Image © Adobe Images

Foreign exchange market snapshot at the London open.

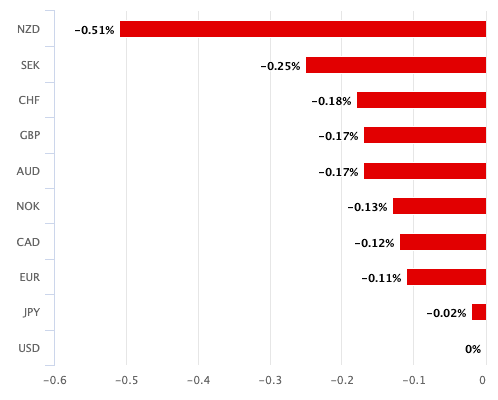

GBP. Pound sterling is looking well supported against the euro and dollar amidst an improved risk backdrop. Trump confirms peace talks with Iran "in final throes", sees a "very, very good deal." No British data for release this week, with eyes on the crosses as U.S. inflation and ECB decision set to take the limelight.

USD. U.S. dollar is the day's underperformer as sentiment improves. Last week's AI-linked stock selloff fades. Brent crude prices down 0.9% to near $93.4 / barrel after Iran and Israel pledged to ease strikes against each other. Economics are back in focus midweek when the U.S. releases inflation numbers.

EUR. EUR/USD touched 1.15 support Monday but has since recovered to 1.1550 amidst USD pullback. Eyes on ECB decision Thursday where a rate cut is expected. Howevever, risks are that the ECB strikes a cautious tone. Regardless of ECB, it's still the USD side of the equation that matters the most, which places emphasis on Wednesday's U.S. inflation data.

AUD. Looking better supported as risk sentiment improves, Chinese exports stronger than expected, despite the Iran war shock, confirming demand for Chinese exports continued to hold up well. Export growth rose to 19.4%/yr in May, beating estimates of 15%/yr, which is good for the China-linked AUD. Solid demand for AI hardware underpinned Chinese exports more broadly. Exports of semiconductors and high‑tech products surged by 111%/yr and 51%/yr in May.

NZD. Top performer of the day thanks to its high-beta response to improved investor sentiment. Trump's Iran progress, Chinese data underpin.

CAD. Loses some ground as it tracks USD lower on the crosses. All eyes on Wednesday's Bank of Canada; expect to leave the policy rate unchanged at 2.25%. Bank will be comfortable with a modestly accommodative monetary policy stance to counter recession, even if inflation is uncomfortably high. CAD at risk of pushback against rate hike bets.