Image © Adobe Images

The Australian Dollar was one of the bigger fallers in the advanced economy currency space in mid-week trade as losses lifted GBP/AUD to one-year highs while helping to paint an increasingly bullish picture onto the charts.

Australian Dollars were sold widely in Wednesday trade when the Euro, New Zealand Dollar and Norwegian Krone were the only advanced economy currencies to underperform the antipodean unit, which also rose against the South African Rand, Polish Zloty and Turkish Lira.

Wednesday's gains for GBP/AUD came amid widespread signs of risk aversion in global markets and followed losses in AUD/USD, which reached its lowest level since November as stocks and commodities came under pressure while government bond markets rallied.

"The data in Asia was not so good overnight with South Korea and Japan both missing lower by a wide margin on industrial production and the Chinese PMI prints coming in lower," says Brad Bechtel, global head of FX at Jefferies.

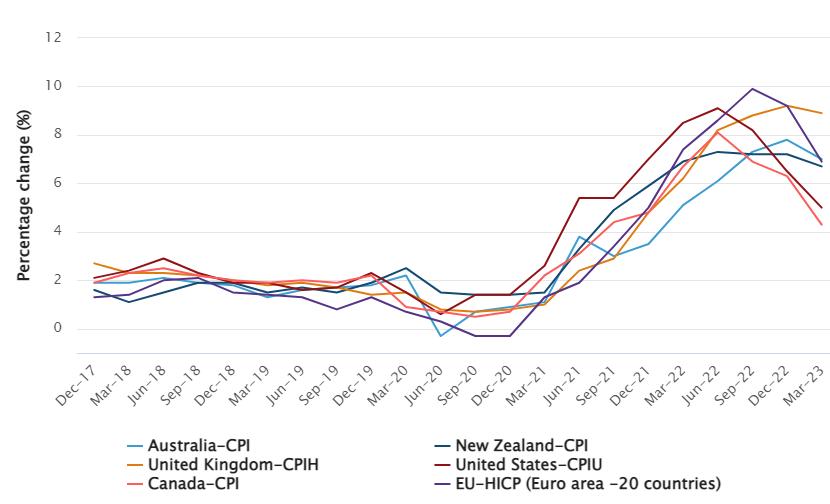

"Australian CPI also came in higher than expected, adding to the string of poor data in the region," he adds.

Above: Pound to Australian Dollar rate shown at daily intervals alongside AUD/USD and including Fibonacci retracements of early 2020 downtrend indicators of possible technical resistances for Sterling. Click image for closer inspection.

Wednesday's risk aversion followed a broad swathe of poor economic figures from across the Asia Pacific region beginning with falling industrial production and retail sales in Japan and South Korea, before culminating in a reported decline in Chinese manufacturing activity.

Notably, April's annualised decline in Korean industrial production approached the double-digits when coming in at -8.9% while Japanese retail sales reversed around a third of the gains reported over the year-to-date.

Meanwhile, decelerating manufacturing activity led the National Bureau of Statistics of China's industrial indicator to fall back to its January 2023 level.

All of the above are potentially symptomatic of high inflation, rising interest rates and moderating demand in advanced economies including Australia where on Wednesday inflation was reported to have reversed its March fall in April amid a pick up in other economic indicators.

"The risk around our forecast of a 4.1% cash rate in August has been tilted toward earlier and/or more action from the RBA. Today’s CPI data add to that risk, with inflation, construction work done and credit all consistent with higher interest rates soon," says Adelaide Timbrell, an economist at ANZ.

Source: Australian Bureau of Statistics.

Prices of transport, fuel, meat, seafood, non-alcoholic beverages, accommodation rents and financial services were the main contributors to April's uptick, while lesser increases in property prices, clothing, footwear, holidays, fruit and vegetables helped to restrain the annual pace of inflation.

But on a seasonally adjusted basis and once changes in prices of the most volatile items are excluded from the basket measured, inflation actually fell in April, continuing an earlier downtrend and leaving economists divided over what the data means for the Reserve Bank of Australia cash rate outlook.

"Our Australian economics team continues to expect the RBA to leave the cash rate on hold at next week’s June meeting," says Kristina Clifton, an economist and currency strategist at Commonwealth Bank of Australia.

"Financial markets are only pricing a very small chance of a June hike but have a 25bp hike almost fully priced by August. An eventual unwind of rate hike pricing can be a headwind for AUD/USD," Clifton and colleagues write in a Thursday research briefing.

The cash rate was raised to 3.85% on May 02 but expectations have shifted since then to suggest a high probability of an August increase taking the benchmark to 4% or more, while the RBA warned of a limited margin for error in relation to its forecasts for inflation.

Above: Pound to Australian Dollar rate shown at weekly intervals with Fibonacci retracements of early 2020 downtrend indicators of possible technical resistances for Sterling.

Updated RBA forecasts suggested this month that it's likely to take until 2025 for Australia's inflation rate to return to within the two-to-three percent target band, which would mean prices would have been growing at above-target rates for more than three years by that time.

Governor Philip Lowe also warned that further increases in the cash rate shouldn't be ruled out, and particularly if increases in workforce pay accelerated during the meantime, which is a widely recognised risk in light of increases in prices essential items like accommodation, food and energy.

Official figures have recently suggested a softening of Australian labour market conditions and moderating growth in wage packets, however, and this might act to reduce the risk of further increases in the RBA cash rate.

"What does this mean for the Reserve Bank? We continue to expect that the cash rate will stay on hold next week. In contrast, interest-rate markets have attached a higher probability to a rate hike after today’s inflation data," says Pat Bustamante, an economist at St George Bank.

"Today’s results make it particularly tricky to get an underlying read given the large impact of policy, seasonality in the data and many of the services prices that drove inflation over the March quarter (medical and hospital services, education, financial services) were not updated for April," he adds.