Deutsche Bank are forecasting further US Dollar strength but analysts open up the prospect of President Trump's administration interevening if the currency gets too strong.

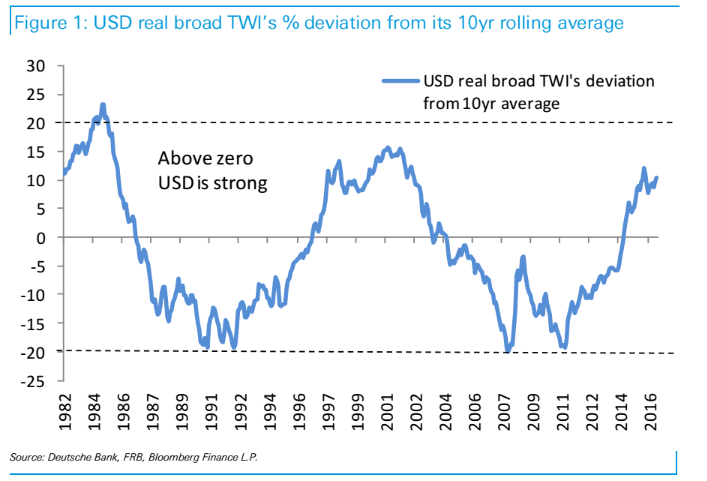

The Dollar is already quite strong, standing at 10% above its long-term moving averages, and whilst this is not a level where past administrations have become anxious about its negative side-effects, it is not far from, such a level.

“Historically, clear USD overshoot terrain entails the real broad USD TWI tracking around 20% above long-term moving averages, or ~10% above current levels,” say Deutsche Bank analysts Alan Ruskin in a recent note.

A good way to measure when the dollar is overbought is to use the Trade Weighted Index and check for when it enters the zone between 15 and 20% above its long-term moving averages.

The above shows that the currency can be considered strong but it is within the remit of its long-term cyclical range.

Further strength is possible based on historical precedent alone.

Ruskin believes the currency could probably appreciating another 5% above current levels.

However, the analyst is more concerned over whether the Trump administration might actively try and target Dollar levels.

"It is possible that a strong USD will be worn by the coming administration as a badge of honour – a signal of global confidence in “Trumpism,'" says Ruskin.

Although he sees as more probable that, “policymakers will wish to keep USD strength in check,” because it is more helpful to trade and manufacturing.

At the root of the problem is that a strong US Dollar will not be very compatible with Trump’s protectionist trade agenda as it will make US exports uncompetitive, whilst continuing to favour imports.

Complicating the picture, however, is that the President’s much-anticipated fiscal stimulus drive will conversely benefit from a strong Dollar, as it will help keep inflation under control.

The apparent contradictory needs of Trade and Inflation perhaps make it less likely the administration will take a strongly interventionist a stance.

Ruskin notes:

“A strong USD is potentially a vital disinflationary offset to likely reflationary fiscal policy enacted when the economy is already at full employment.

“Not allowing the exchange rate to play that ‘safety valve’ role, would risk a further blow-out in bond yields.

“We believe this is one of the more persuasive arguments for avoiding the temptation to use a weaker currency to support manufacturing employment in current circumstances.

Cures for an Overly Strong Dollar

Nevertheless, Ruskin does not rule out intervention altogether.

The first line of defence against an overvalued Dollar, however, would be a dropping of any positive rhetoric about a strong Dollar being “good for America”.

The next would be actively talking down the dollar.

The third line of defence would be active intervention.

Another option might be to use monetary policy.

The final option could be to leave the dollar’s value to be determined by market forces.

Ruskin highlights the fact that the US is normally a vociferous exponent against currency intervention amongst the G20, so if it were to go against its own advice that might pave the way for an aggressive currency war:

“Since Donald Regan presided over Reagan’s initial non-interventionist FX policies in the early 1980s, the US has tried to direct the developed world and more recently the G20 countries, toward freely floating exchange rates with minimum intervention or intervention only under extreme circumstances.

“To back away from this approach, would open the door to interventionism everywhere and overt FX manipulation.”

Despite the US’s anti-interventionist stance, there have been exceptions to the rule, such as between 1984-85 when it was in obvious overshoot terrain.