Image © Adobe Stock

- Economics headwinds abating

- Deloitte says H2 2019 and H1 2020 to show improved growth

- OECD business cycle indicator concurring

Stronger employment data in July took the markets by surprise on Thursday and suggests the Australian economy may be shaking off the funk which has kept expectations subdued over recent months.

In fact, it may be the first sign of a much brighter period of growth in the second half of 2019 and into 2020, analysis from global accountancy firm Deloitte, and certain business cycle indicators.

With an upturn in the economy the Australian Dollar is also likely to partake of the improved outlook and strengthen as well.

On paper the outlook for the Australian economy does not look promising: if there was a country that was first in the firing line when it comes to trade war fallout it would be Australia - it is not for nothing the Australian Dollar is known as a proxy for the Yuan and the country has huge exposure to China.

A dramatic fall in house prices and fear of the fallout from a housing bubble was the main economic concern, but then weakness in Australia’s usually strong labour market and the global trade-induced slowdown increased the negativity.

"The AUD has been short on luck. A weak external environment pushed it lower in 2018, but that recovery was not enough to lift it in 2019, as the domestic policy environment turned dovish," says Rahul Khare, FX Analyst at ANZ.

Deloitte however expects the Australian economy to have much easier ride in the second half of 2019.

Tthe Reserve Bank of Australia (RBA) has been easing aggressively to protect growth and has cut its base lending rates twice this year, bringing the official cash rate down to a record low of 1.0%, and whilst it did not see the need to cut again at its last meeting, all major bank analysts expect at least 1 if not 2 more cuts this year.

“Australia’s economy slowed in 2018–19 due to a housing downturn and a severe drought. But economic growth is expected to pick up on the back of monetary and fiscal stimuli, which is likely to boost household income and consumer spending,” says David Rumens at Deloitte Australia.

The main cause of the slowdown - the fall in house prices - is set to turnaround in H2, says Deloitte.

For starters, the 0.5% cut in interest rates will make mortgages cheaper and then there is all the new regulatory help which has been put in place to support the market. The Australian Prudential Regulation Authority (APRA), for example, has helped increase access to credit for both owner-occupiers and investors.

The re-election of the Liberal government of Scott Morrison has also helped the outlook for the housing market as the labour opposition had threatened to increase capital gains tax further pressuring market prices. This threat, however, has been averted.

Housing is not the only area of the economy Rumens is optimistic about: an injection of fiscal stimulus in the form of A$1000 tax rebates to almost 5 million Australians and A$500 to another 5 million will provide a welcome boost to household incomes and spending.

“Tax cuts and lower mortgage repayments will help boost household disposable incomes, which should support consumer spending through the second half of 2019 and well into 2020. Further, the solid pipeline of state infrastructure spending will support project investment and employment in the construction sector, particularly across the east coast,” say the analyst.

Another driver of growth in 2019-20 is expected to be the all-important mining sector which is expected to show a renaissance in growth for the first time since the sector peaked in 2012. “This, in turn, will support business investment and the construction sector, following the peak in housing construction activity,” says Rumens and Gutterman.

Australia is also supported by idiosyncratic demographic trends. Unlike most countries where the population is steadily ageing high working age immigration has kept the share of the population who are working age in Australia relatively high.

