Image © Adobe Images

U.S. bond yields should retain an attractive sheen for international investors, whatever the outcome of the Federal Reserve policy decision and update, ensuring the Dollar can continue to strengthen against the Euro, Pound and other currencies.

According to a number of analysts we follow, the Federal Reserve will not offer the kind of game-changing shift in guidance required to knock the Dollar from its trend of appreciation.

Steve Englander, Head of Global G10 FX Research at Standard Chartered in New York, says the Fed will reiterate data dependence but retain a tightening bias.

The decision is due at 19:00 BST on Wednesday and the market is poised for the Fed to maintain interest rates at current levels but warn that it stands ready to raise interest rates again, ensuring investors aren't tempted to bring forward expectations for rate cuts.

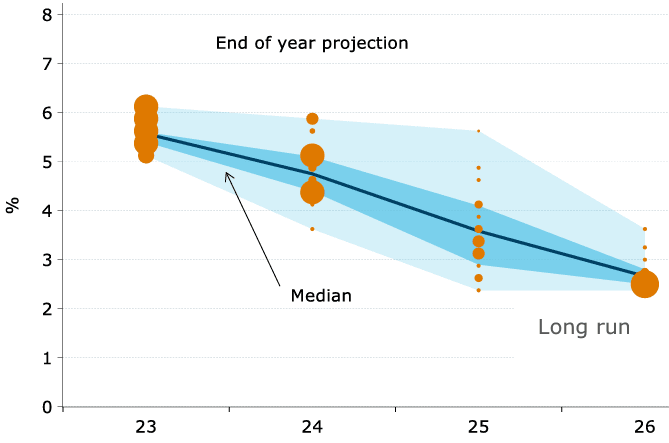

One way it can achieve this is by shifting its own projections for where it sees future rates sitting: Standard Chartered expects the Fed to show one more 2023 hike in the much-watched dot plot chart.

Analysts at the bank also look for the Fed to remove guidance that indicates the potential for one 2024 policy rate cut from its projections.

"FX and FI markets may see this as slightly hawkish, in sharp contrast to the ECB last week," says Englander.

Above: The dot plot chart allows the Fed to communicate its own projections for where the basic rate is headed. Source: Federal Reserve, Macrobond, ANZ Research. Image courtesy of ANZ.

The Fed decision comes amidst an ongoing trend of USD strength that has pushed the Pound to Dollar exchange rate to 1.24 at the time of writing and the Euro-Dollar rate to 1.07, from 1.31 and 1.12 in July, respectively.

By raising its own projections for future levels in the basic interest rate, the Fed would support U.S. bond yields, which tend to have a mechanical supportive pull on the USD.

"To maintain a proper hawkish tone, we expect the FOMC to remove one of the 2024 eases," says Englander. "The Fed's message will be that higher policy rates remain on the table until the economy visibly slows and inflation is closer to 2%."

Standard Chartered says these views are probably hawkish enough to add further USD support and steepen the 2024 rates curve a bit.

"With the Bank of Japan and Bank of England meeting the day after FOMC, the EUR may be the most promising short," says Englander.

But, "if Powell surprises on the dovish side and if China data continues to stabilise, the big gainers could be AUD, NZD and other commodity currencies," he adds.

Analysts at Morgan Stanley meanwhile warn that any post-Fed weakness in the Dollar will likely fade as yield differentials should continue to favour the U.S. Dollar.

Morgan Stanley's rates strategy team sees scope for U.S. yields to move lower as changes to the dot plot chart reveal a lower neutral rate than the market appears to be pricing in.

They also argue that the market is pricing a higher real yield rate than what's implied by the Fed's projections.

This would weigh on yields and, on balance, be considered a 'dovish' development for the Dollar.

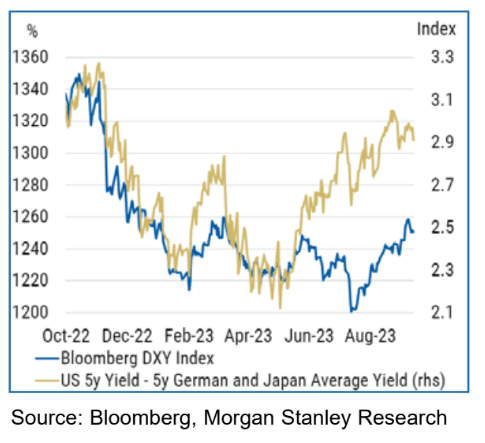

However, the same analysts expect a larger decline in yields in the Eurozone and the United Kingdom than in the U.S., "which should shift yield differentials further in the USD's favour," says Katy Huberty, Global Director of Research at Morgan Stanley.

Above: Yield differentials favour further USD strength says Morgan Stanley. Image courtesy of Morgan Stanley.

"Indeed, our Currency Strategists note that over the past month, the USD has traded below levels implied by yield differentials, which creates significant room for a catch-up USD rally, in their view," she adds.

Therefore, any selloff in the Dollar following the Fed's decision could be considered a kneejerk reaction that would ultimately soon correct.