Image © Adobe Stock

The dollar shines and the Japanese yen slides as U.S. bond yields power higher writes Marios Hadjikyriacos, Senior Investment Analyst at XM.com.

The U.S. dollar resumed its march higher on Tuesday, receiving fuel from interest rate differentials and safe haven flows.

Bond market players have started to push US yields higher once again, enhancing the dollar’s interest rate advantage, while some disappointing business surveys from China pushed investors into the safety of the world’s reserve currency.

As per usual, the main casualty when U.S. yields climb higher is the low-yielding Japanese yen.

The yen has been clobbered both by rising foreign yields and the sharp spike in oil prices, as Japan imports nearly all its energy from abroad, hitting the yen from the trade channel each time global energy prices rise.

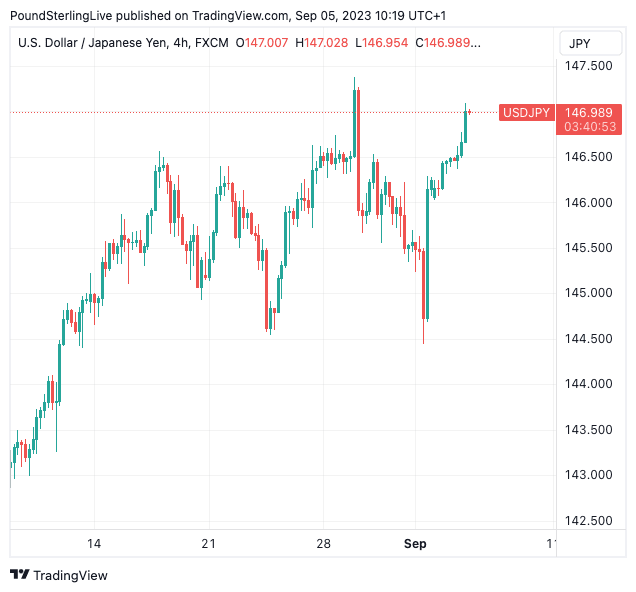

Above: Dollar-Yen at four-hour intervals.

Even though dollar-yen is trading near levels that Tokyo decided to defend last year, the risk of another round of FX intervention seems fairly low as the speed of the yen’s depreciation has been much slower this time and government officials have not been as vocal.

Japanese authorities will likely ramp up their verbal warnings to fend off speculators if dollar-yen continues to ascend towards 150.00, but are unlikely to actually pull the intervention trigger, a view corroborated by the muted implied volatility in FX options.

That’s generally a tell that institutional players are not panic hedging against any massive moves in the yen.

Over in China, the spell of optimism that prevailed in recent days proved short-lived. The reality check came in the form of a disappointing services PMI survey, which fell sharply in August, foreshadowing a persistent slowdown in economic activity.

China-linked assets fell through the trapdoors in the aftermath. The Australian and New Zealand dollars crumbled, with the latter hitting new lows for the year as these economies rely on Chinese demand to absorb their commodity exports. Similarly, Asian shares retreated alongside energy prices, although these moves were not so severe.

One encouraging development was that Chinese developer Country Garden avoided default today after it paid interest on two dollar bonds, helping to avert a deeper crisis in the nation’s embattled property market, at least for now. Yet, this was overshadowed by the poor PMI readings.

In the land down under, the Reserve Bank of Australia kept its policy settings unchanged earlier today, signalling a neutral stance and emphasising data dependence. Naturally, the reaction in the aussie dollar was limited, leaving the currency in the hands of China fears and risk aversion instead.

Wall Street is set to reopen today after a long weekend and futures are trading in the red.

Rising bond yields coupled with concerns around global growth are a rare and toxic cocktail for equities, particularly when valuations are stretched and earnings growth is stagnant. Markets have rallied hard this year, but the risk-to-reward profile from current levels seems highly unattractive.

Finally, it turns out gold prices could not resist gravity for long. The precious metal has resumed its downward trajectory, succumbing to the weight of rising yields and a rampaging US dollar.

Looking at the charts, bullion is at a crucial technical crossroads as a break below the congested $1,935 zone could see scope for extensions towards the $1,900 region.

It is worth noting, though, that gold has displayed striking resilience this year. It is trading less than 7% away from record highs even in an environment where the dollar is strengthening and yields are near their highest levels of this cycle. That’s a sign of relative strength, even if the near-term outlook seems gloomy.