- GBP/AUD's bottom has potentially already been established

- With possible scope for stabilisation above 1.6327 up ahead

- Chance of recovery extending toward or perhaps above 1.70

- UK inflation, budget deficit outlook both important influences

- Australian economics & AUD/USD trend also key for outlook

Image © Adobe Images

The Pound to Australian Dollar rate has been highly volatile of late but there may now be a basis for thinking it's unlikely to fall any lower than 1.6327 from here and that its recovery from this week's all-time lows could potentially extend as far as, or perhaps even above 1.70 up ahead.

Sterling opened the new week with steep losses against many currencies including its antipodean counterparts and in price action that saw the Pound to Australian Dollar rate falling as low as 1.5911 during the Asia trading session on Monday before recovering the entirety of its declines by Tuesday.

"The move followed UK Chancellor Kwasi Kwarteng’s ‘budget’ where he announced tax cuts and spending increases, with a promise of more to come," says David Morrison, a senior market analyst at Trade Nation.

"The question now is whether we’ve seen the low for sterling, or if further weakness is likely. Certainly, the surge in gilt yields is a concern, particularly given how much the Truss government is going to have to borrow to meet its new spending commitments and tax cuts," Morrison said on Tuesday.

Monday's volatility appeared connected to Friday's budget-like announcement in which Chancellor Kwasi Kwarteng unveiled a range of policy commitments that are almost certain to require significant increases in government bond issuance while bulking up the budget deficit.

Above: Pound to Australian Dollar rate shown at hourly intervals alongside GBP/USD.

Above: Pound to Australian Dollar rate shown at hourly intervals alongside GBP/USD.

These went beyond the cancellation of tax increases planned by the prior government and were not limited to the simple provision of assistance relating to energy bills as they also included outright tax cuts as well as other giveaways, the announcement of which was followed by steep losses for Sterling.

"Calm returned to sterling during London trading as it retraced much of last Friday’s/early Monday’s weakness. The volatility, however, serves as a salutary reminder of the need to deliver credible policy, particularly in the current climate of high inflation and asset price weakness," says Brian Martin, head of G3 economic research at ANZ.

"Given the rise in borrowing needs (GBP71.2bn), UK market rates have risen. We expect policy rates to rise materially further (4.0%) but think the market’s view of 6.0% rates is too high. Sterling may therefore take some time to settle, while the government needs to boost fiscal credibility," Martin wrote in a Tuesday research briefing.

The subsequent price action in Sterling has prompted much discussion about "fiscal responsibility" among analysts and economists while coming at a time when high inflation has gotten the Bank of England (BoE) raising interest rates and looking to sell down its portfolio of UK government bonds.

But the Pound's declines for the year were already sizable even before Friday's budget while multiple increases in interest rates from the BoE have done little to keep Sterling exchange rates from falling in recent months.

Source: ANZ.

Source: ANZ.

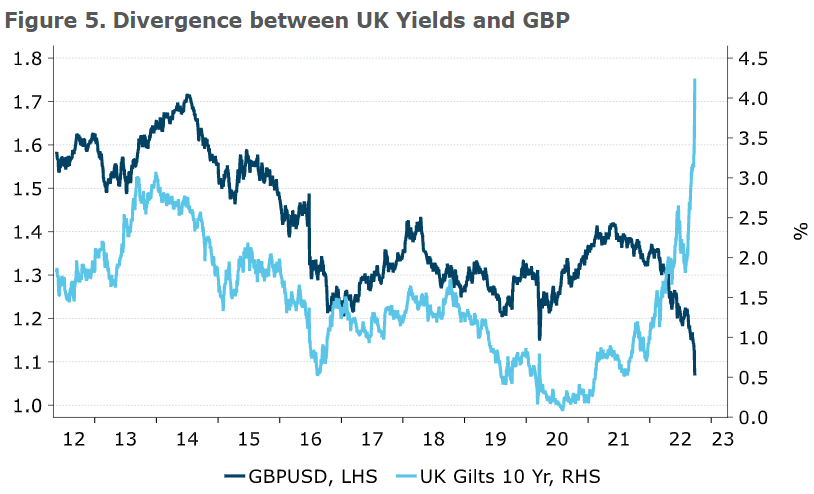

The following is nothing more than guesstimation but it's possible all of this is the result of insufficient returns offered to compensate for the risks of investing in Sterling bonds, which is potentially necessitating currency and bond price discounts that would explain the divergence between yields and the Pound.

