Image © Adobe Images

- AUD upside limited this week says CBA, as global factors weigh.

- Trade tensions and Federal Reserve policy both on AUD's radar.

- Forecasts of AUD uptrend next year scrapped by Commerzbank.

- AUD now seen drifting lower through 2020 as RBA policy hurts.

The Australian Dollar softened at the beginning of the new week even in spite of a broad rally in so-called risk assets during the morning session on Monday, while some analysts say upside will be limited in the days ahead and others are cutting their forecasts for the Antipodean currency through the end of next year.

Australia's Dollar was left lagging behind many of its developed world rivals Monday even as stock markets and commodity prices rose the world over in response to President Donald Trump's apparent rethink of a Chinese tariff package announced earlier this month. The Aussie challenged the top of its August range last week in response to President Trump's change of heart, but some local analysts are suggesting those are about all the gains the Antipodean unit will see in the short-term.

"AUD/USD upside is limited despite AUD/USD stabilising last week, and lifting on a trade‑weighted basis. Slowing global momentum and heightened economic risks will continue to weigh on the commodity‑sensitive currency," says Richard Grace, head of FX strategy at Commonwealth Bank of Australia (CBA). "Downside risk to global growth remains high and are USD supportive especially against AUD and NZD. US‑China trade tensions could get worse before getting better, a hard‑Brexit cannot be ruled out and global policymakers may react too slowly or timidly to slower growth momentum."

President Trump's says some new tariffs that were due to be applied to Chinese goods from September 01 will now not go into effect at all and that implementation of just more than half of the new levies will be deferred until December 15, suggesting that yet another escalation of the trade conflict and overall hostility between the world's two largest economies could be avoided. But with that decision coming barely more than a month after another tariff truce was agreed at the Osaka G20 summit in Japan, market confidence in the durability of the latest deescalation has been low from moment one.

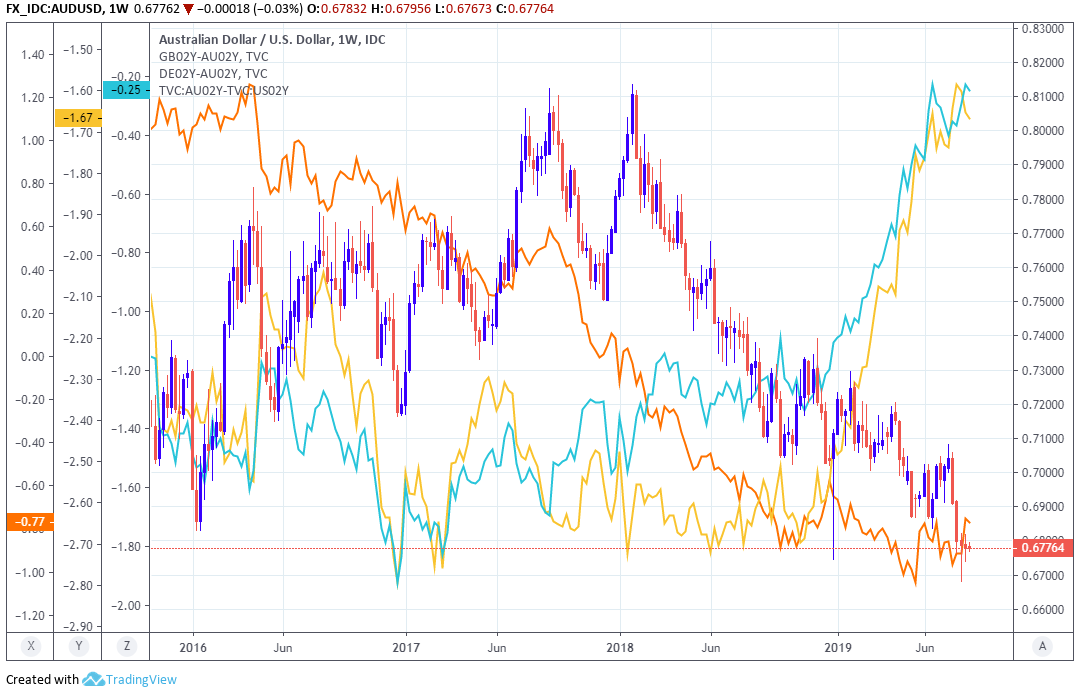

Above: AUD/USD and yield spread relative GBP (green), German (yellow) and U.S. bonds (orange).

The Aussie has been among the hardest hit by the U.S. trade war due to the extent to which the economy and currency are exposed to China, which is a significant extent given the nation's largest business is in commodities that are mostly sold to Chinese firms. This is why it outperformed last week.

However, confidence in the prospect of the U.S. and China reaching a durable truce or an actual resolution to the tariff conflict is low and the Aussie now has other problems too, not least of all Reserve Bank of Australia (RBA) interest rate policy and the impact it's having on the attractiveness of the Aussie to international investors.

The RBA has cut its interest rate twice this year in the hope of lifting the consumer price index back within the 2%-to-3% target band and is expected to reduce the cash rate on at least one more occasion before the year is out. This has already seen the yield on Australian government bonds fall beneath that of comparable paper issued by the U.S. government, while reducing the premium traditionally offered by Aussie fixed income assets relative to other G10 peers.

"The escalation of the trade conflict between the USA and China changes everything. Also for the AUD. We now expect lower AUD-USD levels for the time being and have revised our forecast accordingly," says Esther Reichelt, an analyst at Commerzbank, in a review of the bank's Australian Dollar forecasts.

