The Dollar has weakened in November on newfound fears of a recession - hinted at by a flattening US treasury yield curve - but some analysts reckon this could in fact be a signal to buy the Dollar.

A flattening of the US yield curve is one of the big themes occupying trader chatter at present - as a flattening yield curve tends to signal an impending recession.

"The yield curve continued to flatten this past week, sparking interest from financial market participants and people looking for a diversion from thinking about the holidays," notes Diane Schumaker-Krieg, Global Head of Research, Economics & Strategy at Wells Fargo.

The yield curve matters because it can warn of impending recession; which has obvious and significant implications for US economic growth and the Dollar.

"The yield curve’s track record on predicting recessions has been very good, particularly when the curve inverts," notes Schumaker-Krieg. "An inverted yield curve is a red flag that a recession is less than one year away."

But, a couple of analysts reckon fears of an impending recession are misplaced and investors might be misinterpreting the economic weathercock that is the US bond market.

While the market is pointing 'recessionward' a misdiagnosis may present a buying opportunity for the Dollar as when markets realise the false-alarm, the currency will probably rise.

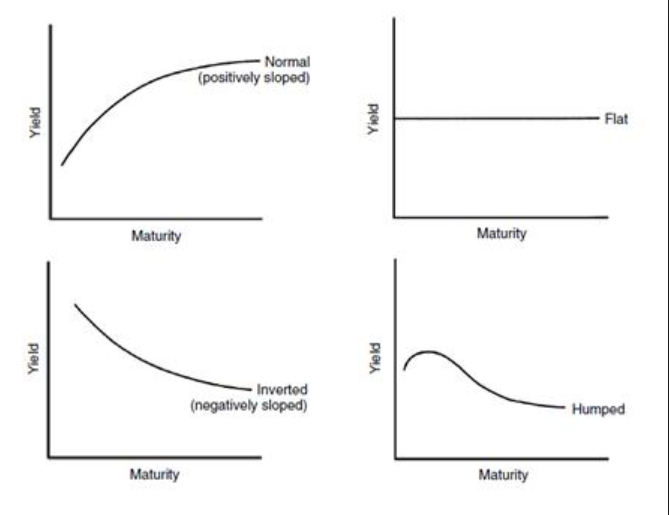

What is the Yield Curve?

The yield curve is a diagrammatic illustration of investors expectations about the future course of inflation and interest rates (charts provided below).

To understand it you have to understand bonds, which are a type of securitised loan which governments and large corporation's issue in order to borrow money.

A bond is sold to investors seeking a relatively safe bet by the organisation which seeks to borrow money.

The money raised has to be paid back, like in a standard loan, however, normally it is paid back in full at the end of the bond's 'term' which is stipulated beforehand and can be anything between 3-months and 30-years, rather than baked into repayments over a period of time like a standard bank loan.

In addition to the repayment of the principle at the end, the lender also gets an interest payment every 6-months or a year to compensate for inflation-erosion.

Bonds can be sold on, over and over, usually for close to the original loan amount but the price is adjusted for inflation.

If inflation expectations are high, for example, then the bond price falls, because the amount which will be repaid at the end of the term will be worth comparatively less than it would in less inflationary conditions; and vice versa for falling inflation expectations.

The 'yield' is simply a recalculation of the percentage interest paid at regular intervals to the bond-holder to compensate them for inflation-erosion.

For example, If the price of a 10-year bond falls from an original amount which is £100 to £90, due to higher inflation expectations, and that bond has an annual interest payment - or coupon as it is called - set at 5.0%, which is equal to £5.0 of the original value (£100), then if the bond price falls to £90 the same £5.0 coupon will actually be equivalent to a higher 5.55% based on the new price (£90).

This means that the 'yield' is 5.55% and has risen by 55 basis points (from 5.0% to 5.55%).

As can be seen, therefore, yields are an extremely accurate way of measuring what the 'market' thinks about the future course of inflation.

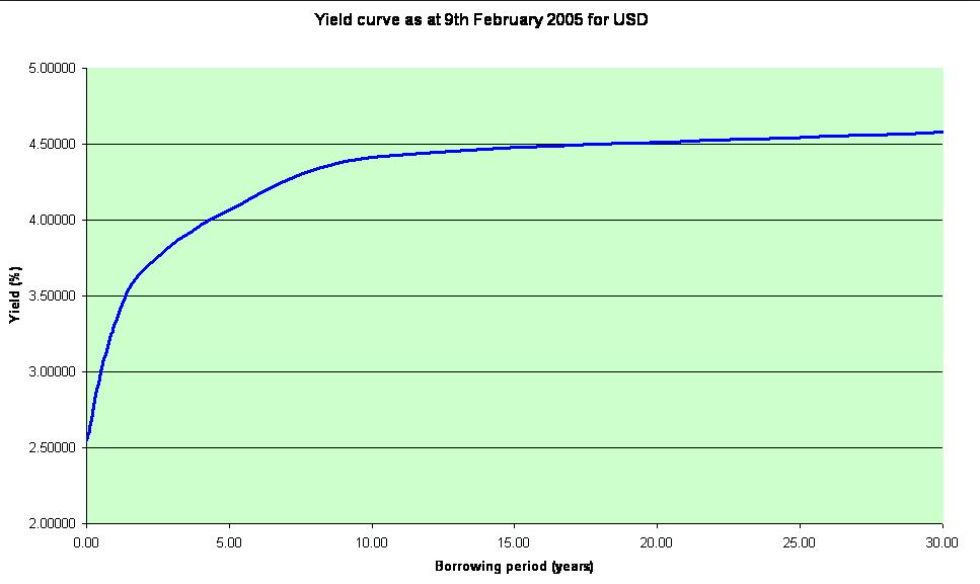

In normal market conditions, yields get steadily higher as the bond's maturity period lengthens, to compensate for the increased risk of inflation eroding the principle over a longer period of time.

The yield curve is composed of a standard graph with the x-axis representing bonds of differing maturities from short to long, and the y-axis the yields on the different lengths of bonds.

Normally the curve should rise and steepen as it moves from left to right and maturities get longer as shown in the chart below:

Sometimes the curve looks different, as it does right now, when it has flattened, sometimes it can even become inverted.

Flat as a Pancake, but Not Yet Inverted

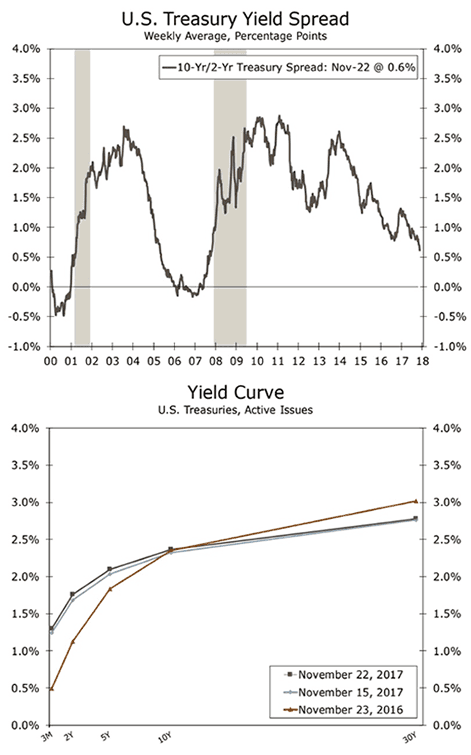

The US treasury yield curve is flatter at the current time and there are concerns this flatness could lead to the inverted yield curve, which we noted earlier, is a precursor to recession.

Recession would inevitable mean the prospect of lower interest rates at the Federal Reserve, which would in turn send the Dollar lower.

The reason is simple - if the curve is getting flattened it means longer-term bond yields are low, which means investors don't think inflation will rise much longer-term, and a lack of inflation longer-term is usually taken as a sign of low growth.

The flattening is highlighted by the narrowing difference between the 2-year US government bond yield and the 10-year yield, which has gone from 85 basis points in late October to 57 basis points on Tuesday, November 21.

Source: IHS Global Insight, Bloomberg LP and Wells Fargo Securities

But, analysts are sceptical that the flattening yield curve will morph into an inverted curve.

"The flattening in the yield curve we have seen in recent weeks does not appear to be a precursor to an inversion. Instead, the flattening appears to be driven by technical concerns," says Wells Fargo's Schumaker-Krieg.

"Some argued that a flatter curve signaled that the US economy may be approaching the end of its current expansion. We disagree," says Philip Wee, an FX analyst with DBS Group Research.

The reason Wee does not agree that the flattening curve is a sign of recession is that this time the flattening curve has not resulted from a fall in longer-term bond yields, but to a rise in shorter-term yields as a result of a higher growth expectations in the short term, spurred by the Federal Reserve's intentions to raise interest rates more vigorously than previously expected.

The Fed raises interest rates to combat rising inflation, so its decision to increase them more aggressively recently is seen as a thumbs up for the economy.

Another reason why Wee does not think the flatter yield curve is pointing to a recession is that stocks keep rising, and this must mean that investors are hopeful for future growth, otherwise, they would be selling stocks.

"The three major US stock indices – Dow Jones Industrial Average, S&P 500 and the Nasdaq – all closed at record highs yesterday. US real GDP growth has been above 3% QoQ saar for two straight quarters into Q3. We expect US growth to stay above its post-crisis average of 2.1% in 2018 and 2019," says Wee.

Confidence in the Fed

The view of ACLS Global Chief Strategist Marshall Gittler is similar as he does not regard the flatter curve as a cause for concern.

"It’s another down day for the Dollar. The extremely flat US yield curve – flattest it’s been since the 2008 Global Financial Crisis – has been keeping the dollar from rallying. Does the flattening yield curve signify market fears of a recession?" asks Gittler.

Actually not, concludes the strategist, rather, the flatter curve due to lower yields in longer-dated bonds is actually indicative of newfound investor confidence that the Federal Reserve will be able to keep inflation under control over a longer period.

"Or does it simply indicate that the market has confidence in the Fed and believes that it’s likely to continue to raise rates, which should keep inflation under control going forward?" he asks.

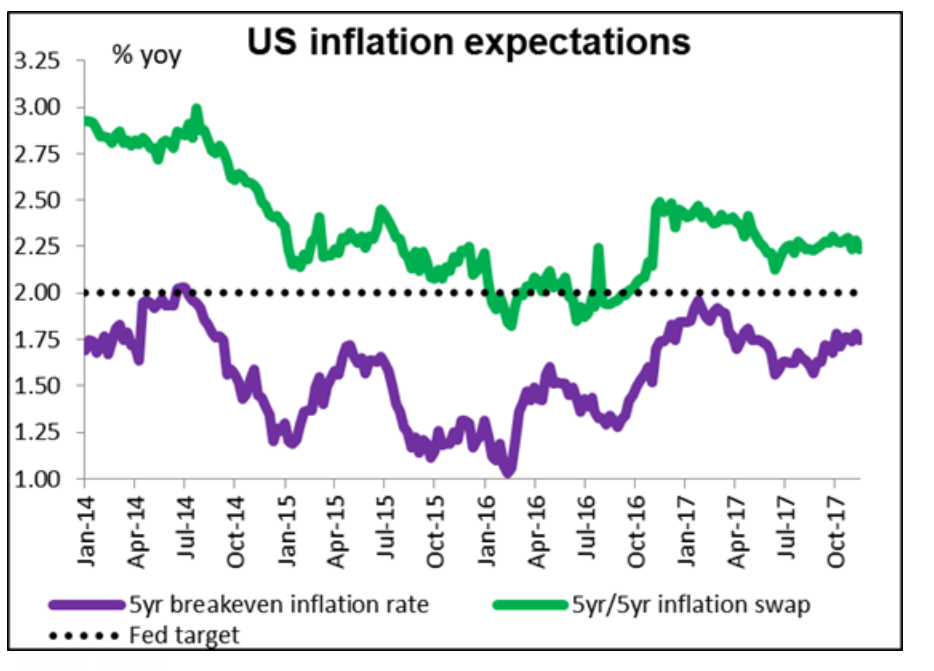

US Inflation expectations have not suddenly sunk in the long-term over recent weeks, he argues, "which leads me to think that it’s the latter – confidence in the Fed."

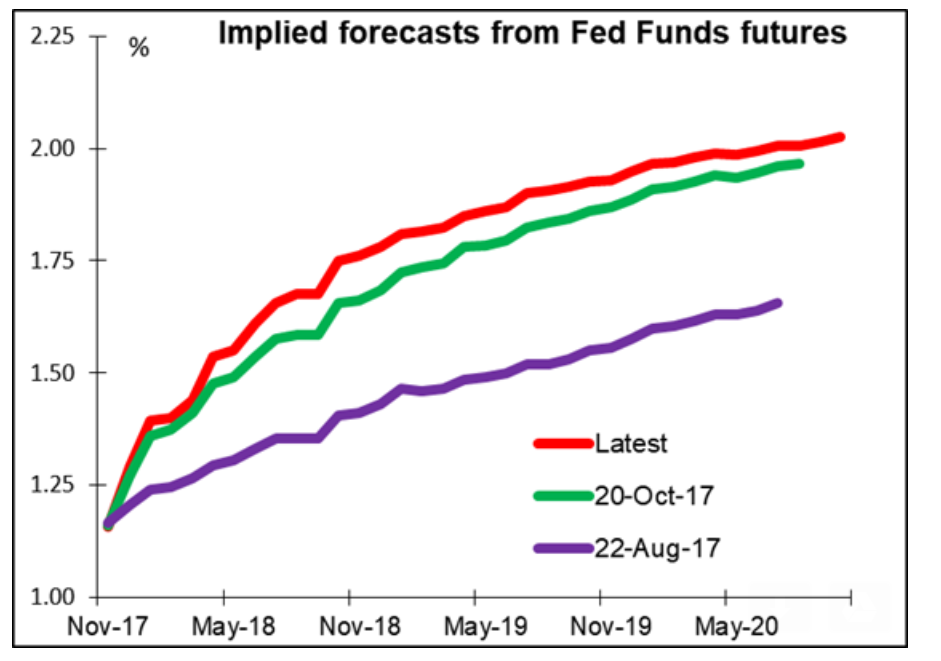

Fed's Funds Futures are a financial derivative which illustrate expectations about when the Federal Reserve is likely to raise or lower interest rates

Fed Fund Futures are now illustrating via their price that the Fed is looking to increase interest rates more steeply in the future, indicating higher - not lower - inflation expectations.

Gittler concludes that, if anything, the market is signaling its time to buy not sell the Dollar.

"Given that the flattening yield curve is a vote of confidence in the Fed and not a signal of an impending recession, I think it should be a reason for the Dollar to rally, not weaken," he says.

Chasing Emerging Market Risk

ING's Chris Turner explains the lack of upside in the Dollar despite the move higher in short-term yields as a sign investors are diversifying and, "chasing growth stories globally."

"Instead it seems unhedged positions in global equity markets look a bigger driver of FX right now. USD/Asia, in particular, is starting to break lower as investors chase growth stories more globally," says Turner.

He also sees little scope for further upside in shorter-term yields without an inflation breakout, suggesting a more cautious approach to buying the Dollar

"And with one Fed hike this year and two next year (March and Sep) virtually priced, it is questionable how much higher short-dated US rates can move right now, without an inflation break-out," says Turner.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.