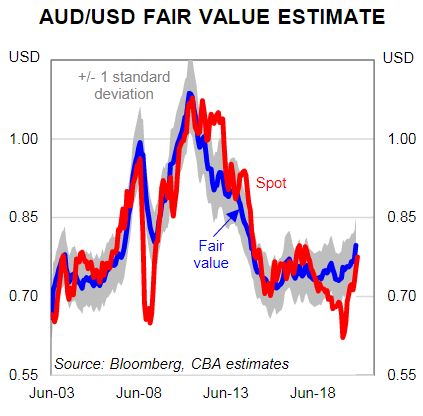

- AUD fair value range estimated at 0.74 to 0.85 by CBA.

- AUD/USD tipped for climb to 0.80, aided by commodities.

- But U.S. bond yield rally, virus both short-term risks to AUD.

Image © Desiree Caplas, Adobe Stock

- GBP/AUD spot rate at time of publication: 1.7546

- Bank transfer rate (indicative guide): 1.6932-1.7055

- FX specialist providers (indicative guide): 1.7283-1.7423

- More information on FX specialist rates here

The Australian Dollar is still fundamentally undervalued even after its forty percent rally from March 2020 lows, according to analysts at Commonwealth Bank of Australia (CBA), who say that surging commodity prices are lifting model-derived estimates of the currency’s underlying worth.

Australia’s Dollar was among the worst performing major currencies on Tuesday after softening in response to a sudden bout of risk aversion that’s thought to have been prompted by resurgent coronavirus infections in some parts of Asia and a sharp rise in American bond yields.

But the antipodean unit remained the second best performer for 2021 behind only the oil-linked Norwegian Krone and was still 42% above its March 2020 low against the U.S. Dollar after being supported in its recovery by rallying commodity prices.

“Fair value for AUD/USD continues to increase. We now estimate fair value for AUD/USD is in a range of 0.74 to 0.85, centred on 0.80. The recent surge in the iron ore price can underwrite further gains in AUD/USD to over 0.80 in our view,” says Joseph Capurso, a strategist at Commonwealth Bank of Australia.

AUD/USD was trading just above 0.77 on Tuesday and toward the lower end of the fair value range estimated by CBA, with almost five percent upside before the exchange rate reaches 0.80 and the middle of its equilibrium range.

Source: Commonwealth Bank of Australia.

Commodity prices have rallied ever more fervently since the advent of coronavirus vaccines prompted investors to price-in a global economic recovery that comes sooner rather than later to most parts of the developed world, lifting the commodity-linked Australian Dollar in the process.

Rising commodity prices are a headwind for the Pound-to-Australian Dollar rate, which many Australian lenders including CBA expect will trend steadily lower in 2021. Although none are as bearish as analysts at TD Securities, who said last week that GBP/AUD could fall to 1.70 in the months ahead as Sterling lags commodity currencies due to their stronger fundamentals.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“Commodity prices are the major driver of fair value in our equation. Iron ore prices (62% FE Fines) increased by over 30% since the start of December,” Capurso says. “AUD/USD fair value would likely have lifted further if Australia-US 2 year OIS interest rate differentials had not turned negative recently.”

Further increases in U.S. government bond yields would pose as a short-term headwind to the Australian Dollar because they could eat away at the value implied by 2 year AU-U.S. overnight indexed swaps as well as that which comes from commodity prices.

Above: 10-year U.S. government bond yield with Fibonacci retracements of 2020 fall and 30-year yield (blue).

U.S. government bond yields have surged since Federal Reserve policymakers began to suggest last week that a tapering of their $120bn per month quantitative easing programme could come sooner than markets give credit for, with yields stepping up more strongly after last Wednesday’s Georgia State election handed the Democratic Party a majority in the U.S. Senate.

That gave the former opposition an absolute congressional majority and the incoming President Elect Joe Biden greater freedom to implement his agenda.

"A rebound in the USD, along with a rally in US treasury yields has put renewed pressure on spot gold prices, with the market now trading well below US$1,850/oz," says Warren Patterson, head of commodities strategy at ING. "Rising yields will make it more challenging for the yellow metal to trend higher, however much will depend on inflation expectations and what this means for real yields. Meanwhile, last Friday Joe Biden called for fiscal spending and said, ‘it will be in the trillions of dollars’. Hopes for spending in clean energy and infrastructure will likely increase investor appetite for metals."

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Yields have risen because of both expectations of even greater U.S. government spending after the election and due to suggestions by the Fed that it may soon pull back from the market. This is notable because 10-year bond yields represent the ‘risk free’ rate that is one of several inputs used by analysts to determine the fair or fundamental value of stocks.

When risk free rates rise, so-called risk premiums fall and this results among other things in a situation where corporate earnings have to grow even faster in order for shares to justify their existing valuations.

"The NASDAQ Equity Risk Premium is 360 bps vs. a “risk free” premium of -100 bps in real yield of 10-year US treasuries. The negative real yield is how the US forces us all to “play the game” of being long the stock market, as it’s the only asset right now with positive risk premium we can harvest," says Peter Garnry, head of equity strategy at Saxo Bank. "If you are a financial planner the only way to access positive return is in the equity market."

Above: AUD/USD rate shown at daily intervals alongside S&P 500 index futures (blue).

Above: AUD/USD rate shown at daily intervals alongside S&P 500 index futures (blue).

Without the prospect of faster corporate earnings growth share prices could fall as they did to open the new week, leading risk-sensitive currencies like the Aussie to also fall while safe-havens like the U.S. Dollar rise.

"Dollar strength continued as softening risk appetite and higher relative yields led outperformance. In the near term, risks for the AUD are balanced with global equities and US yields remaining key," says David Plank, head of Australian economics at ANZ. "These moves should see local rates markets open to some selling pressure. Any new lockdowns in China amid a new outbreak of coronavirus cases could lead to a risk-off tone across commodity markets."

Faster corporate earnings growth may be unlikely in a world and global economy that is for the time being threatened by the prospect of either renewed or prolonged secondary ‘lockdown’ due to a resurgent coronavirus.

Coronavirus infections have risen strongly in Europe and North America in 2021 but its the accelerated pace in China and Japan that could be of more concern to investors given how China’s superstar economic recovery has been the most crucial for sustaining the rebound in commodity prices. This and the rally in bond yields pose a risk to the Aussie although beyond the short-term the antipodean unit is among the most likely beneficiaries of the anticipated global recovery.

“Real 10‑year yields remain negative. Negative real US yields will be a drag on USD over the medium‑term,” CBA's Capurso says. “USD may rally modestly further in the near term but we expect the rally to be brief and contained. First, the global economy is entering the “sweet spot” of a growth upturn with low inflation. The global economic recovery will be supported by greatly improved prospects for increased fiscal stimulus in the US because Democrats will control both houses of Congress. Second, USD is modestly overvalued.”