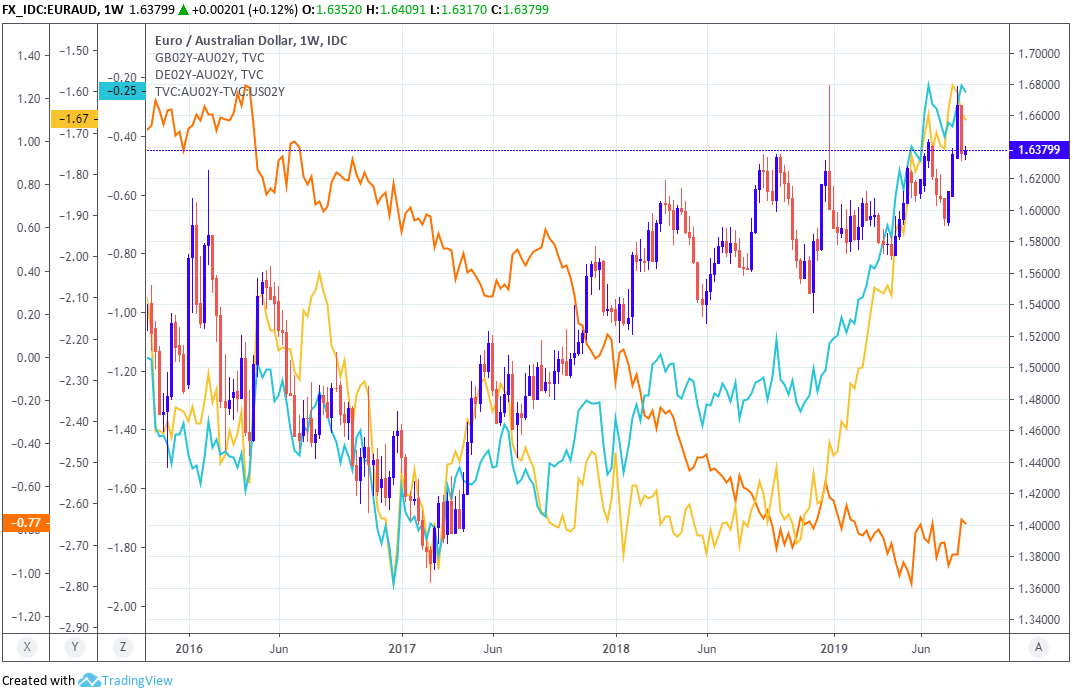

Above: EUR/AUD and yield spread relative GBP (green), German (yellow) and U.S. bonds (orange).

The RBA's 2019 cuts have all-but eliminated the incentive for investors to hold Aussie assets instead of those available in the U.S., and they're fast eating into the incremental returns still offered by the Aussie relative to other currencies. But markets are still anticipating even further reductions to the cash rate. Governor Philip Lowe said earlier this month it wouldn't be "entirely unreasonable" to expect an "extended period" of low rates, or further cuts from the RBA if the outlook begins to warrant it.

Given Australia's large commodity trade and the sensitivity of materials prices to the global growth outlook, another knock for the world economy could be enough to prompt further action from the RBA, and such a knock could come simply if U.S. and Chinese leaders fail to promptly agree a lasting resolution to tariff fight. Another trigger for an additional rate cut could come if the Australian jobs market weakens enough for the unemployment rate to rise further from its recently-increased level of 5.2%.

Changes in rates are normally only made in response to movements in inflation, which is sensitive to GDP growth, but impact currencies because capital flows tend to move in the direction of the most advantageous or improving returns. Those flows tend to move in the direction of the most advantageous or improving returns, with a threat of lower rates normally seeing investors driven out of and deterred away from a currency.

"Contrary to what we originally expected, the RBA could thus relax its monetary policy to a larger extent than the Fed. Accordingly, the Australian dollar is likely to remain on the defensive against the US dollar for the time being, which is why we now expect the downward trend in AUD-USD to continue," Reichelt says.

Above: GBP/AUD and yield spread relative GBP (green), German (yellow) and U.S. bonds (orange).

Pricing in the overnight-index-swap market implied on Monday, a December 03 cash rate of just 0.57%, which is almost a full 50 basis points below the benchmark's current 1% level. The RBA has cut in increments of 25 basis points on two occasions so far.

The further two cuts anticipated by the market for 2019 are equal to the reductions in the U.S. Fed Funds rate that are also envisaged by investors, but if delivered would result in a situation where the RBA will have cut on four occasions before year-end when the Federal Reserve will have only reduced its cash rate three times.

This would still leave U.S. cash rate at 1.75%, which would mean the gap between benchmark interest rates in the U.S. and Australia becomes even wider later in 2019 than it was at nadir of the Aussie Dollar downtrend seen earlier this year. As a result, Commerzbank and others are forecasting fresh losses to hit the Aussie sooner or later.

"Interest rate cuts by the RBA and a highly uncertain outlook for China will continue to put downward pressure on the AUD. This is particularly true against the euro, as we see only very limited options for further expansionary measures by the ECB, which is unlikely to be sufficient to weaken the euro in the long term. On the other hand, the depreciation against the US dollar should come to an end at some point," Reichelt says.

Reichelt forecasts the RBA will in fact cut the cash rate to a record low of 0.5% before the year is out and that the AUD/USD rate will fall to 0.66 by the end of December, before declining to 0.64 in time for the end of next year.

Meanwhile, the Euro-to-Australian-Dollar rate is seen rising from 1.63 to 1.70 this year and to 1.88 by the end of 2020. The Pound-to-Aussie rate is seen rising from 1.78 to 1.87 by year-end and all the way up to 2.09 next year. Those are all significant downgrades from Commerzbank's earlier forecasts.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement