Above: BOJ Governor Haruhiko Kuroda stayed emphatically pro-stimulus at his latest press conference. Image © European Central Bank, reproduced under CC licensing.

- Bank of Japan makes no further moves towards unwinding stimulus

- Notes headwinds from global macro forces

- Yen failing to attract safe-haven flows as markets shrug at trade war

The Japanese Yen fell midweek after Japan's central bank disappointed investor expectations by not taking a more decisive move to dismantle the country's massive stimulus programme.

The Bank of Japan's (BOJ's) 'quantitative and qualitative' easing programme (QQE) is a constant headwind for the Yen because it keeps interest rates unnaturally low, incentivising capital outflows, and money supply high.

The BOJ produces a policy statement after each meeting and the September statement showed no new measures to cut stimulus or any hints the BOJ was planning such a move.

Whilst some analysts had expected as much others had foreseen a possibility of further tightening following the measures taken at the July 31 meeting.

Recent comments from Japan's President Shinzo Abe that monetary stimulus should not "continue forever" were taken as a hint to the BOJ to start turning the 'taps off' - however, in all fairness, few analysts thought the BOJ would respond immediately.

The governor of the BOJ, Haruhiko Kuroda, stayed emphatically pro-stimulus at the press conference after the meeting, saying, "we must maintain our powerful monetary easing given it will take time to achieve our inflation target.”

The remark could be taken as mild rebuke of Abe's interference.

When asked more specifically to respond to the President's suggestion Kuroda simply reiterated the orthodox line that, "We won’t be continuing our current unconventional policy if 2 percent inflation is met.”

The BOJ implemented policy changes at its July 31 meeting which allowed for more flexibility in controlling the longer end of the yield curve, allowing 10-year rates to rise, and also reduced the size of deposits subject to their -0.1% negative interest rate from 10tn to 5tn Yen. These were taken as de facto tightening measures and possible firsts steps to removing stimulus altogether.

Yet there were no new measures mentioned in the statement on September 19, and more space was given to discussing geopolitical risks from trade conflicts and their negative effects on global supply chains.

"Risks to the outlook include the following: the U.S. macroeconomic policies and their impact on global financial markets; the consequences of protectionist moves and their effects; developments in emerging and commodity-exporting economies including the effects of the two aforementioned factors; negotiations on the United Kingdom's exit from the European Union (EU) and their effects; and geopolitical risks," says the BOJ.

One other reason the BOJ may have decided to sit on its hands is the timing of Japan's presidential election on September 20 (the day after the BOJ meeting).

Although president Abe is expected to win re-election with 70-80% of the diet behind him, some analysts said the BOJ was unlikely to make any major policy changes ahead of such an important political event.

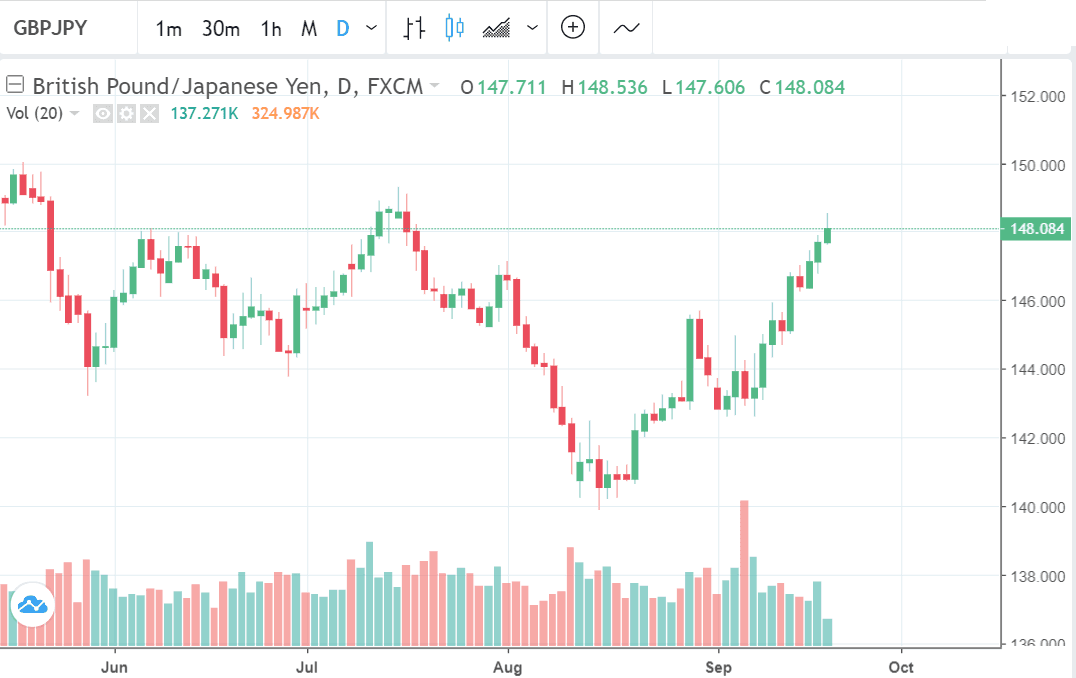

USD/JPY extended its rally to a 7-week high of 112.45 on Wednesday whilst GBP/JPY rose to 148.54, surpassing our 147.90 target in the process.

Find out why we set this target here.

Whilst BOJ inertia was one fundamental reason given for the currency's weakness, another possible driver may have been a rise in US 10-year Treasury yields, which suggested a longer-term growth and reflationary outlook for the US, supporting the Dollar.

And, while global trade tensions remain elevated they are clearly no longer providing the support to the safe-haven Yen that we have come to expect.

"The latest leg of Yen weakness is surprising as it has coincided with a further escalation of trade tensions between the US and China. The yen was expected to strengthen on the back building trade tensions but that has clearly not been the case recently," says Lee Hardman, a Currency Analyst with MUFG in London.

The latest salvos in the global trade war was fired Tuesday when the US imposed a 10% tariff on a variety of Chinese imports. China said it would not sit back and would respond.

U.S. President Trump was quick to respond to the retaliation by tweeting that “there will be great and fast economic retaliation against China if our farmers, ranchers and our industrial workers are targeted”.

"Despite the risk of a further escalation in trade tensions, it was notable that risk assets staged an initial relief rally yesterday perhaps reflecting some relief that financial markets proved resilient to the latest announcements which were well anticipated," says Hardman.

Hardman says it is clear to him that the recent improvement in risk sentiment is beginning to weigh more heavily on the yen especially as yields outside of Japan are also adjusting higher at the same time.

Advertisement

Lock in Sterling's September recovery: Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here