Image © Adobe Images

Inflation is running hot, but the takeaway is that the Federal Reserve has nothing to panic about.

The dollar is softer on the day the U.S. announces inflation rose 0.5% in June alone, taking the headline annual rate to 4.2%. All were in line with expectations.

That's well above the Fed's target and is consistent with a repricing in market expectations for the Fed to raise interest rates in the coming months.

That shift in expectations has underpinned the dollar's recent renaissance, which leaves it as the best-performing G10 currency for the past month.

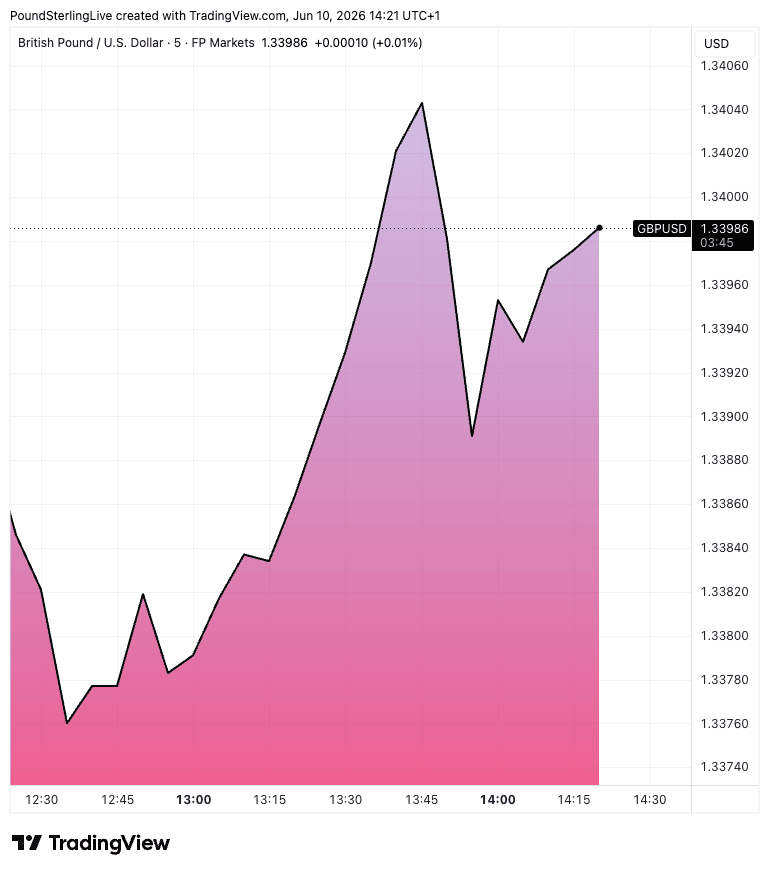

However, if we look at the price radar, the dollar is under pressure against half of the G10 basket in the wake of this week's main economic calendar event, which includes a loss on the day against the GBP and EUR.

Above: GBP/USD in the wake of the inflation release.

There are a few reasons for this.

Firstly, the market was primed for a strong reading following last week's run of hot data. That simply means the market requires increasingly awesome beats.

A mere on-target print won't shift the dial for bulls, so some 'sell the fact' behaviour is possible.

Secondly, in the details, there is some softness. Noticeably from core inflation, where a 0.2% m/m increase was actually less than the 0.3% expected and half of what was reported in April.

In core, there is little evidence of concerning trends building.

Thirdly, it's hard to see the inflation data running away from here, as there are notable base effects for the coming months that will likely cap the headline reading for U.S. CPI.

June 2025's +0.3% will drop out of the headline, while for July the drop off from a year earlier is +0.2%, for August it's +0.3% and for September it's +0.3%.

That means a steady run of +0.3% m/m readings will mean headline annual inflation is mechanically limited at 4.2%.

And then, there's the prospect of genuine headwinds as petrol prices peak and start subtracting from the monthly headline.

"There's really no sign - whatsoever - that U.S. inflation is overheating. That has implications for the Dollar," says Robin Brooks, Senior Fellow at the Brookings Institute.

"Just imagine what'll happen to inflation when the war ends and oil prices fall. I think markets are wrong to price hikes for the Fed. Very wrong," he adds.

If Fed rate hike bets have reached their ceiling, it's not hard to argue that the dollar will find it harder to rally.