The Pound continues to struggle to make meaningful headway against the Australian Dollar and we are inclined to expect further declines in GBP/AUD over coming days but are wary of a packed data and events calendar.

The second week of October was a good one for the Pound which managed to gain against the group-of-ten of the world’s largest freely-traded currencies.

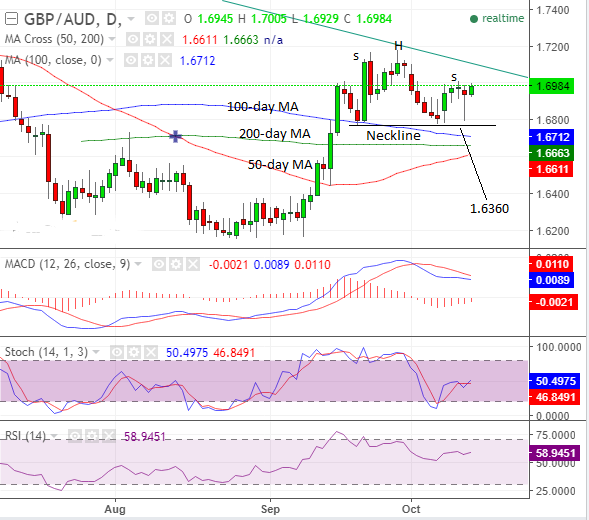

However, gains against the Australian Dollar were hard-won with a mere 0.06% gain being recorded once markets closed on Friday where the exchange rate was left at 1.6833 suggesting two currencies vying for momentum.

Richard Perry, a technical analyst with Hantec Markets in London has studied the GBP/AUD charts recently and argues recent price action is suggestive of the Australian Dollar holding the advantage in the near-term.

“Another test of the key near-term support at 1.6775 shows how the market is forming a four-week reversal pattern, which currently looks to be a well-defined head & shoulders top," says Perry.

Head-and-shoulders tops are composed of three peaks, with the central one the highest (the 'head'), and the two either side slightly lower but of a similar height (the 'shoulders').

“They occur at the end of uptrends and are very bearish signifiers,” notes Pound Sterling Live's technical analyst Joaquin Monfort.

"The momentum indicators are already tracking lower with the RSI showing a series of lower highs over the past few weeks, the MACD lines in decline and the Stochastics also turning back lower again," adds Perry eyeing further evidence of the potential for GBP/AUD downside in the near-term.

Monfort meanwhile notes a trend-line is likely to present a tough obstacle for any strength in GBP/AUD to overcome.

“For confirmation of more upside, we would ideally wish to see a break above the current highs at 1.7183, which would lead to a continuation up to an initial target at 1.7400, followed by a subsequent target at 1.7640 and the May highs,” says Monfort.

A failure to break above the trendline is of course bearish as it implies the longer-term trend of decline remains well and alive. The technical charts therefore favour the Aussie Dollar over coming days, but much will of course rely on the outcome of week’s data releases.

Australia: Watch Labour Market Data on Thursday

Tuesday sees the release of the minutes to the Reserve Bank of Australia's most recent policy decision held on October 3. An initial statement release by the RBA following the meeting knocked the Aussie Dollar as mention of the currency's recent strenght was made.

Will the RBA drill down further on the currency issue? If so, then further weakness might be likely. However, we believe the message is out and incorporated in the currency's valuation so would be surprised if any notable moves were to emerge.

Rather, markets will be combing the minutes for hints of when the RBA intends to next raise - or lower interest rates. Currently, expectations are for a move to be made in 2018 and we would expect the RBA to communicate that they remain focussed on economic data when it comes to decision making on rates.

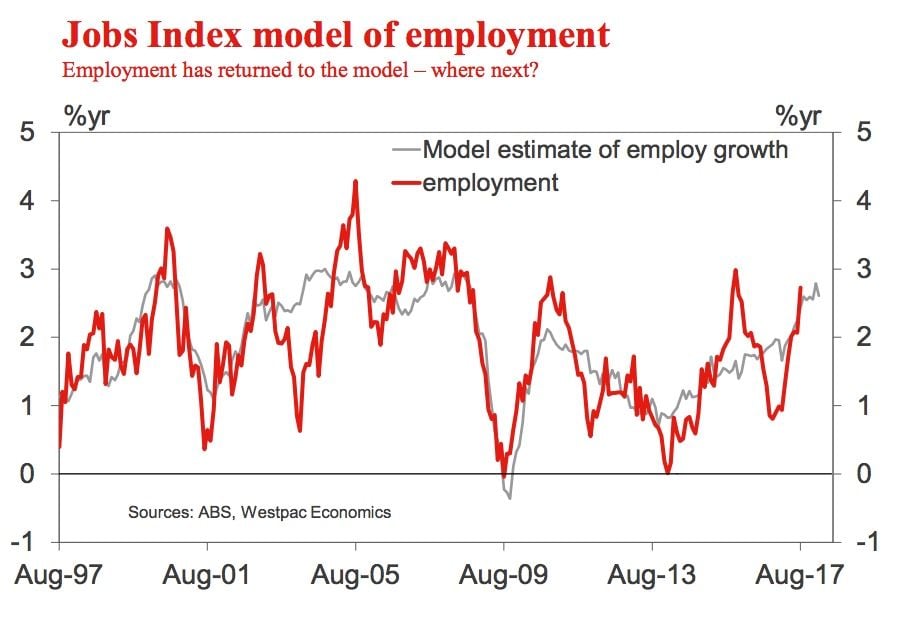

With this in mind, the highlight in the Australian Dollar’s calendar for the week is the delivery of employment data for September on Thursday, October 19.

The headline number to watch will be the employment change - markets are expecting a reading of +15K, down from the previous month’s +55,2K.

“The leading indicator including our preferred Jobs Index all point to ongoing robust demand for labour. We are also looking for annual growth in employment to overshoot the Index through late 2017 and into early 2018 as it rebounds from an undershoot during late 2016 early 2017,” says an economic preview note from Westpac ahead of the release.

Westpac are forecasting a reading of 25K, which if correct would certainly play positive for the Aussie Dollar.

The unemployment rate is forecast to read at 5.6%, unchanged on the previous month.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

The Pound: Data Steps Forward, Politics Takes a Step Back

Politics have been the key driver of Sterling this month - in the first week of October Prime Minister Theresa May’s position as leader of the country was put into doubt during the Conservative Party Conference and the second week saw the completion of the crucial fifth round of Brexit talks.

May survived and while no major breakthrough in Brexit talks have been reached, there are a number of hints that a breakthrough is likely before the turn of the year.

But the drivers of Pound Sterling are expected to move away from politics as we progress through mid-October.

“Expect the narrative for GBP to slowly shift towards the November ‘Super Thursday’ Bank of England meeting,” says Viraj Patel, an analyst with ING Bank N.V. in London. “Here we see upside risks as the Bank are not only likely to hike by 25bp, but the risks are that Governor Carney signals that this is more than a ‘withdrawal of stimulus’ hiking cycle.”

At present markets are forecasting a 0.25% interest rate rise to be delivered in November, commensurate with the communications for such a move set out by the Bank of England and its officials at various points in September.

The Bank suggest an interest rate rise is needed to ensure inflation does not runaway - it is already closing in on the 3.0% level and is thus a full 1% above their mandated target level. By raising interest rates the Bank would be able to slow spending but higher rates also = a stronger Pound as foreign investors are attracted to increased yields in the UK.

Tuesday: Inflation Data, Bank of England's Carney to Appear before Parliament

The question being asked from the Pound’s perspective is whether further interest rate rises are likely beyond November. Much depends on the data out this week.

Inflation data is due on Tuesday, October 17 with headline CPI for September forecast to read at 3.0% on an annualised basis, up from 2.9% registered in the previous month. Monthly CPI is forecast to read at 0.3%, down from 0.6% seen previously.

If numbers come in above 3.0% this would indicate inflationary pressures in the economy are running above expectation and perhaps more than one Sterling-supportive interest rate rise is required in coming months.

The Bank of England is mandated with maintaining inflation as close to 2% as possible with the Monetary Policy Framework noting:

“If the target is missed by more than 1 percentage point on either side – i.e. if the annual rate of CPI inflation is more than 3% or less than 1% – the Governor of the Bank must write an open letter to the Chancellor explaining the reasons why inflation has increased or fallen to such an extent and what the Bank proposes to do to ensure inflation comes back to the target.

This could therefore be the week that Governor Mark Carney gets his pen out and sends a letter to Chancellor Philip Hammond.

Such a move would be symbolic, but by raising interest rates in November the Bank will be seen to be taking concrete actions in dealing with rising inflation.

Of course, were inflation to read below the expected 3.0% marker, the Pound could come under pressure this week, notable pressure if a big fall in inflation were reported.

Also on Tuesday, Carney himself will appear before members of Parliament’s Treasury Select Committee in which he will be grilled over recent policy decisions, and where he sees policy going over coming months.

“The session should provide clarity on how big a majority the MPC will have when it hikes rates in November as we expect – overly dovish tones from both could suggest a closer vote, but ultimately we think the BoE will hike,” says a note from TD Securities ahead of the event.

Wednesday: Watch Wage Data

But perhaps more important than inflation data itself, is data that tells us something about how inflation data will look in the future.

This is why labour market data from the Office for National Statistics on Wednesday, October 18 are key, and wage data specifically.

The average earnings index - with bonuses included - is forecast to rise 2.1%. A number greater than this would be seen as positive for the Pound as it would signal that domestic inflationary pressures are building. When pay packets increase, demand increases which in turn pushes up prices.

The Bank of England would view such a dynamic as evidence that further interest rate rises are required if inflation is to be contained. It also suggests a robust economy that can absorb one or two interest rate rises in coming months.

A beat of the 2.1% forecast by markets would therefore be good for the Pound, but a lower number would be negative for the currency.

Wage increases have been slow in coming as the productivity of the average UK worker remains constrained. The exact reason for this lack a lack of productivity is not yet fully understood, but only when we see strong increases in productivity will we likely see pay packets make jumps higher.

“Surveys broadly indicate that employers remain on a hiring spree, with the employment component of the Services PMI at a 19-month high. Meanwhile, there are reports of salaries being bid up amid labour scarcity, with the REC Report on Jobs finding that permanent salaries had risen at the fastest pace since October 2015,” say analysts at Investec in a note to clients.

We would suggest markets will be pessimistic heading into this data release owing to data out last week from the ONS which showed UK labour productivity, as measured by output per hour, was estimated to have fallen by 0.1% from Quarter 1 (Jan to Mar) 2017 to Quarter 2 (Apr to June) 2017 while over a longer time-period, labour productivity growth has been lower on average than prior to the economic downturn.

A beat on expectations would likely be the more surprising outcome and therefore the impact on Sterling - to the upside - would be greater. So watch for a decent rally in Sterling were the data to beat.

Thursday: The Health of UK Shoppers

The week of data ends off with the release of UK retail sales which are a key indicator of consumer confidence.

Markets are forecasting monthly retail sales for September to read at -0.2%m down on the 1.0% seen in the previous month.

So expectations are low here and a beat would certainly give Sterling a lift into the latter half of the week.

Friday: Politics Still With us, Watch EU Leaders Summit

While data will be key readers should remember that the EU leaders’ Summit on October 20 where Heads of State of the European Union will gather to discuss progress made on Brexit thus far.

We already know that it will be agreed negotiations are not ready to move on to discussions of trade.

But we have also noted reports that the EU could be willing to move on to talks in the near future were May to offer up some concessions. The Pound rallied last week on the news as it suggests the EU and UK are actually closer together on outstanding issues than initially expected.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.