Image © Pound Sterling Live

- GBP/ZAR poised to break lower although 50-week MA supporting

- Political factors a major concern for both currencies

- Main release for Sterling is UK Q2 GDP data; for the Rand political factors significant

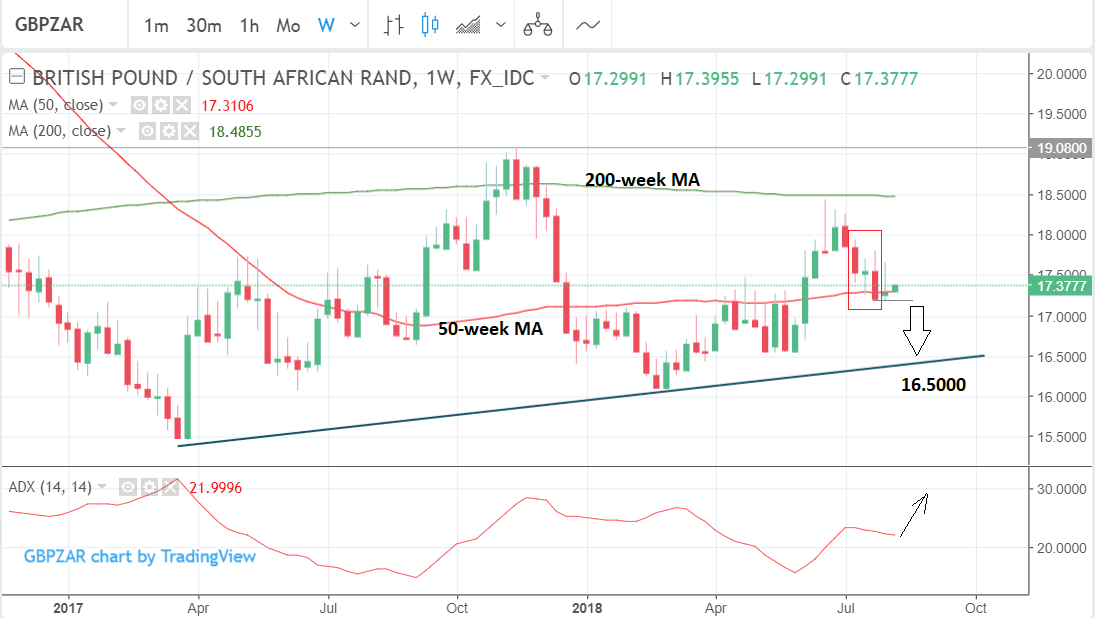

The Pound-to-Rand exchange rate is trading at 17.35 on the interbank market which is marginally higher than the 17.28 close of the previous week.

Political crosscurrents both from the UK and South Africa appear to be keeping the pair in a tight range but our technical studies suggest there is some evidence of a marginal bias to the downside on the weekly chart.

GBP/ZAR has formed a bearish continuation pattern - outlined in a red box above - but at the same time downside has been inhibited by the 50-week moving average (MA) at 17.31. Large MAs often act as obstacles to the trend leading prices to stall, bounce or reverse.

For confirmation of a bearish continuation we would want to see a clear break below the 50-week MA and the 17.1740 lows. Such a move would probably take the exchange rate down to the next target at the trendline at 16.5000.

