- The Dollar is being tipped to rise in Q2 especially against AUD, CAD and NZD

- Greater financial market volatility and slowing global growth are factors

- The Euro and Yen to weaken less as hunger for carry-trading decreases

© RCP, Adobe Stock

The Dollar is set to rise over the next three months, especially versus the commodity block currencies and even safe-havens such as the Euro and Yen, forecasts Mark McCormick chief currency strategist at TD Securities.

A mix of increasing market volatility due to combination of rising US interest rates, economic policy uncertainty a la Trumponomics and a broad-based global economic slowdown from the peak of late 2017 is likely to weigh on the commodity block of currencies.

This includes the Australian, Canadian and New Zealand Dollars but an US Dollar recovery could be felt by the Euro and Yen says McCormick.

The upshot of it all is that the previous fears of 'Row' (Rest of the World) growth eclipsing the attractiveness of US assets and leading to a fall in the Dollar may not be as marked, and - in the short-term anyway - could lead to a bounce of 2-3% in the Dollar Index.

"It's all about growth. For now, this backdrop favors a modest overweight in the USD versus the dollar bloc," says TD's McCormick, adding, "uur immediate setup is that the market continues to ignore some positive economic factors that underscore the room for a modest correction in both the EUR and JPY, leaving room for the DXY to carve a 2-3% bounce at the start of Q2."

Soon-to-be-released March PMI's - survey-based leading indicators of economic activity - could be key in this regard as should they show a general global slowdown it may help dispel the idea that RoW is likely to continue outperforming and actually support the Dollar.

March PMI's for some regions have already been released such as the Eurozone, which were disappointing when compared against previously exceptional releases.

"The March round of PMI will offer a nice test on whether the global story is losing momentum but early signs point to some lost acceleration in Europe against some firming on the US side," says McCormick.

But it is not just PMI data, a further possible counterweight to growth may come from the increased market volatility we have been witnessing of late in the large stock market sell-offs of the last few weeks.

This volatility itself could trigger a slowdown in growth. This is particularly the case now that bad news is no longer equated with an increase in monetary easing and therefore stock market gains.

Increasingly it seems all news, whether good or bad indicates movement to normality, higher interest rates, more expensive borrowing costs, and to a greater or lesser extent is, therefore, negative for stocks.

Volatility is likely to extend because no-one sees a return to the days of easy money.

In current conditions TD Securities see the Dollar as coming out on top despite the risks that falling stock prices will lessen inflows from foreign investors in the US stock market.

Indeed there is also evidence that the US stock market is inversely related to the Dollar.

Increased risk-appetite tends to be positive for stocks but negative for USD which still has strong safe-haven qualities.

This is borne out by seasonalities which show that April is on average the weakest month in the calendar for USD and at the same time the strongest month for the S&P 500.

For TD the broader decline of the RoW story is clearly more significant to supporting USD, at least in Q2.

McCormick's views about growth and USD are echoed by Daniel Been, chief FX strategist at ANZ Bank, who sees "growth leadership" rotating back to the US Dollar as markets become increasingly more focused on growth.

"Growth leadership is set to rotate back to the US, while the absolute level of growth is also set to ease. Together these should continue to drive under-performance in cyclical and commodity currencies," says Been.

As evidence of US growth outperformance Been points to the recent ISM report moving higher "in a world where consistently other countries saw deceleration."

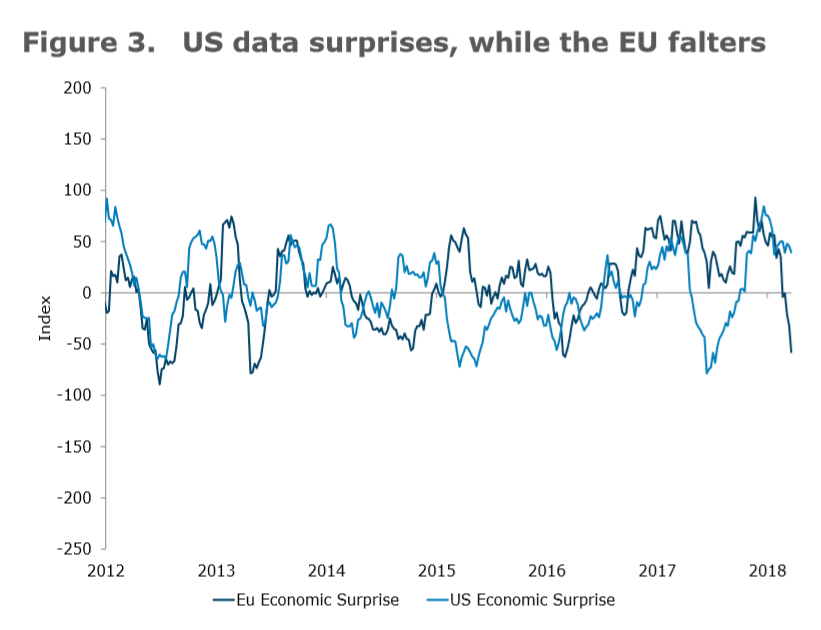

The chart below shows the widening divergence between US and Eurozone net economic data surprises.

Backing the Dollar going forward, Taimur Baig, Chief Economist with DBS, Singapore's largest bank, says he sees the US economy doing better than Europe (as per the economic surprise index graph a) while the Fed's policy of raising interest rates should also prove supportive.

"Contrary to our call a quarter ago, DXY weakened 2.5% in Q1, but we see no reason to remove our bullishness on the greenback," says Baig.

"Some degree of Dollar repatriation to take place around the tax-reform measures (enacted late last year), protectionist skirmishes to continue, and rate differential between the US and the rest of major industrialised economies to widen," are further reasons given by Baig to expect a stronger Dollar.

It's Getting More Expensive to Borrow, and this Could Favour the Dollar

As global central banks step back from offering loose money supply conditions, credit conditions, particularly offshore dollar funding costs have tightened, although that may simply reflect some heightened issuance of Treasurys and commercial paper.

"There is however no going back as far as funding conditions are concerned. For companies and sovereigns preparing to issue or rollover debt this year, chances are high that progressively higher cost would have to be paid," says Baig.

The rise in global borrowing costs will arguably hurt currencies of countries which have higher budget and trade deficits (which must be financed) and support surplus nations' currencies, such as, for example, the Euro.

Greater asset volatility may also lead to gains for safe-havens such as the Yen, USD itself and the Euro from repatriation flows as spooked investors sell riskier holdings and return funding.

Less predictably low interest rates in fewer countries will reduce carry trading anyway which was such a big influence on FX during the low-interest rate years.

Carry involves borrowing in a currency where interest rates are low and investing that money in a currency where interest rates are higher. The difference in interest earned and interest paid is the profit, all other things being equal.

Given carry trading is funded by selling low-yield 'funding' currencies such as JPY, USD and EUR these will gain a boost from not being sold as heavily.

Based on this reasoning, overall, ANZ's Been is bullish USD as we have said, but also JPY and EUR, although it is not clear which will win out versus the greenback.

"For some of the lower yielding surplus currencies, the outlook remains pretty good, especially in the JPY, where valuation adds a further tailwind," says Been.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.