Image © Adobe Images

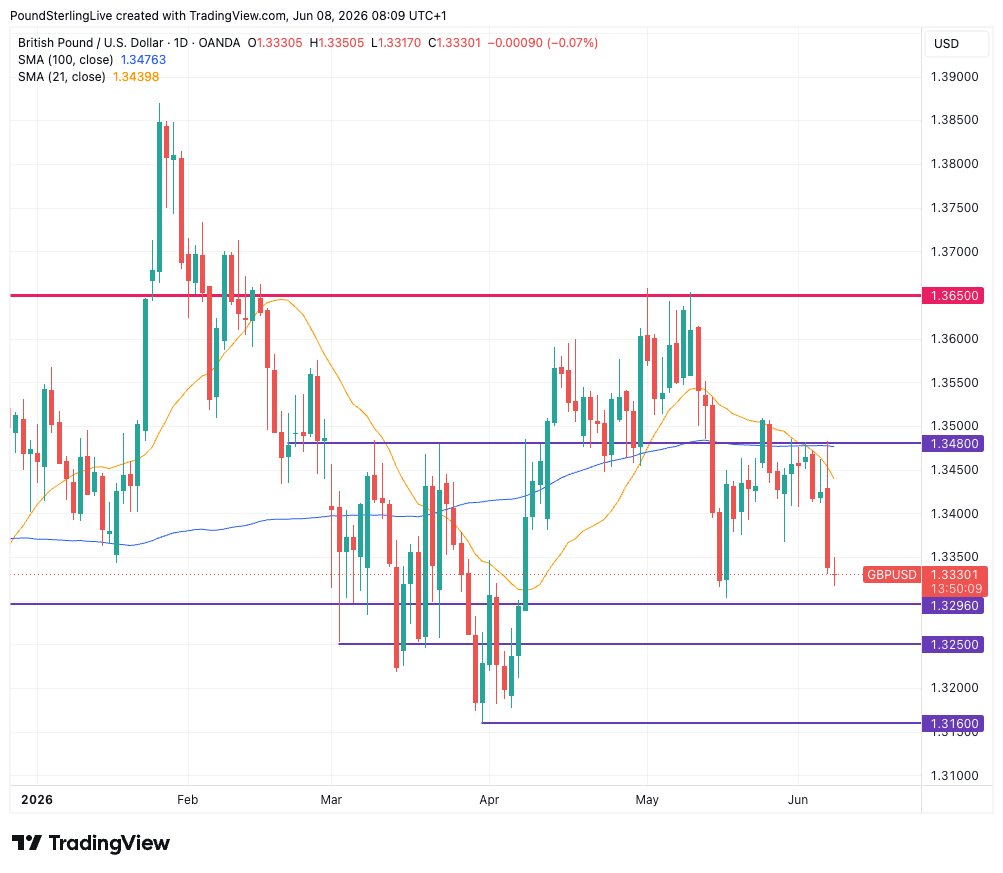

Week-ahead forecast: The balance of probabilities favours further downside pressure while GBP/USD remains below its 21-day and 100-day moving averages.

The dollar is pushing ahead on Monday, helped by the tailwinds of Friday's bumper jobs report and an escalation in the Middle East conflict.

The Greenback's advance squeezes the pound to dollar exchange rate down to 1.3329 at the time of writing, ensuring the immediate focus is on whether a looming test of support at 1.3320 can withstand renewed selling pressure. That's a graphical horizontal support line based off the May low; it also served as a support-resistance pivot for much of March-April.

A break lower here likely accelerates losses toward 1.3250 and potentially 1.3160.

Sterling would need to reclaim the 1.3440-1.3480 resistance zone to neutralise the bearish bias, but for now the technical outlook remains tilted modestly in favour of the dollar.

A deterioration in the wider investor mood underpins the dollar at the start of the week, with oil prices rising in response to renewed fighting in the Middle East, as Isreal and Iran trade blows.

"Monday’s market movements are set to be dominated by reaction to the escalation in Middle East tensions, with Iran striking Israel followed by Israel retaliating," says a morning market note from Lloyds Bank.

The dollar is a safe-haven petrocurrency that tends to gain when oil prices rise amid Middle East tensions.

Bumper Jobs Report Leaves its Mark

Friday's 0.63% drop on the daily GBP/USD chart certainly leaves a mark and will underscore a turn in momentum to the downside.

It's a reminder that the pro-USD tone to markets extends beyond just the Middle East: "This isn't the only important theme for rates markets though, as the aftermath of Friday's bumper employment report ripples into expectations for Fed Funds," says Lloyds.

"The risk-off sentiment continues after US stocks and bonds fell sharply on Friday, driven by a confluence of factors, including media reports that Meta was set to raise equity, follow-through pressure after Broadcom’s underwhelming AI revenue outlook, a sharp unwinding in semiconductor stocks after the recent rally, and a stronger-than-expected US jobs report that intensified worries that the Federal Reserve could raise rates to head off inflation risks," says Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.

The dollar rose against the pound, euro and G10 peers after the U.S. Bureau of Labor Statistics said the economy added 172K jobs in May, easily exceeding a consensus market bet for 82K jobs to have been created during the month.

"The much stronger than expected U.S. jobs report has had the obvious impact with front-end rates and the dollar stronger," says Derek Halpenny, Head of Research Global Markets EMEA at MUFG Bank Ltd.

Money markets went into the jobs report seeing approximately 15bps of hikes priced for the December FOMC meeting but now they see about 30bp, meaning a rate rise by year-end is now fully anticipated.

Whether that pro-USD repricing can extend this week will likely depend on the flavour of the inflation numbers due out of the U.S. on Wednesday.

U.S. CPI to Tee Up Crucial Fed Meeting

U.S. inflation data forms the central focus of the coming week as it will offer the final set of hard data to the Federal Reserve's policy committee, which will meet next week and deliver its first decision under new Chair, Kevin Warsh.

Headline CPI is expected to have risen 0.3% m/m in May, down from 0.6%, but that'll be enough to help heave the annual rate rise to 4.2% from 3.8%.

Core, is seen rising up to 0.5% m/m from 0.4% in April, helping the y/y rise to 2.9% in May from 2.8% previously.

These data are too hot for the Fed to ignore, and it should, at the very least, abandon its 'dovish' guidance that saw it anticipating a rate cut as the next move.

For the dollar, that's supportive and underpins the downbeat stance we adopt on GBP/USD in the coming days.