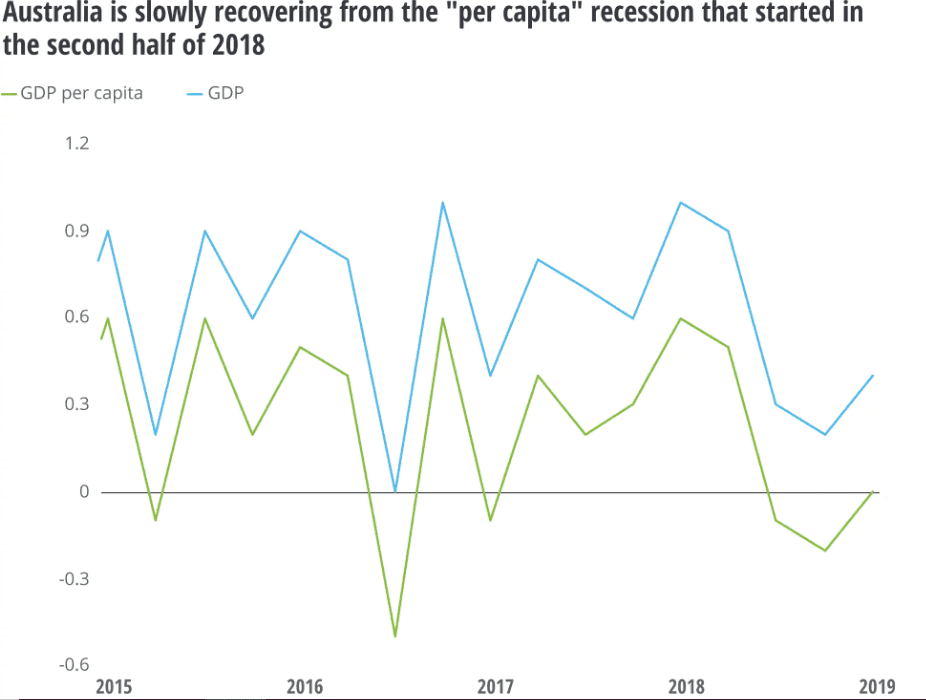

Growth on an aggregate basis has been relatively strong and Australia has not had a technical recession for 28 years. The recent slowdown was, however, reflected in a fall in per capita growth, yet even here there appears to be signs of a basing and turning around in the trend (as shown in the graph below).

Deloitte's analysis is not the only evidence supporting an improved outlook for Australia.

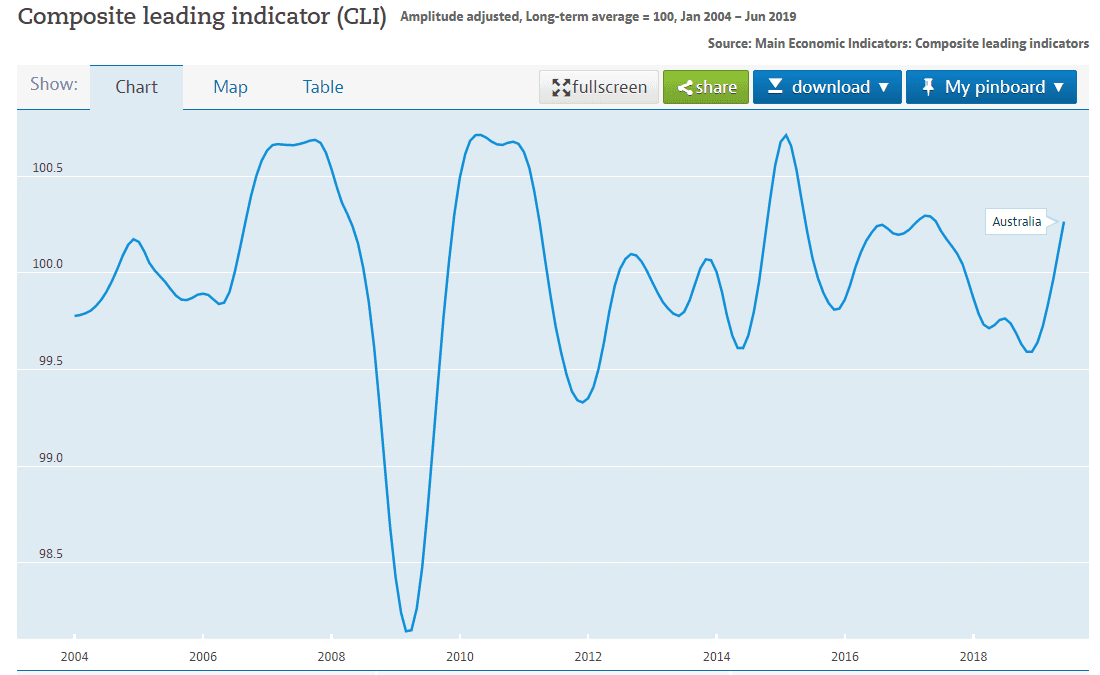

The OECD’s composite leading indicator (CLI) a respected signal of turning points in the business cycle and it is showing a new upcycle could be about to start.

The indicator turned at the start of 2019 and has since risen above the 100 ‘equilibrium’ level which distinguishes periods of expansion from contraction. Given the 6-9 month lag between the CIL and the economy, we may be reaching the point right now at which economic data starts to catch up.

