Image © Government of South Africa, reproduced under CC licensing

- ZAR advances on USD and GBP after ANC appears to back reforms.

- But ANC panned in local press on claims support doesn't go far enough.

- ZAR also aided Wednesday by bets on more Federal Reserve rate cuts.

- Commerzbank eyes signals of further upmove in USD/ZAR on the charts.

- Rabobank sceptical of outlook for emerging market currencies inc ZAR.

- Bank of America sells ZAR ahead of October budget, Moody's review.

The Rand advanced against major rivals Wednesday after the governing African National Congress (ANC) appeared to offer support for a long-awaited reform program including specific proposals put forward by finance minister Tito Mboweni, but markets may have misread South Africa's ruling party.

ANC party grandees and officials agreed Wednesday that South Africa's economy is in need of reform, although not for the first time, and stated its support for a broad array of programs but the rub for observers is that few of the measures it endorsed were in any way new. The statement was lightweight on details and Mboweni's proposals from August appeared to have gotten only a brief look-in among members of the national executive committee.

STATEMENT ON THE OUTCOMES OF ANC NATIONAL EXECUTIVE COMMITTEE HELD ON 27-30 SEPTEMBER 2019#ANCNEC pic.twitter.com/illVHAyiRp

— African National Congress (@MYANC) October 2, 2019

Business Day, South Africa's venerable equivalent to the FT, panned the ANC's statement and led with the following on Wednesday morning; "The ANC released a lengthy statement on its plan for economic recovery on Wednesday, repeating the long list of priorities mostly from the National Development Plan of 2011, which it has restated year after year without implementing."

The daily print and web paper has suggested most of the commitments made by the ANC are reiterations of old ideas that are yet to right the capsizing ship that is the South African economy and apparatus of governance. It also noted that many of "controversial", but nonetheless key, parts of Mboweni's plan were not even mentioned by the ANC. That could be bad news for the Rand come the end of November, when Moody's announces its latest rating decision.

"Successful restructuring of the ailing electricity giant is important to revive growth, investment and employment in South Africa. No wonder investors are getting cold feet in the run-up to Moody's rating decision on the country’s sovereign credit rating. The loss of the last investment grade rating is likely to result in substantial ZAR depreciation," says Elisabeth Andreae, an analyst at Commerzbank. "We advise ZAR investors to remain cautious."

Above: USD/ZAR rate at 15-minute intervals alongside Pound-to-Rand rate (blue line, left axis).

The Rand rallied against major rivals on perceptions that African National Congress support for reforms might make a loss of South Africa's last remaining investment grade credit rating less likely. Mboweni published a 'paper' of prescriptions for economic reforms in August, including on how to fix the ailing electricity provider Eskom, but little was said by the ANC on that score.

Optimism about the credit rating might soon unwind but the Rand and emerging markets were strong generally on Wednesday as investors appeared to be betting the U.S. economy is headed for a rough patch. Global stock markets were lower and so were commodities like oil, while gold and government bonds were higher. But in the currency world, the Dollar was higher against the safe-haven Franc, lower against the safe-haven-but-equity-sensitive Yen and down against all 'risk' assets including the Rand and other emerging world currencies.

Trouble in America shouldn't be good news for South Africa or the Rand but it might turn out to be so if it ultimately leads the Federal Reserve (Fed) remove the fingers from its ears and open fire on the U.S. economy with a barrage of rate cuts. As a side effect, that would lift growth the world over including in an economically-challenged South Africa, but so far the Fed has shown itself to be deaf to the overtures of the market and demands of the White House. It would also make the typically-higher yields on South African government bonds seem more attractive on the offshore side, potentially stoking demand for the Rand.

"USD/ZAR’s sell-off from the August high at 15.4997 ended at its current September low at 14.5027 [and is] heading back up again towards major resistance at the 15.4574/15.4997 August highs. This we expect to cap," says Karen Jones, head of technical analysis at Commerzbank. "Only if a rise and daily chart close above the 15.4997 high were to be seen, would the September 2018 peak at 15.6945 be back in sight. Minor support is seen between the 55 day moving average and the three month support line at 14.8114/14.6999."

Above: USD/ZAR rate at daily intervals alongside Pound-to-Rand rate (blue line, left axis).

The Institute of Supply Management (ISM) Manufacturing PMI surpsised the market previously on Tuesday when it fell to decade low for the month of September, with most components of the survey helping to paint a picture of a U.S. economy that is now being bitten by President Donald Trump's trade war with China. Until now, the Fed has been reluctant to indulge markets and the White House with the level of interest rate cuts that many say is necessary for the U.S. economic expansion to be kept alive.

But indulging the market could be good for the Rand because high U.S. rates have raised the cost of financing for emerging economies that borrow in the market because the U.S. benchmark is effectively the global 'risk free' rate that plays an important role in dictating the returns demanded by investors in all financial assets, but especially bond market investors who loan money to governments. High or rising rates in America also boost demand for the Dollar, which is itself problematic for the emerging world.

As I predicted, Jay Powell and the Federal Reserve have allowed the Dollar to get so strong, especially relative to ALL other currencies, that our manufacturers are being negatively affected. Fed Rate too high. They are their own worst enemies, they don’t have a clue. Pathetic!

— Donald J. Trump (@realDonaldTrump) October 1, 2019

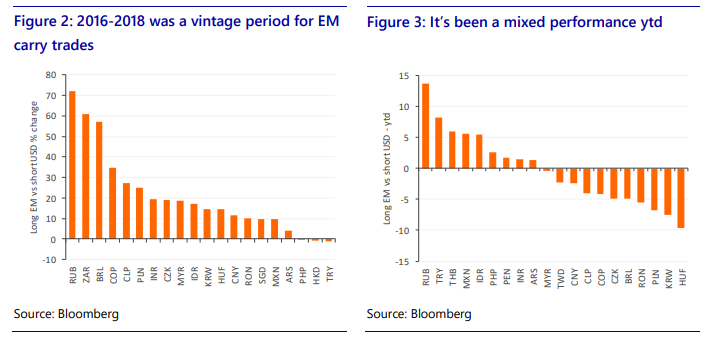

"Some of the biggest moves in USD/ZAR over the past few years can be attributed to massive spikes in JPY/ZAR caused by Japanese retail players capitulating when global sentiment deteriorates markedly. Essentially, a carry trade can be a sharp tool," says Piotr Matys, a strategist at Rabobank. "With President Trump saying that reaching a deal with China is not a priority ahead of the 2020 presidential election, we remain sceptical about a major breakthrough."

September's ISM Manufacturing PMI surprised sharply on the downside Tuesday, dropping from 49.1 to 47.8 when markets had looked for it to rise to 50.4 last month. Weakness was broadbased too and the index, which is computed from surveys of of 400 purchasing managers in the U.S. manufacturing sector, is now at its lowest level for ten years.

The only three categories to increase in the September ISM survey were the new orders index, the prices index and the index of GDP-reducing imports. U.S. production output fell more than 2% last month, the employment index dropped more than 1% while both the deliveries and inventories indices also fell. And the index of new GDP-boosting exports dropped by 2.3%, the institute says.

"The ISM manufacturing index has dropped to a 10-year low as trade worries, weak global growth and a strong dollar weigh on the sector. Given the threat of contagion to other parts of the economy further Fed rate cuts are coming," says James Knightley, chief international economist at ING. "It was below every single forecast in the market... These figures suggest that further output declines are likely and point to downside risks for Friday’s US jobs report."

Above: Rabobank graph detailing recent as well as 2019 performance of 'carry' currencies like ZAR.

Chinese growth is slowing, Europe's economy is widely believed to be stagnating and Germany's economy already looks to be in recession due mainly to the damaging impact that President Donald Trump's trade war has had on international trade and manufacturing sectors the world over.

This has already seen the European Central Bank (ECB) rush to support growth with an interest rate cut further below zero and a fresh round of quantitative easing, but the Fed has cut rates just twice even after lifting them nine times in the three years to the end of 2018.

Bloomberg News reported Friday that Trump is considering limiting some American investment flows to China, which would be an aggressive step that marks yet another escalation in the trade spat. The two sides are set to hold talks in Washington on October 10 and 11 but if an agreement isn't reached, the White House could lift the tariff rate imposed on around $250 bn of China's annual exports to the U.S. from 25% to 30%. Further tariffs are also scheduled to go into effect on December 15.

"We think EM would need a major positive surprise to rally in October," says David Hauner, a strategist at Bank of America, in a note to clients last week. "Rand is the EEMEA bellwether but it also faces the medium-term budget statement and subsequent Moody's review. We think that the downgrade is priced in for the bonds, but experience suggests still FX weakness. We think the balance of risk is asymmetric...Investors may consider buying USD/ZAR ahead of the October risk-events as protection, even if the events themselves later on may lead to renewed USD/ZAR selling. We buy USD/ZAR at 14.86."

Above: Dollar Index shown at daily intervals and annotated for recent events. Click for larger image.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement