- CHF the major FX underperformer amid U.S. bond yield rally

- Yields rise from slumber on signs of U.S. growth acceleration

- Leaving CHF, other low yielders vulnerable to further losses

- But global growth worries, Asia’s virus woe tempers declines

Image © Adobe Images

- GBP/CHF reference rates at publication:

- Spot: 1.2775

- Bank transfers (indicative guide): 1.2328-1.2417

- Money transfer specialist rates (indicative): 1.2660-1.2686

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Swiss Franc has been a standout underperformer among major currencies in the last week but could fall further in the weeks and months ahead, according to analysts at BofA Global Research, who say it’s the most vulnerable among major currencies to a recovery in U.S. bond yields.

While the prospect of eventual changes to Federal Reserve (Fed) monetary policy settings have been on the radar of investors for some time, U.S. bond yields had declined during recent months as the market appeared to judge that any action from the bank was unlikely to actually materialise.

But perceptions appear to have shifted lately and most palpably in the week since last Wednesday’s Institute for Supply Management services sector PMI hinted of a renewed acceleration by the U.S. economy early in the third quarter, a notion which was encouraged further by last Friday’s bumper non-farm payrolls report that showed the U.S. recovering close to a million jobs from the coronavirus for a second consecutive month.

Now, with the job market clearly closer to having achieved the milestone target of “substantial further progress” in the direction of full employment, a possible September announcement of plans to taper the Fed’s $120BN per month quantitative easing programme has never been more likely and after months of calm the American and global bond markets are beginning to take notice with implications for the Swiss Franc.

“A clear pattern is emerging and, in our view, should the trend in global fixed income continue, then CHF stands to be the biggest laggard in G10 FX,” says Kamal Sharma, a strategist at BofA Global Research.

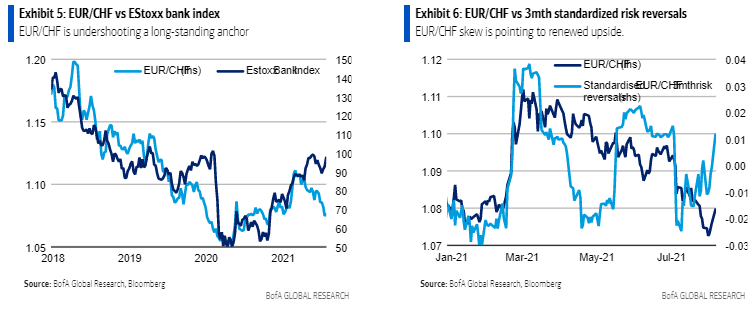

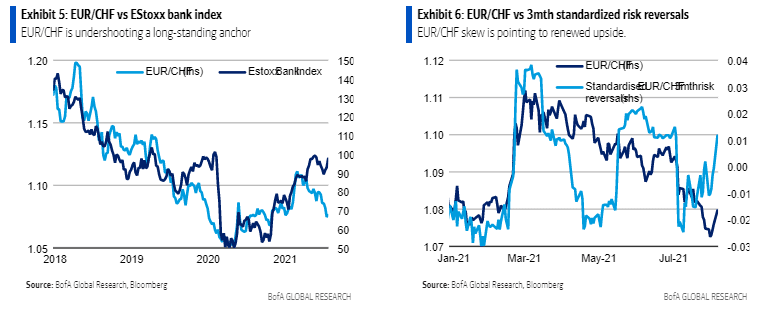

Above: BofA Global Research graphs showing EUR/CHF path implied by signals from the options market and European banking stocks.

“Both charts would suggest EUR/CHF could correct back towards the 1.10 level but do not suggest sustained outperformance beyond these levels unless associated with accompanying outflows from Swiss assets markets. Our preferred focus would therefore be lower CHF vs high-beta currencies and vs USD,” Sharma writes in a recent note.

While Sharma and BofA Global Research colleagues say a EUR/CHF recovery toward 1.10 could be in the pipeline, expectations of greater declines relative to “high beta” currencies mean the more meaningful moves are likely to be against those such as the Norwegian Krone, New Zealand, Australian and Canadian Dollars as well as, and possibly to a slightly lesser extent, Pound Sterling.

Switzerland has the lowest official cash rate in the world and so also some of the lowest bond yields, which leaves the Franc ever vulnerable to increases in interest returns paid to holders of other countries’ debts, which is a neat explanation for much of the recent increase in USD/CHF.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“The Swiss National Bank (SNB) has steered a consistent path for some time and latest FX developments are unlikely to shift its narrative,” Sharma says. “If the past week's stabilization in yields is the precursor to further gains, we believe CHF is the most vulnerable currency in G10 to a yield reset.”

Almost all Dollar rates have risen in the last week in tandem with an upturn in the all-important two-year U.S. government bond yield, which rose by almost a third to 0.22% in the week to Tuesday, prompting the USD/CHF exchange rate to rise more than 2% from near to its lowest levels since June when the Fed first began to signal that it could look to make adjustments to its QE and interest rate policies sooner than previously suggested.

The only U.S. Dollar decline seen within the G10 contingent of major currencies during the last week was against the New Zealand Dollar, which has itself benefited of late from mounting expectations that the Reserve Bank of New Zealand (RBNZ) could lift its own interest rate as soon as August 18.

Above: USD/CHF shown at daily intervals alongside GBP/CHF, EUR/CHF and 02-year U.S. bond yield (blue line).

“The franc continues to trade pretty poorly with EURCHF and USDCHF both having solid days yesterday. The cross seemingly found a base at 1.0720 last week after being relentlessly heavy for the past month and to the confusion of many,” says an unnamed trader on the London FX desk at J.P. Morgan, in a morning desk commentary.

“Needless to say USDCHF has been a big beneficiary of the recent shift in Fed speak/US data and we are challenging the downtrend from the YTD 0.9470 highs as I type. We are running modest USDCHF longs into US CPI tomorrow, with 0.9275 the next level topside,” the note reads.

While a major FX underperformer in the last week Switzerland’s Franc had previously been an outperformer during the period when U.S. government bond yields were declining which, when combined with elevated levels of inflation expectations, had eroded their real-terms yield offering to investors.

Many analysts have connected those declines to either earlier doubts about whether the Fed would really be likely to announce changes to its monetary policies any time soon, or to the recent momentum of the coronavirus across large parts of Asia.

It’s possible that both were factors in driving bond yields lower and the Swiss Franc highs, and is also possible if-not likely that global economic headwinds emanating from Asia could see some element of demand for the safe-haven Franc lingering and ultimately serve to temper its declines.

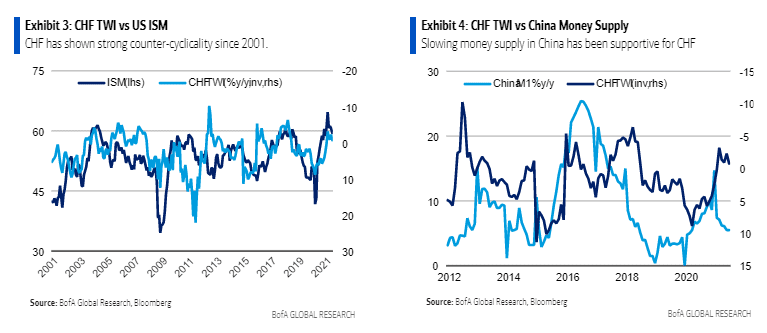

“If yield compression has indeed been driven by a re-pricing in global (particularly China) growth prospects, then the move in CHF makes more sense,” BofA’s Sharma says. “Though the recent turn must be seen in the context of the systematic decline, the pick-up in real yields has weighed on CHF to the extent that Swissy has been the biggest underperformer in G10 on the week”.

Above: BofA Global Research graph showing an inverted, or upside down, Swiss Franc in overall trade-weighted terms set against the level of the U.S. ISM composite PMI survey index (left) and changes in Chinese money supply.