- Eurozone growth rate extends decline in 2018

- 'Growing Pains' and overly strong Euro main reasons

- But economists caution not to read too much into most recent data

© Paolese, Adobe Stock

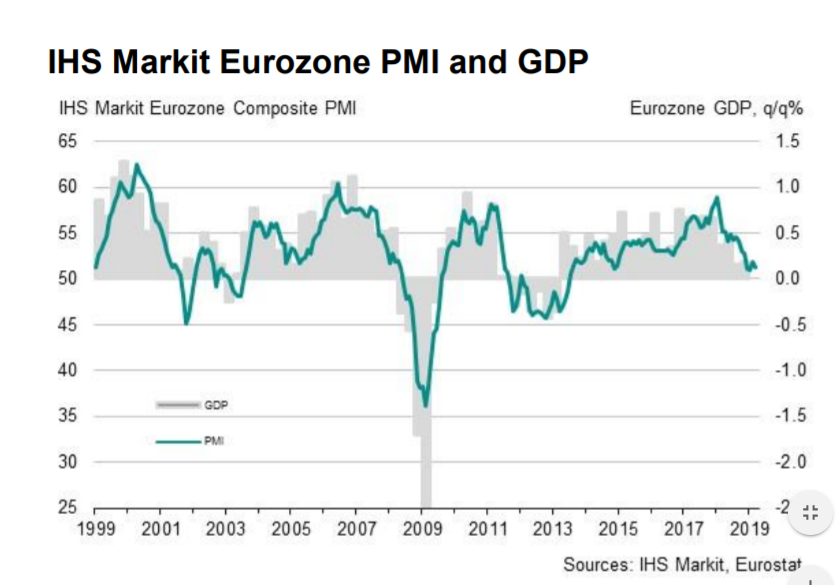

Eurozone business activity expanded at a slower-than-forecast rate in March marking two successive months of disappointment.

The Composite PMI is made up of the services and manufacturing PMIs and it fell to 55.3 in March from 57.1 when a shallower decline to 56.7 had been foreseen.

The Eurozone services PMI slowed to 55.0 in March from 56.2 in the previous month of February; this was deeper than the decline forecast by economists to 56.0. Eurozone Manufacturing PMI, meanwhile, slowed to 55.6 from 58.6 in the previous month, which was a big miss from the 58.1 expected.

In their official report, the survey data compilers IHS Markit report the data shows business activity in the Eurozone slowed at its fastest rate in over a year and the Composite index fell to a 14-month low.

The 'New Orders' subcomponent of the survey, which is a strong leading indicator of future growth also fell.

The 'Employment Growth' component remained more robust, however, continuing to register, "one of the largest monthly rises seen over the past 17 years." Job gains were reported in both manufacturing and services.

PMIs measures levels of business activity via a survey of purchasing managers, who have a unique insight into business conditions due to their pivotal role.

The slowdown in the pace of growth was caused by a mixture of "capacity constraints" as backlogs of unfinished work rose, and the stronger Euro, which has reduced the attractiveness of Eurozone-made export products, according to Survey compilers IHS Markit.

The data suggets the Euroboom of 2017 - a period of exceptionally strong and consensus-beating economic growth rates - might be over. Considering the Euro exchange rate complex rose rapidly alongside the outperformance in growth rates, there could be an argument to be made that the single-currency might not enjoy the kind of fundamental support in 2018 that it did back in 2017.

Nevertheless, it must be pointed out growth in the region remains comfortably in expansion territory and declining growth rates come off a series of record-highs:

Reasons for the Slowdown

The survey indicated that despite increased employment, 'capacity constraints' remained a bottle-neck issue to faster growth with backlogs of unfinished work rising to a greater extent than in February.

"Manufacturing vendor delivery times again lengthened to one of the largest extents over the past 18 years, reflecting widespread supply chain delays amid strong demand for inputs," says IHS Markit.

Both 'input' costs ie raw materials and 'output' costs of finished articles continue rising at a fairly rapid pace, due to a combination of commodity price inflation as well as higher employment costs (pay) and operating costs.

The 'Expectations' (of future growth) component fell to a 4-month low.

"The loss of momentum since the buoyant start to the year has been quite dramatic," says Chris Williamson, Chief Business Economist at IHS Markit.

The economist cautions against an overly pessimistic interpretation of the data, saying that a major factor in the loss in growth momentum may be due to 'growing pains', which "resulted from the strength of the recent growth spurt."

Hegoes on to add, "supply chain delays and raw material shortages were often reported to have stymied production in manufacturing (delays in German supply chains are currently more widespread than at any time in the survey’s 22-year history)," thus the conclusion may be that this is not be indicative of a broader-based economic slowdown.

A further sign the loss of steam may be due to roll-out issues was the admission by respondents of a widening skills gap limiting production.

Yet, these are not the only reasons.

Williamson says the "strong Euro" has contributed to a halving in export order books, "since the end of last year."

The economist concludes the region has peaked "around the turn of the year and the region is settling into a slower, but still robust pace of expansion."

He also adds that price pressures are balanced as rising domestic inflation has been offset by the falling cost of foreign imports due to the strong Euro.

In response to German and French PMI's which were released slightly before the Eurozone data, but, nevertheless, were closely indicative of the EZ data, Pantheon Macroeconomic's chief Eurozone economist Claus Vistesen said the data for the two largest countries was indicative of a slowdown from a peak but not the end of the growth cycle altogether.

"This index is volatile, however, and could easily swing back in coming months. The details (in Germany) broadly tell the same story as in France. Growth remains robust, but the pace has slowed, especially in manufacturing orders following a record-high pace at the beginning of the year," said Vistesen.

Reaction from the Euro

The Euro weakened after the release of the data, with EUR/USD falling from a pre-release 1.2355 to a post-release low of 1.2340. GBP/EUR, meanwhile, rose from 1.1465 to a peak of 1.1485 but was pulling back into the 1.1470s at the time of writing.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.