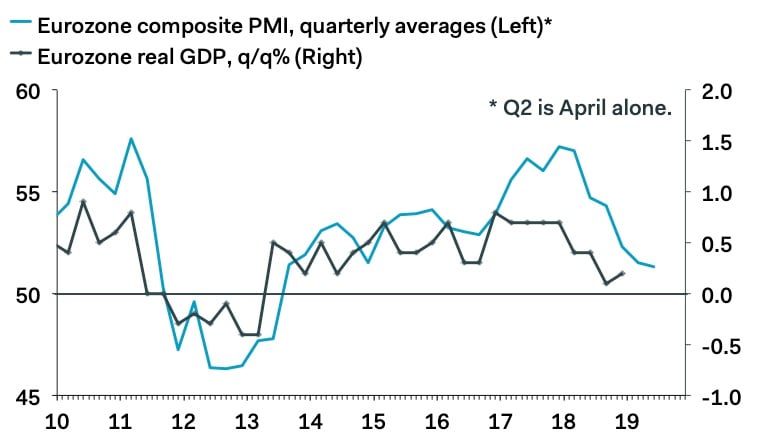

Above: Eurozone PMI correlation with real GDP growth. Source: Pantheon Macroeconomics.

"The slowdown in manufacturing eased slightly, but the overall story remains grim. Output and new orders are falling steadily, and because demand is sliding more quickly than the rate of contraction in production, work backlogs are also now in a sustained downtrend. Weakness in export orders, especially from the U.K., are one of the main drags. By contrast, the services sector is doing much better on all accounts," says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics.

Manufacutring surveys were released alongside measures of services sector activity, which surprised on the upside for April in Germany and France, although this was not enough to prevent the bloc-wide Eurozone services PMI from sliding to a new low of 52.5 this month.

The Eurozone services PMI was initially reported as 52.7 in March but that number was revised higher to 53.3 Thursday and consensus had been in favour of a 53.1 reading for April. Viewed from whichever angle, the April Eurozone services PMI was also a disappointment for market.

"The Composite PMI for France edged up but is still consistent with fairly weak GDP growth," says Andrew Kenningham, chief Eurozone economist at Capital Economics. "A weighted average of the Composite PMIs for the rest of the euro-zone must have dropped back again in April, so there may be more disappointing news to come from Italy and/or Spain when the final surveys are published at the end of the month."

Above: Pound-to-Euro rate shown at hourly intervals.

The Pound-to-Euro rate was quoted 0.19% higher at 1.1566 following the release and is now up 4.02% for 2019.

"We retain our bearish bias over the long-term; but reduced 'no-deal' near-term Brexit risks should offer temporary support to sterling," says Vassili Serebriakov, a strategist at UBS. "Overall, the scope for a further bounce is fairly limited and over the longer-term, the UK's external imbalances are a more critical influence on sterling's ultimate destination. To reflect this mixed picture we maintain our combination trade of long domesticallygeared UK equities and long EUR/GBP as part of Top Macro Trades."

Thursday's gain owes itself to a steep -0.37% fall in the Euro-to-Dollar rate, as the Pound-to-Dollar rate was also seen in the red during the morning session.

The Pound was lower against half the G10 basket Thursday even after retail sales figures for the month of March surprised on the upside to such extent, one economist described the numbers as "astonishing".

Above: Pound-to-Euro rate shown at daily intervals.

Thursday's data comes hard on the heels of a trading session where markets were buoyed by newfound optimism about the outlook for the global economy after a series of Chinese economic numbers including the first-quarter GDP figure surprised on the upside.

"The flash PMIs for April suggest that, despite some stronger industrial production data in the first couple of months of this year, the euro-zone has not yet turned a corner and that the manufacturing slump in Germany has continued at the beginning of Q2," says Kenningham of Capital Economics.

China's economy grew at an annualised pace of 6.4% in the first-quarter of 2019, unchanged from the rate of growth seen in the final quarter of last year, when markets had looked for it to dip to 6.3%.

Furthermore, growth in fixed asset investment, industrial production and retail sales all picked up during March, suggesting the world's second largest economy may have gained momentum heading into the second quarter.

Wednesday's data reenforced the idea in the market that "green shoots of recovery" are now sprouting up everywhere around the global economy.

"The stimulus-induced (dare we say artificial) bounce in China’s data has yet to feed through into the Eurozone economic picture. This positive feedback loop could still materialize – it would be foolish to completely rule it out – but we live in a world where it’s worth questioning the strength of that feedback loop, especially since China’s stimulus has not been all that big," says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

Given the correlation between manufacturing activity in Germany and China, some in the market may have anticipated that April's PMI surveys would reveal signs of an upturn in Europe too.

Official first-quarter economic figures will not be released until May but the European Central Bank (ECB) has already said that 2018's economic slowdown almost certainly carried over into the New Year, prompting the governing council to abandon plans for a 2019 interest rate hike.

"What is pretty clear to us is that some investors were long EURUSD into this morning’s data thinking the results would be stronger," says BMO's Gallo.

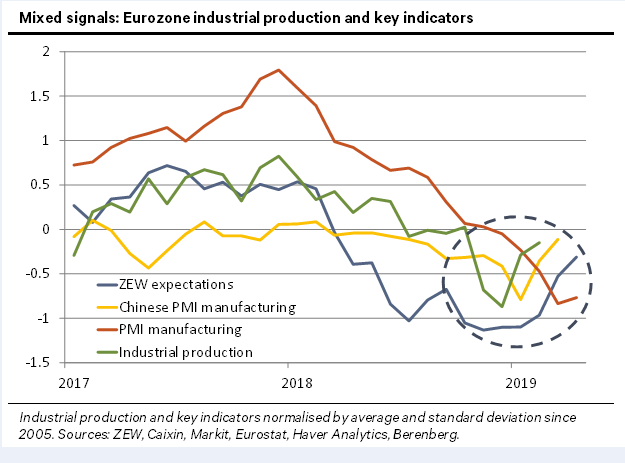

Above: Eurozone growth indicator correlations with GDP growth. Source: Berenberg.

"The export-oriented Eurozone has suffered more than other regions from the global trade slowdown over the past 12 months. Most recent data, such as the 6% fall in export orders for German manufacturing in February, project further weakness ahead. But the newsflow is no longer uniformly bad, " says Holger Schmieding, chief economist at Berenberg.

Eurozone growth fell to 0.2% in the third quarter of 2018, to 0.1% in the final quarter, which took annual GDP growth down from 2.3% to 1.8% last year. The ECB said in April that growth probably slowed even more in the first quarter and that inflation could fall further over the coming months.

This matters for the Euro because the bank needs faster economic growth in order to get the consumer price index and core inflation back toward the target of "close to but below 2%". It can't lift interest rates in a meaningful manner until inflation can sustainably hold the target level.

Thursday's data suggests economic weakness in the Eurozone may have even extended beyond the first quarter, although there's still more than two months left to go in the second innings of the year.

The coming months could yet reveal signs of a Eurozone recovery although the market might be deep into the third-quarter before such a thing is confirmed by official growth figures. Until then, IHS Markit surveys and a drip feed of official industrial output statistics will be enough to help economists firm up estimates.

"Near term, Eurozone industry looks set to remain weak. For the outlook from mid-2019 onwards, however, we are more optimistic than consensus. If and when the industrial cycle in the export-oriented Eurozone turns, it could do so noticeably. Some uptick in domestic activity in Europe on top of fading external burdens could see to that," says Berenberg's Schmieding. "As usual, it could still be a bumpy ride, though. The period during which data are mixed rather than mostly good still looks set to last for a few more months."

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement