The price of steel may have reached a cycle high which means the Australian Dollar may be at risk of impending weakness.

If the price of wine went up you would expect grapes to get more expensive.

Likewise, a rise in the price of steel would be expected to make iron ore more expensive, since steel is made primarily from iron ore.

This appears to be the logic underpinning Westpac Analyst Robert Rennie's view of the market since he argues that the surge in steel prices caused by data showing falling stockpiles will probably drag iron up with it.

“As long as these super high steel prices remain in China, it’s hard to generate a scenario where iron ore can fall much,” says Rennie.

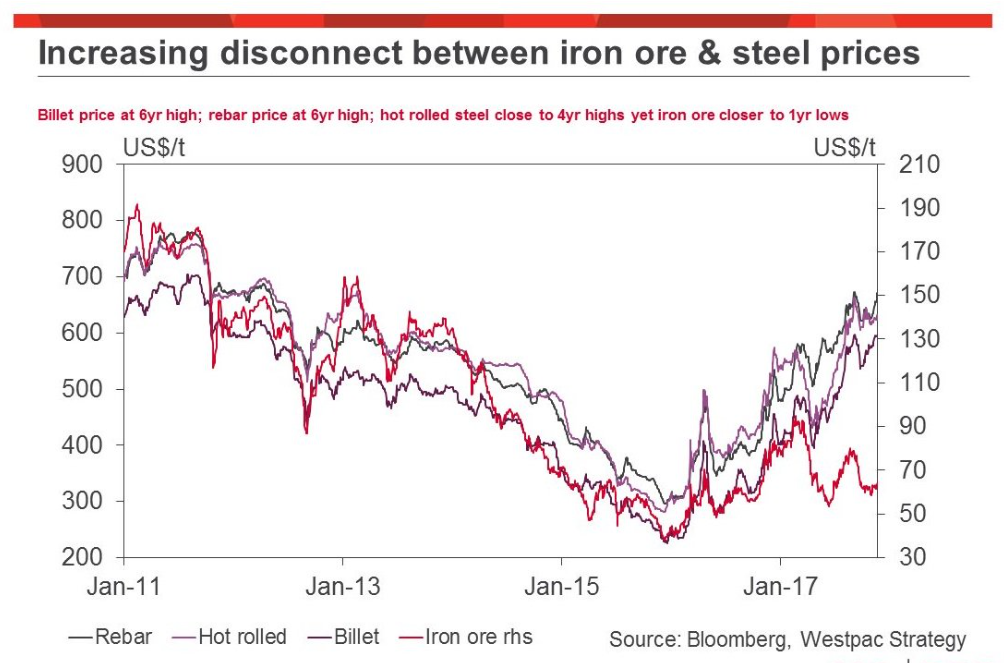

Rennie's chart below featured on Business Insider Australia, appears to show in not so many words a compelling correlation between the price of iron and steel: "Rebar", "Hot-rolled" and "Billet" being the names of different types of steel.

The chart shows that more recently there has been an increasing disconnect.

The invariable inference made by Rennie is that iron will probably rise to close the gap with the rising price of steel.

Indeed over recent days, iron ore has risen and seems to be recoupling again, but hwo much higher can it go?

Last of the Summer 'Iron'

Compelling as Renie's line of argument may be, further evidence from Liberum Analyst Richard Knights, suggests a more complex set of circumstances underpinning the iron and steel market which indicates iron will probably not in fact not rise to catch up with the price of steel - but they will probably both fall.

The surprise fall in steel inventories which led to steel prices rising was, in fact, a seasonal aberration - usually in winter steel prices fall as inventories steadily rise because demand - primarily from the construction sector - slumps.

The last set of inventory figures may have been unusual, because of the impact of the closure of 15-20% of Chinese steel capacity for 4 months, but this is probably a one-off and the fall in inventories is not expected to last.