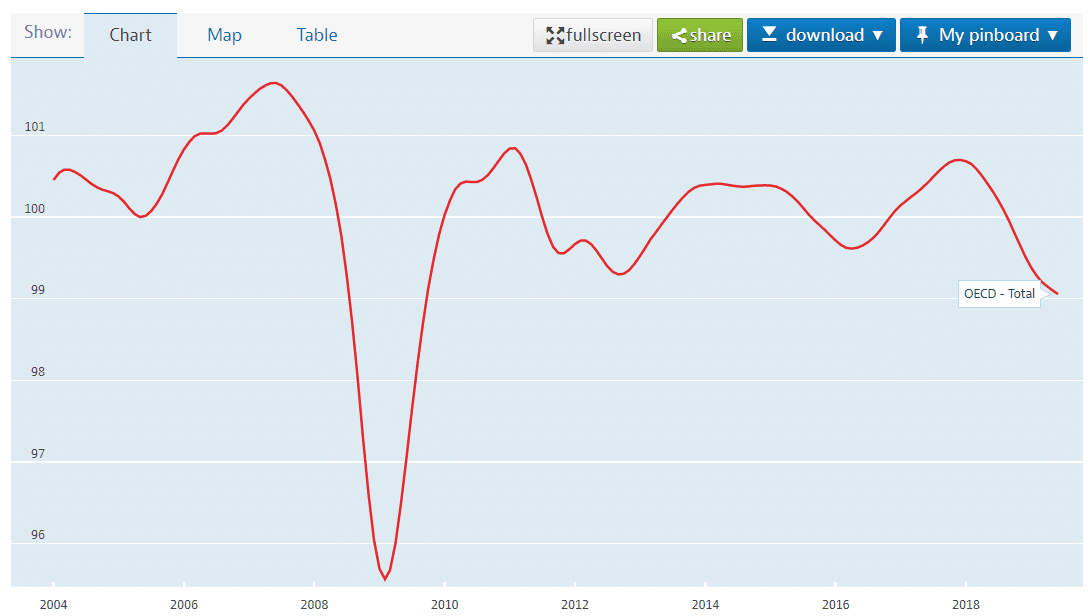

The Australian CIL also stands in contrast to the composite OECD indicator which is falling due to the effects of the global slowdown. This could indicate Australian exceptionalism and a ‘counter-world-cycle’ upswing.

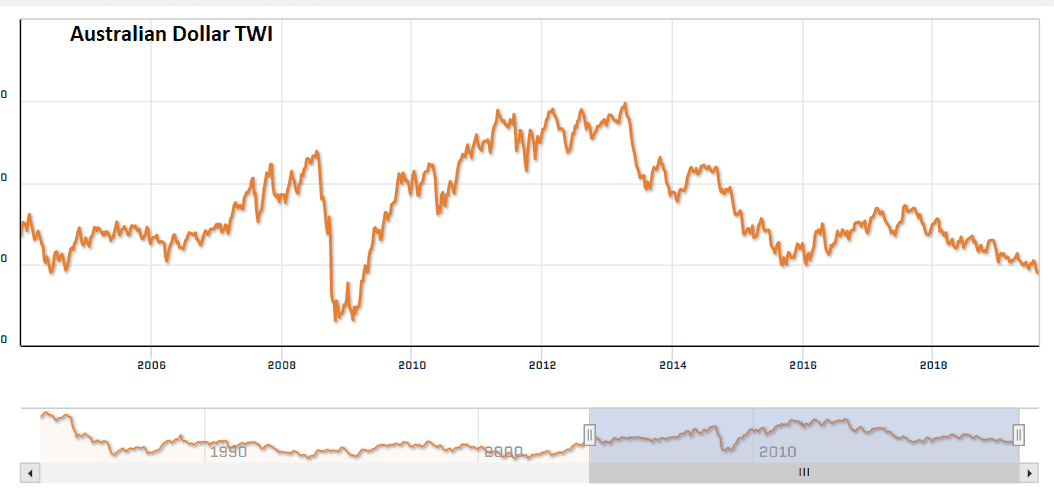

The rising Australian CIL has also been diverging with the weakening Australian Dollar Trade Weighted Index (TWI) since the start of 2019 - normally the two rise and fall in relative harmony. According to analysts it could reflect an undervalued Australian Dollar which may start to rise from here on in.

The evidence of potential growth paints a positive picture for Q’s 3 and 4 and the start of 2020, but will the expected upturn be enough to prevent the RBA from cutting interest rates again, something which would be negative for the Australian Dollar?

The answer is that it is unlikely to be enough.

The RBA is looking for a ‘new’ revised full employment rate of 4.5% before it expects inflation to start rising back up to target.

This week’s data showed unemployment stuck at 5.2% due to an increasing participation rate. It suggests the RBA is right about there still be more spare capacity in the economy and unless the rate can fall 70 basis points the RBA will probably continue with its easing cycle, especially given the overarching global headwinds from the increasing slowdown in manufacturing and trade.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement