© Natanael Ginting, Adobe Stock

Despite an unexpected jump in South African economic growth analysts at Swiss bank Julius Baer don't expect the Rand to strengthen much further.

The South African Rand has been rising strongly ever since it plumbed multi-month lows back in November 2017, but this uptrend is now forecast to fade and the Rand could even begin to weaken once more.

These are the expectations of analyst Annabelle Rey with Switzerland's Julius Baer who is the latest to add her voice to the view that the benefits to the currency presented by the Cyril Ramaphosa takeover are limited.

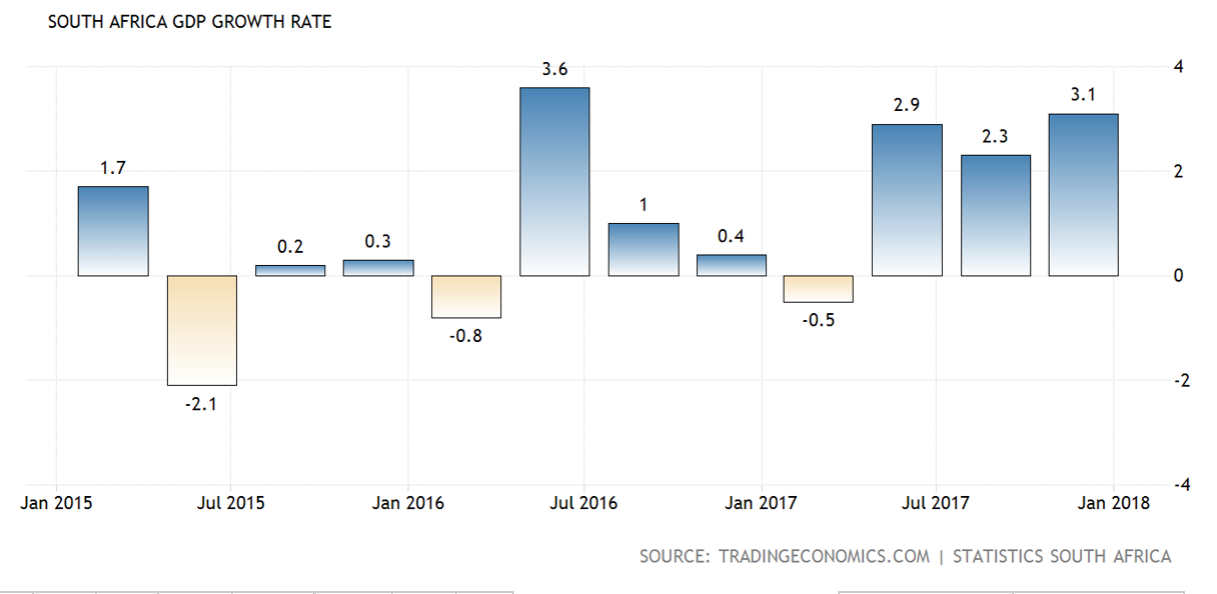

Rey's research findings come despite some ostensibly positive developments for the currency, including most recently the surprise jump in GDP in the final quarter of 2017, which rose 3.1% on the previous quarter, beating expectations of only a 1.8% rise, hands down.

Yet the surge in GDP was not enough to shift Rey's bearish opinion as she believes most of the growth came from a rise in "temporary" components such as agriculture and trade rather than the 'engine rooms' of growth: manufacturing and mining.

The previous quarter's GDP growth rate was also revised up to 2.3% although these figures may sound high the quarterly growth data series is historically subject to considerable volatility.

Others are also not convinced that economic growth rates will be sustained at the recently announced level.

"We are sceptical as this high momentum is sustainable. The change in government and the hope of a change in politics are likely to lead to positive momentum for investments. But the planned tax rises, rising imports, and the continued drought are likely to slow the growth momentum. We remain cautious regarding the rand," says Commerzbank Elisabeth Andreae.

(Image courtesy of tradingeconomics.com)

Longer-term growth based on comparisons to the year before (year-on-year) is trending up - which is positive, but, nevertheless, it has still far from the glorious heights of pre-2015s.

(Image courtesy of tradingeconomics.com)

Ramaphosa's Reign

As mentioned the positive driver of the Rand over recent weeks has been the end of the Zuma presidency and his replacement with the more reform-orientated Cyril Ramaphosa, yet Julius Baer's Annabelle Rey highlights doubts about how quickly the new President can implement new reforms.

Ironically, his administration's main reform so far has been Rand-negative, in the form of the expropriation of land without compensation - which constitutes a huge, off-putting, red-flag, to foreign investors.

The composition of the new cabinet which includes many of the 'old-guard' from the Zuma regime further suggests that there is a risk that the reform-bias previously attributed to Ramaphosa maybe heavily compromised or conditional.

The expropriation of land, for example, has been seen as a sop to radicals and together with the orthodox cabinet reshuffle suggests a blunting of political risk as a primary bullish driver for the Rand going forward.

Moody's Review

A major event on the horizon for the Rand is the credit rating review by the largest credit rating agency Moody's in March (later this month).

Moody's is the last of the big three agencies to continue to categorize SA as a reliable borrower or SA debt as 'investment grade'.

The other two agencies Fitch and Standard and Poors have downgraded SA debt to below investment grade, or 'junk status' as it is known in market-speak. A similar downgrade by Moody's would lead to the fire sale of SA bonds, much higher borrowing costs and a cliff-edge fall in investment, given the number of people willing (or able) to lend the country money would fall drastically overnight.

Of course, all this would also have an extremely negative knock-on effect on the Rand too.

SA came close to suffering a downgrade in November 2017 but Moody's stayed its hand and kept the country on review pending a re-appraisal in March. We have now reached that re-appraisal.

Funnily enough most analysts, although bearish the Rand, are nevertheless positive about the outcome of the credit rating review.

"Moody’s, whose review is due later this month, is now less likely to downgrade South Africa to junk," says Rey.

Commerzbank's Elisabeth Andreae agrees saying "the published (GDP) data surprised with a rise of 3.1%. This is good news in view of Moody’s rating review at the end of the month - as higher growth facilitates the urgently required consolidation of the public finances."

The chances of a downgrade are also lower after the recent budget which balanced spending with higher taxes and this was also thought to be seen as a positive by Moodys and less likely to make them press the button on a downgrade.

Cleary the Rand's next move is heavily dependent on the outcome of the rating review, but as things stand the chances of a downgrade have diminished; nevertheless this expectation is already incorporated in the price of ZAR and the boost might have already been felt.

Negative Correlation With USD

It is also interesting to note how closely the recent rise in the Rand correlates with a sell-off in the US Dollar but it will come as no surprise to long-standing observers of the South African currency.

The Rand has a high tendency to go in the opposite direction to the US Dollar and the relationship is not based on chance as South African companies have a higher-than-average of debt denominated in US Dollars, as well as loans from US financial institutions.

This means when the Dollar rises in value so do their debts and repayments which become more expensive to service, and this explains the inverse relationship between the two currencies.

Given the outlook for the US Dollar does not appear very rosy in 2018 the Rand could actually gain a lift from this particular driver, suggesting the currency is not at imminent risk of a sizeable sell-off and the downside could be well protected.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.