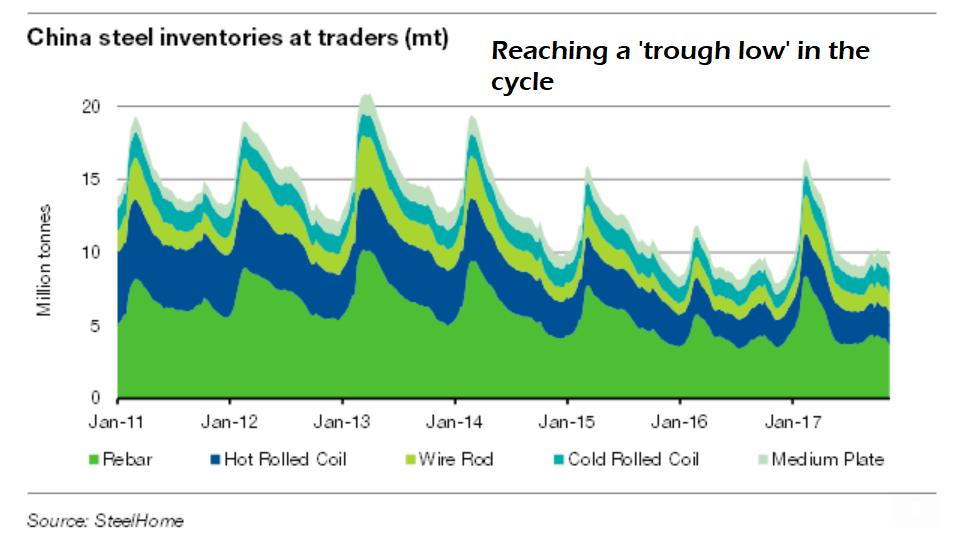

Using data sampled from trader inventories on information website SteelHome, Liberum manages to come up with what they argue is a good estimate of total steel inventory levels in China.

The inventory level charted over several years shows a strong seasonal cyclical pattern, which indicates inventories often reach a trough low just before January.

The most recent level strongly corresponds with the level of trough lows in previous years suggesting inventories may have reached a cycle low and are therefore unlikely to fall any further, which also means steel prices are also unlikely to go any higher.

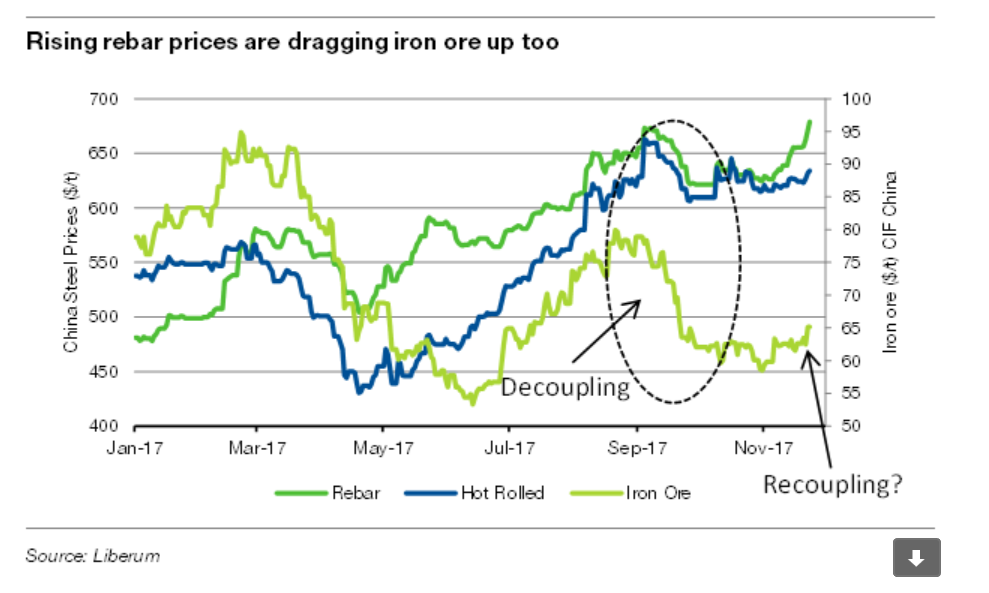

"The apparent tightness in inventories is dragging rebar prices higher again, taking iron ore with it. If this relationship holds, there is clearly scope for more upside for iron ore prices, but we don't see it as sustainable," says Knights.

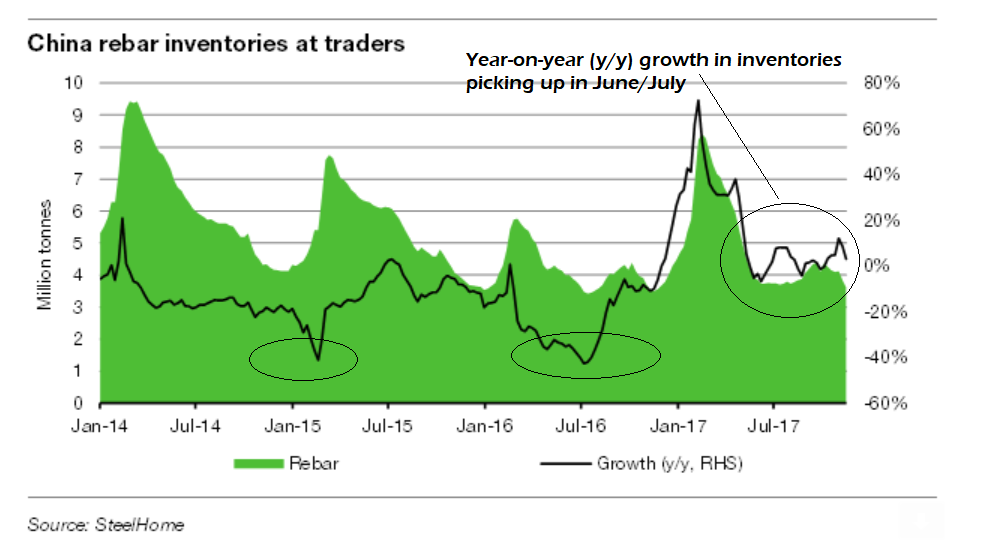

Indeed a close up of the inventory cycle for 'Rebar' the primary steel product, overlaid with a black line showing the year-on-year growth rate in inventories, indicates a substantial lift in growth most recently, which could be an early warning of more upside in inventories/downside in prices.

Slump in Imports

Liberum's Knights also notes that at the same time as steel is climbing and iron just beginning to look like it might be catching up Chinese port data is showing a puzzling collapse in iron ore imports into China of a magnitude equivalent to a third of total imports into the country.

"While (steel) mill profitability is rising, demand also appears to be cratering. The latest weekly ports data from Global Ports shows an 8mt decline in Chinese iron ore imports - equivalent to a drop of around a third of Chinese seaborne demand, or China's entire import demand for low-grade iron ore," says Knights.

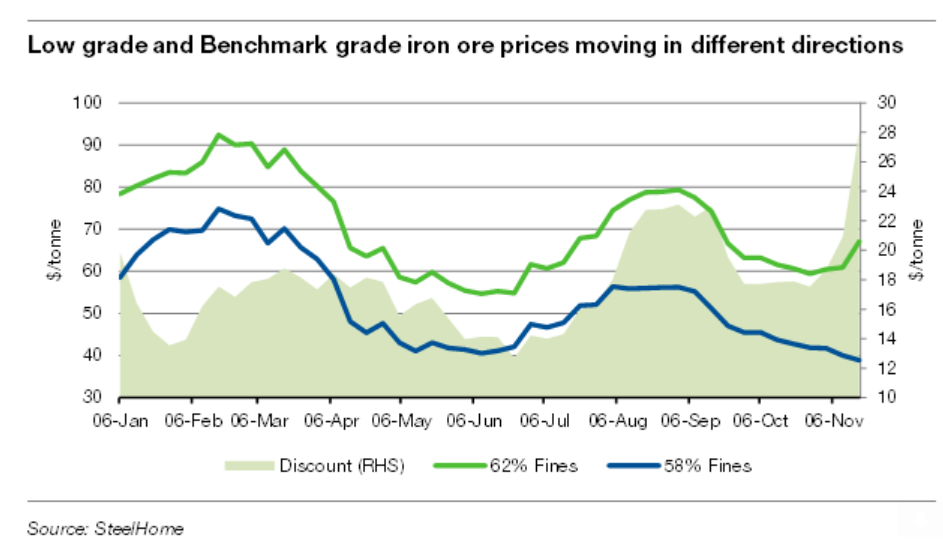

One explanation of the fall in iron ore imports may lie in the divergence between the price of high-grade iron ore (62% purity) which has risen in an attempt to close the gap with rising steel lately, and low grade iron ore (58% purity) which has continued falling, widening the disconnect with steel prices.

Given low-grade prices are falling whilst higher grade are rising and the fall in imports is about equivalent to the total level of low-grade iron imported into China the drop in imports may be mainly imports of low-grade ore.

"We estimate Chinese low-grade imports are around 250-300mt per annum. Winter closures are expected to reduce steel demand by c.40-60mt over 4 months, or 180-270mt per anum in iron ore terms. In other words, the potential reduction in demand is almost equivalent to China's total demand for low-grade iron ore," says Knights.

This isn't actually surprising when you consider that the Chinese government has been incentivizing the use of higher grade iron ore because it is less polluting to the environment.

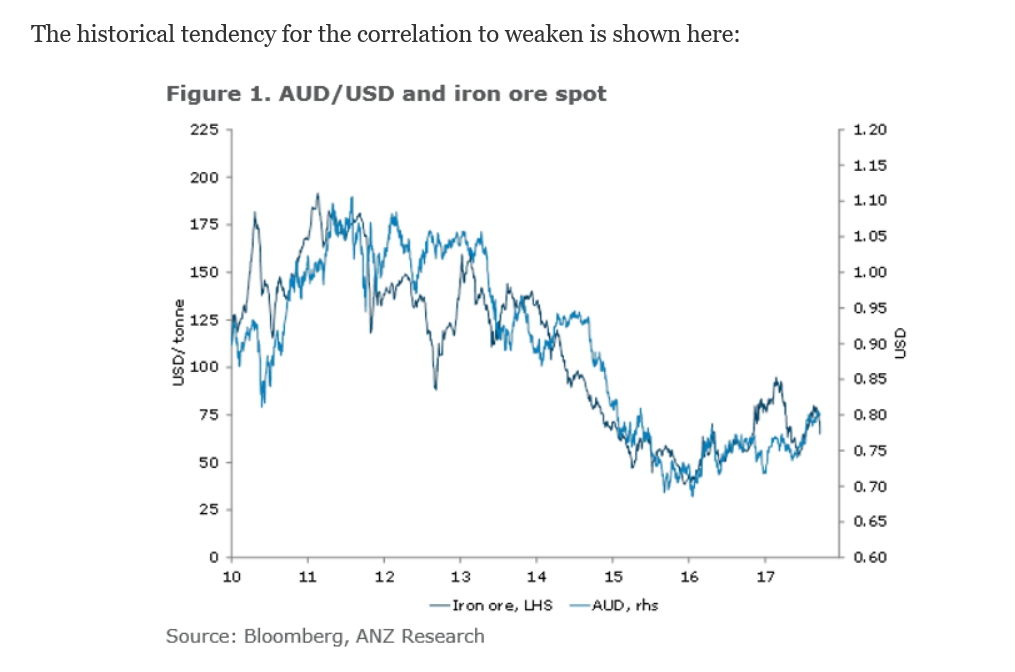

Implications for the Australian Dollar

It is not always possible to draw a link between iron ore prices and the Aussie Dollar even though iron ore is Australia's biggest export.

The chart below shows whilst there is a correlation it is rather haphazard at times.

Nevertheless, what is significant in this particular case is that most of the iron ore from Australia is high grade and originates from the mineral Hematite.

Australia is, therefore, less likely to be vulnerable to the sudden fall in Chinese demand low-quality ore, which is more likely to hit exports from India.