That's been the working assumption of the author since roughly mid-month and is why it may now be possible to argue that the bottom has already been seen by many Sterling exchange rates including GBP/USD and GBP/AUD.

"It’s possible that the price action witnessed in GBPUSD on Friday and Monday was the cathartic moment for the re-pricing of UK risk premia we have been writing about," says Stephen Gallo, European head of FX strategy at BMO Capital Markets, in a Tuesday review of the outlook for the Pound.

"If so, the panic may be over. However, with an uncertain winter still ahead of us, our view is that there are still more downside than upside risks for GBPUSD during the 1-3M period in question," Gallo wrote.

At Monday's low of 1.0350 the main Sterling exchange rate, GBP/USD, had fallen by more than 23% for 2022 and was still trading just more than 20% lower for the period on Tuesday after having recovered above the 1.08 level.

Above: GBP/USD shown at 4-hour intervals alongside AUD/USD and with Fibonacci retracements of September decline indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

Above: GBP/USD shown at 4-hour intervals alongside AUD/USD and with Fibonacci retracements of September decline indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

To the extent that any of the Pound's recent losses really were a reflection of an attempt to find a new equilibrium offering sufficient risk-adjusted returns, the discount now offered by Sterling is very sizable and running at more than twice the overall rate of UK inflation in August.

As far as sufficient risk-adjusted returns were ever relevant, it could be argued that the sharp recovery seen in GBP/USD and GBP/AUD over the course of Monday and Tuesday is an indication of that new equilibrium already having been found, if not overshot by some distance.

The latter might be an especially pertinent point and one that would grow more relevant if it transpires that economists are right in thinking UK inflation has already peaked or is otherwise close to doing so, as this kind of development might argue for a lesser or narrower discount in the future.

"The UK government needs to be careful not to cause a vicious cycle where GBP weakness increases imported inflation, which in turn encourages the BoE to increase interest rates even more," says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

"Even the market pricing steep increases in UK interest rates may do damage to the UK economy," Capurso and colleagues said on Tuesday.

Above: AUD/USD shown at daily intervals alongside GBP/USD. Click image for closer inspection.

Above: AUD/USD shown at daily intervals alongside GBP/USD. Click image for closer inspection.

In any case, GBP/AUD always tends to closely reflect the relative performance of Sterling and the Aussie when each is measured against the U.S. Dollar, which makes it possible to infer a number of things about the likely outlook for the coming days and weeks.

Assuming it's right to think GBP/USD is likely to stabilise above roughly 1.06 but that it could struggle to recover above 1.12 in the near future, then GBP/AUD may be likely to find itself supported above 1.6327 from here.

It may even have scope to rise back toward, or perhaps even above 1.70, although all of these numbers make the completely unrealistic assumption that the Australian Dollar remains around its Tuesday level against the U.S. Dollar.

This leaves a lot about the GBP/AUD outlook to be determined by Australian economic developments and other international factors in the days and weeks ahead although it's possible, if not likely, that much of the trade will still take place somewhere within roughly the 1.6327 to 1.70 range.

That range could break on the downside in the event of a sharp rally in AUD/USD, although it would likely take a very sizeable depreciation of AUD/USD in order to lift GBP/AUD by much above the 1.70 handle in the immediate period ahead.

Above: AUD/USD shown at weekly intervals alongside GBP/USD. Click image for closer inspection.

Above: AUD/USD shown at weekly intervals alongside GBP/USD. Click image for closer inspection.