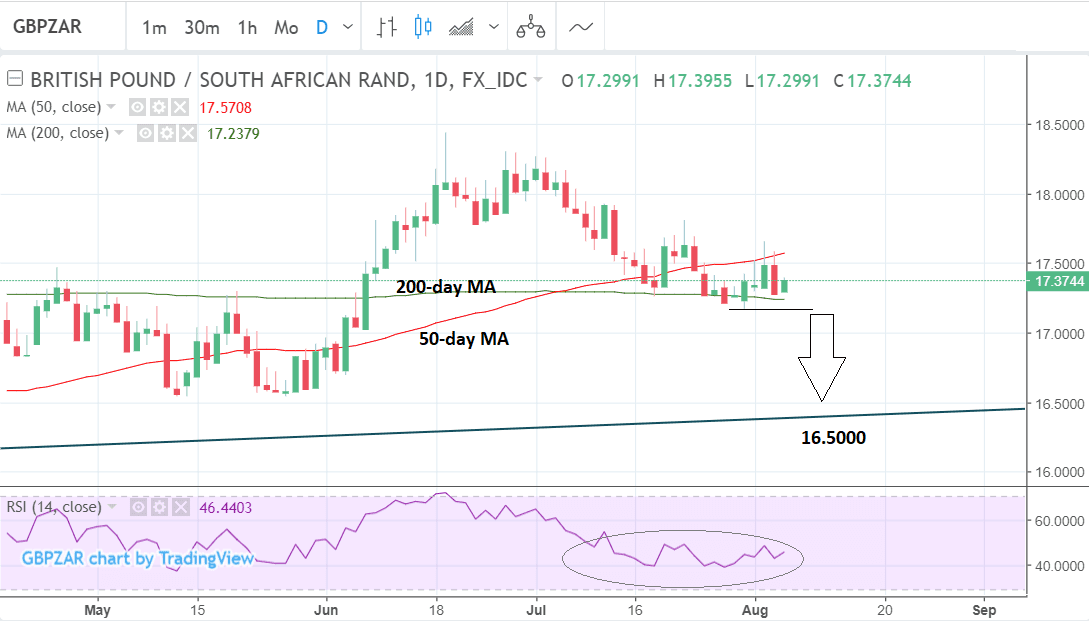

The daily chart shows the pair going sideways along the 200-day MA in a similar way to itsrange along the 50-week MA on the weekly chart.

There is a chance both that the exchange rate could break below the MA on the way lower to its target at 16.5000 or that it could reverse and rise.

The RSI momentum indicator in the lower pane looks as if it is basing and could be about to rise, which would also suggest upside in the underlying asset.

The RSI may even have formed a type of bottoming pattern itself, called a double bottom, which heralds growth not decline; and a move above 46.5 on the RSI could be quite bullish for both for momentum and GBP/ZAR.

This seems to suggest bullish and bearish forces are more evenly balanced on the daily chart - a fact which should caution sellers and backs up our initial observation on this pair that sideways action might be in store.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

What to Watch for the South African Rand this Week

The Rand had been recovering quite strongly on increased inflows to its domestic bond market but this was overshadowed recently by domestic political concerns.

Chief amongst these is the government's decision to push through a change in the country's constitution to allow for the expropriation of land without compensation.

The announcement of the policy immediately sent the Rand as it will increase SA's riskiness as an investment destination.

Previously inflows to SA bonds had rise because of their unique risk-reward profile, which offered investors a relatively high yield in return for the risk of holding SA debt.

In the week ahead investors will be watching the news wires closely for more domestic political news but on the hard data front it will be quiet week for the Rand as there are no tier one or two releases to report.

A key factor which could impact on the Rand in the week ahead is increasing global trade tensions and the negative impact these could have on global growth.

If a trade war between the US and China causes a slowdown in China emerging market currencies such as ZAR might continue to struggle.

"Tariff actions will mostly likely impact adversely on global growth by affecting integrated supply chains and hitting net-exporting EMs, including SA," says Zaakirah Ismail an analyst at Standard Bank.

America's most recent threat is to increase tariffs on $200bn worth of Chinese goods from 10% to 25%.

Yet whilst the latest threat is expected to cost China circa 100bn in lost revenue markets may now have fully absorbed the shock according to analysts at Citibank.

"The war of words escalates between US – China on trade but there is little follow through in terms of actual substance," says Citibank, adding, "China already offered in June to buy an additional USD70bn in US farm, manufacturing and energy products.

This compares to a loss of ~$101.7bn in Chinese exports to the US if the latter goes ahead with the higher 25% tariffs on USD200bn of Chinese goods (Citi analyst estimates)."

"The approximately USD31bn difference suggests the two sides may not be as far apart as is currently imagined. And recall that markets already appear to be well on their way towards partly discounting additional US tariffs on Chinese goods via the 10% depreciation in CNY seen since April," concludes Citibank.

In the week ahead, therefore, investors will be watching the news wires closely for more domestic political news as well as the latest developments impacting on global trade, but on the hard data front it will be quiet week as there are no tier one or two releases to report in SA.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here