The pound to dollar rate (GBP/USD) continues to recover from its February multi-year lows as markets believe they have priced the exchange rate at appropriate levels when it comes to the EU referendum.

However, one of the UK's leading independent analyst houses, Capital Economics, questions whether markets have become too complacent with regards to the potential downside that lies ahead for the UK currency.

The pound to dollar exchange rate has pushed higher to record levels around 1.44 this week; up from the multi-year lows at 1.38, hit soon after the referendum date was announced and 'Brexit Fever' reached its zenith with the entrance of Boris Johnson into the 'Out' camp.

The recovery has also been assisted by the US Federal Reserve who have pushed back expectations for the timing of their next interest rate.

This suggests investors once again have the luxury of focussing on the US side of the equation now that the theme of Brexit has lost its bite.

“At first glance, evidence of a Brexit effect seems to have subsequently diminished more recently,” says Oliver Jones at Capital Economics, who has recently updated clients on the nature of the shifting sands posed by the EU referendum.

Indeed, there has actually been little to stoke the Brexit story of late, with bookies Betfair placing the odds of a Brexit at 33 pct, a figure that most other bookmakers are quoting.

Two voter-intention polls released over the past week have shown a substantial lead for the 'In' campaign, with the latest showing an 8 percentage point lead over those pushing for an exit from the bloc.

Latest Pound / US Dollar Exchange Rates

| Live: 1.3401▼ -0.06%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.2945 - 1.2999 |

**Independent Specialist | 1.3213 - 1.3267 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

The Pound is Back at Fair Value Against the US Dollar

There has always been an assumption that once the 'In' vote is secured, the pound will bounce back sharply.

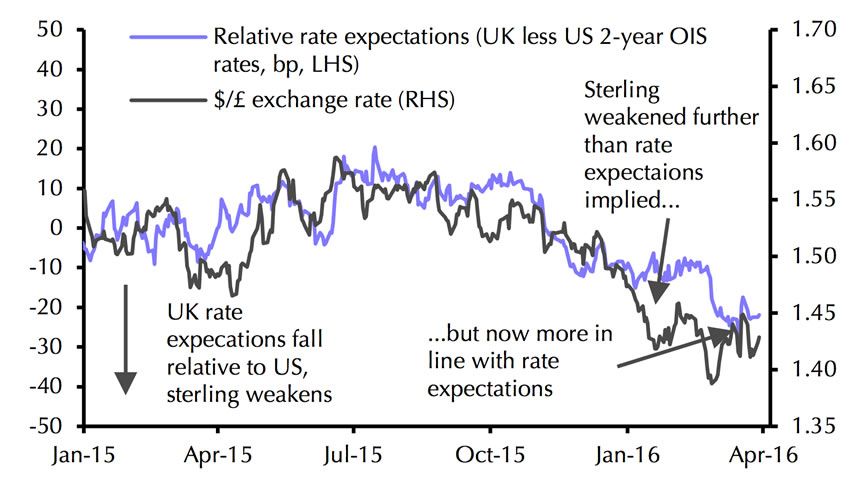

The view was based on the observation that sterling was becoming undervalued based on where it traded in relation to interest rate diffirentials.

The difference in interest rate expectations between the United States and United Kingdom have long been a key determinant of GBP/USD’s value as interest rates are held to ultimately reflect the nature of the underlying economy.

Interest rate diffirentials and the exchange rate tend to move in lock-step.

We have reported over recent months that the exchange rate has moved away from interest rates differentials suggesting that the pound was getting out of kilter with underlying fundamentals.

In short it was becoming under-valued; the gap between fair value and reality has been referred to as the ‘Brexit premium.’

Capital Economics note that the gap has since closed, confirming the GBP to USD exchange rate is now back around fair value:

There are two implications here. One is that should the 'In' vote win, there is not much space for a massive rebound.

The second is that the downside risks may have faded. Has the worst now passed for sterling then?

Not likely.

Rather, what the convergence of the GBP/USD and interest rate differentials suggests is that interest rate markets have merely caught up with the pound.

“Even the most optimistic commentators on the long-run impact of a Brexit on the UK economy generally acknowledge the potential for some short-term disruption in the aftermath of a leave vote. If the near-term shock turned out to be particularly disruptive, it wouldn’t be at all surprising if the MPC decided to keep rates on hold for longer than it would otherwise have done, or even cut them,” says Jones.

The Bank of England warned this week that there were indeed risks to the UK financial system posed by the uncertainty a Brexit would bring.

We would most likely see the Bank delaying any interest rates in the event of an exit to maintain financial stability. Lower interest rates for longer = a lower British pound for longer and hence why fair value has been pushed lower.

Are Traders Becoming Complacent on Brexit Risks?

It would be incorrect to suggest we have heard the end of Brexit when it comes to the pound.

Both upside and downside risks are still substantial argue Capital Economics.

“We think there is scope for markets to move significantly further when the result of the vote becomes known on 23rd June,” says Jones.

Proof that Markets Remain Alert to Brexit

Capital Economics note the following tell tale signs that big moves are anticipated by the financial markets:

- investors have been buying put options as insurance against a fall in sterling in the event of a Brexit, as demonstrated by the sharp drop in the risk reversal on six-month $/£ options, which expire three months after June’s vote

- In contrast, the risk reversal on one-month options, which expire before June 23rd, has hardly moved, suggesting that it is the EU referendum which investors are worried about

- despite the recent rebound, equity markets also appear worried about the possible impact of a Brexit. Again, investors have been purchasing put options in order to protect themselves against a drop in the FTSE 100 should the UK vote to leave the EU, as 180-day option-implied volatility for the index has spiked recently.

Forecasting GBP to hit 1.20 Against US Dollar

Jones says that if a ‘Brexit premium’ does still exist, then there is scope for it to be reversed, boosting UK assets and sterling, if the UK votes to stay in the EU.

But other concerns, including the current account deficit, could prevent the pound from fully reversing its recent fall.

“Meanwhile, given bookmakers’ odds and polls currently point to the UK voting to remain in the EU, we don’t think that markets are fully pricing in a Brexit,” says Jones, “Accordingly, sterling could plunge significantly further – perhaps to $1.20 or so – in the event of a vote to leave.

Equities may well drop too, though based on markets’ reaction so far, corporate bond spreads might be less affected.