- A reliable indicator of impending recession is flashing red

- Markets betting the Federal Reserve is liable to committ a policy mistake

- Bodes for a softer Dollar according to analysts

© Xiong Mao, Adobe Stock

The flattening of the yield curve has been bothering investors for some time now; those regular followers of Pound Sterling Live will recall this issue is something we were looking at quite a bit back in November 2017 when the phenomenon first hit the radar.

The yield curve - the difference in expectations for future interest rates - matters because it can warn of impending recession; which has obvious and significant implications for US economic growth and the Dollar.

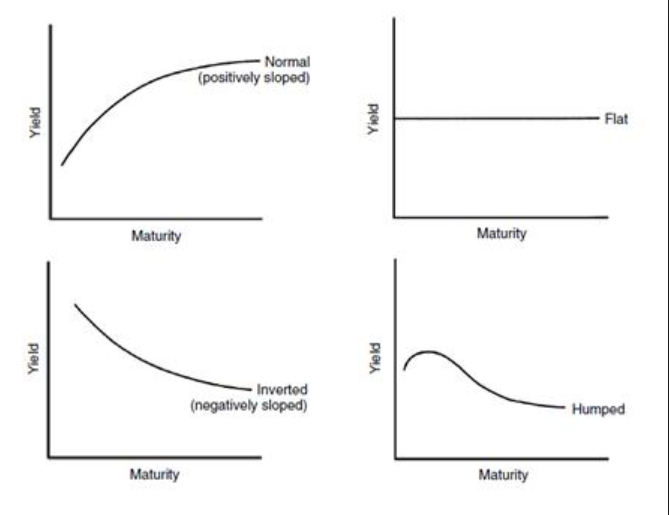

Normally the curve should rise and steepen as it moves from left to right and maturities get longer as shown in the chart below:

Sometimes the curve looks different, as it does right now, when it has flattened, sometimes it can even become inverted.

But what causes the curve to flatten?

"The yield curve has continued to flatten as the market sees Fed’s hiking cycle as gradually more mature," says Marit Øwre-Johnsen at DNB Bank ASA. "With six rate hikes since December 2015, Fed is heading closer to the so-called neutral rate. Fed’s estimate for the normal rate is close to 2.8%, while the Fed funds rate now stands at 1.75%. According to our projections Fed will reach the neutral rate in H1 2019."

Lower long-term rates suggest lower interest rates at the Federal Reserve in the future, therefore an inverted yield curve suggests interest rate cuts in the future, presumably in response to a struggling economy.

Whatever the case, the US treasury yield curve is flatter at the current time and there are concerns this flatness could lead to the inverted yield curve, which we noted earlier, is seen as a precursor to recession.

The shape of the curve is catching the attention of Federal Reserve policy makers, which in turn has caught the attention of foreign exchange markets who are trying to anticipate what the current scenario spells for the US Dollar going forward.

St. Louis Federal Reserve President James Bullard has over the course of the past 24 hours said that central bankers need to debate the yield curve right now, and that it could invert within six months.

"I am getting concerned about the flattening yield curve," Bullard told CNN's Richard Quest on Wednesday. "The inverted yield curve is a powerful predictor of economic downturns."

The phenomenon is likely be taken by investors as a recessionary signal for the US economy – irrespective of whether that is a true reflection of the underlying economic reality.

"The flatness of the US yield curve has now got to an ‘eyebrow raising’ stage – with St. Louis Fed President Jimmy Bullard claiming that the yield curve could become inverted within the next 6 months," says Viraj Patel, a foreign exchange strategist with ING Bank N.V.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Will a Flatter Curve = a Flatter Dollar?

Analysts are chewing on the latest developments and letting us know what this could potentially spell for the Dollar.

"The ongoing flattening of the US yield curve is one factor that could dampen support for the US dollar from higher yields. The market remains sceptical that the Fed will need to raise rates beyond 3.0%. The failure of the long end of the curve to move higher is a policy conundrum for the Fed. For the US dollar to derive more support for rising US yields, it will likely require the market to price in a materially higher terminal rate for the Fed’s tightening cycle," says Lee Hardman, a foreign exchange analyst with MUFG in London.

Bullard saying that the curve could invert within the next six months and reined back on rate hike momentum as a result, which is indeed a weighing factor on the Dollar.

However, Randy Quarles countered Bullard suggesting that while historically a curve inversion has preceded a recession, it doesn’t necessarily mean that will happen.

New York Fed President Dudley suggested he saw no reason to increase the pace of tightening at this stage.

"US yields are continuing to push higher led by 2-years causing the flattening, but the broader USD is still holding up well in the face of it," notes Robin Wilkin, an analyst with Lloyds Bank Commercial Banking.

ING's Patel says that were more investors adopt the view that the flattening yield curve is heralding a recession, it would likely trigger a broader flight-to-safety within global markets.

"Assuming that such dynamics were not already in play during the transition from a flat to inverted yield curve. Thus, the question we need to ask ourselves now is how likely is an inverted US yield curve over the next 6 months?" asks the analyst.

The sharp flattening of the curve – and clear lack of interaction between short-term and long-term US rates – leads ING's economists to posit that either one of two market dynamics are occurring:

(a) investors are pricing in growing risks of a Fed policy mistake – such that the narrative of a growing US economy within the backdrop of short-term policy rate adjustments is no longer credible; or

(b) the market is completely mispricing the strength of the US economy – as well as the current stage of the economic cycle that we’re in.

"Both the economic and financial evidence lends greater support to the former; as we’ve pointed out before, markets have begun to price in the peak for the Fed tightening cycle – with the 3-year short-term OIS forward rates lower than their 2-year equivalent," says Patel.

Moreover, the extremely low US unemployment rate – and general length of the current economic expansion – suggests to ING that the cycle is nearing its end (fiscal stimulus is merely a shot of adrenaline to extend the cycle by a year or two).

"While we have been arguing that the USD will take its cue from the US economic cycle – irrespective of what the Fed does – we do believe that the outlook for global asset prices in general now rests on what US monetary officials choose to do next. Tightening into a highly-leveraged late-cycle US economy could be a toxic combination for risky assets – one that should keep global risk appetite on the back-burner should the US curve remain as flat as it is," says Patel.

This all spells for the US Fed taking its foot off the accelerator when it comes to raising interest rates, and noting rising interest rates to be a long-term support of the US currency, this could therefore spell for a weaker Dollar.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.