Image © Adobe Stock

- Risk trends to drive Yen higher

- JPY is also undervalued

- High public debt a risk factor

The Yen is probably going to get stronger as global uncertainty persists, says QCAM Currency Asset Management AG.

The currency has been trading quite strongly of late on the back of increasing global growth fears mainly put down to trade tensions. Given there is no end in sight to these tensions, or rather there seems to be no turning back to the way things used to be, the Yen is likely to continue on strengthening.

The reason for this is the carry trade, which involves traders borrowing in a low-interest rate currency such as the Yen and using the funds to buy either a currency in a higher interest rate jurisdiction or a higher-yielding riskier asset.

The difference between what carry traders earn from the higher-yielding asset and what they have to pay for borrowing the Yen is the carry trade profit margin.

The carry trade works fine when the overall economic outlook is positive but when it deteriorates investors get cold feet, pull out of their risky assets, and repatriate their money to Japan.

This is why the Yen gets stronger when risk appetite wanes and fear starts to grip traders - it’s all the carry coming home.

The recent dramatic turnaround in U.S. interest rate expectations has been a major driver of carry backflows which have been pushing the Yen higher, however, the effect is likely to be only temporary as interest rates are still substantially higher in the U.S. than in Japan.

“The recent shift in the Fed’s interest rate projections changed the carry arithmetic, but only temporarily, since US interest rates remain significantly above those of Japan,” says Eschweiler.

Perhaps as important for the Yen is the global outlook, which includes the outlook for world trade, the sustainability of international tech supply chains, and the path of globalisation, which currently seems uncertain.

“Certainty is a factor still more important than the interest rate differential,” says Eschweiler. “Investors are less likely to short the yen and go long on higher-yielding currencies if economic and market conditions are uncertain. The resumption of trade talks between the US and China and the monetary policy support pledged by the Fed and other major central banks provide some relief. Still, damage has already been done to the global economy and uncertainty is likely to prevail until economic surveys and activity data signal a clear turn for the better. As long as this is not the case, we think the yen is likely to do well.”

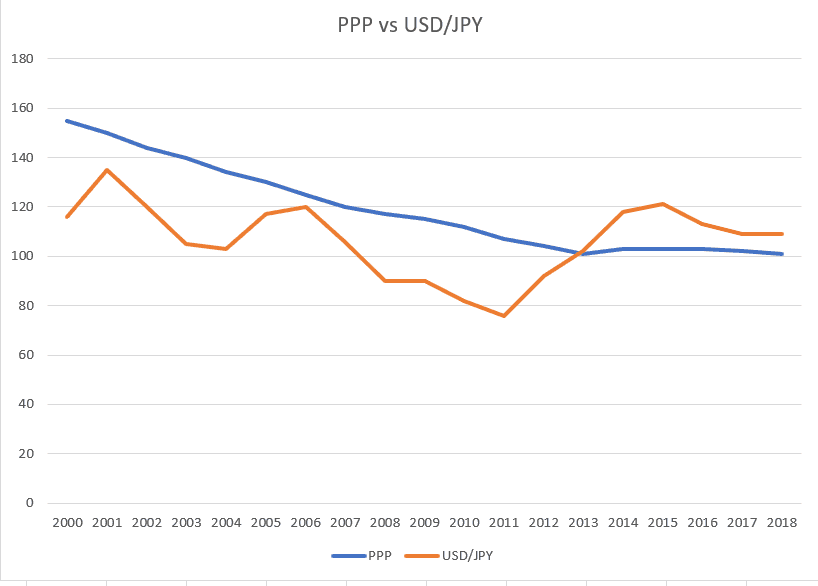

A secondary factor in QCAM’s long Yen call is that the Yen is undervalued according to Purchasing Power Parity (PPP) valuations.

PPP is a method of establishing the ‘fair value’ of a currency so as to have a benchmark against which the actual exchange rate can be compared so as to get a feel for when it is getting outrageously over or undervalued.

PPP uses the direct comparison of the cost of a basket of the same goods in two countries to establish a valuation.

If a basket of goods in Japan, for example, cost 1000 Yen, and the same basket cost 10 U.S. Dollars in America then the PPP would be 100 Yen to the Dollar, or 1000 Yen divided by 10 Dollars.

Assuming this was the case, the current USD/JPY exchange rate of 108 would be deemed high and reflective of an undervalued Yen (or overvalued Dollar).

The inference is that the exchange rate would fall down to meet its fair value in the future, suggesting a bearish outlook for the pair.

Yet, as Eschweiler says, in reality, currencies can remain PPP under or overvalued for long stretches of time and the method is problematic as a method for forecasting.

The chart below, for example, uses PPP data calculated by the OECD and compares it to the exchange rate. Note how it has been higher since 2013.

Another reason to expect a stronger Yen is the country’s high current account surplus. This is because Japan has such strong exports and the biggest share of the current account is made up of the trade balance.

A high surplus would normally project a stronger Yen but in the case of Japan the surplus is almost balanced out by high Foreign Direct Investment (FDI) outflows, says Eschweiler.

Indeed this in part is caused by the carry trade as well as Japanese investors searching for yield outside of Japan.

There is also a major reason to be cautious about further Yen upside too, according to QCAM.

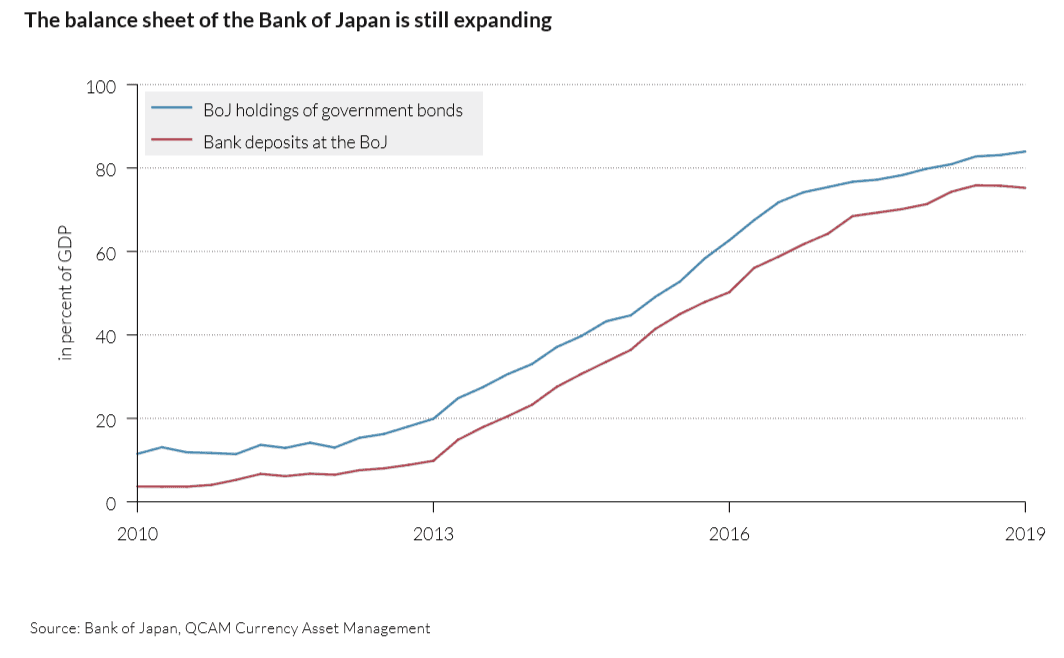

That is Japan’s high level of public debt, which is the highest in the world as a percentage of GDP - currently at 240%. The level of debt poses as financial stability risk.

85% of GDP of the government’s debt is owned by the Bank of Japan (BOJ) and this is increasing by about 10% a year due to the government running a circa 3.0% annual budget deficit.

The money the BOJ lends to the government comes from deposits it holds from domestic banks, which leaves it vulnerable. This poses a potential negative for the Yen.

“The BoJ funds the expansion of its balance sheet with deposits from domestic banks. Moral suasion can probably prevent a run on the BoJ, but the banking system will become increasingly nervous about its exposure to public debt as BoJ holdings of government bonds rise further. It is not clear how and when this public debt funding scheme will end, but we think it is unlikely to be positive for the yen,” says the QCAM economist.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement