"Our decision was to move ahead with a 25 basis point hike and to change our guidance, as I mentioned, from 'ongoing hikes' to 'some additional hikes' or 'some additionaly policy firming' may be appropriate" - Federal Reserve Chairman Jerome Powell.

Image © Adobe Stock

U.S. exchange rates were mostly underwater for the period in the final session of the week after the Federal Reserve (Fed) suggested that its interest might rise by less than was previously thought once all is said and done, leading some analysts to anticipate further declines for the Dollar up ahead.

Dollars were bought widely in European trade on Friday after consumer and banking shares led stock indices lower around the world while driving a rally in government bonds, although the last-minute recovery has merely crimped what are still widespread losses for the week overall.

Losses were their steepest and broadest after the Federal Reserve raised the Fed Funds interest rate range to between 4.75% and 5% but signaled for the first time in more than a year on Wednesday that the outlook for borrowing costs is now an open question.

"Our decision was to move ahead with a 25 basis point hike and to change our guidance, as I mentioned, from 'ongoing hikes' to 'some additional hikes' or 'some additionaly policy firming' may be appropriate," Chairman Jerome Powell said in Wednesday's press conference.

"As I mentioned, in assessing the need for further hikes we'll be focused as always on the incoming data and the evolving outlook, and in particular on our assessment of the actual unexpected effects of credit tightening," he added.

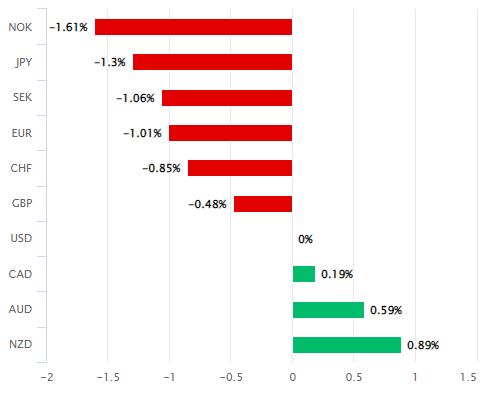

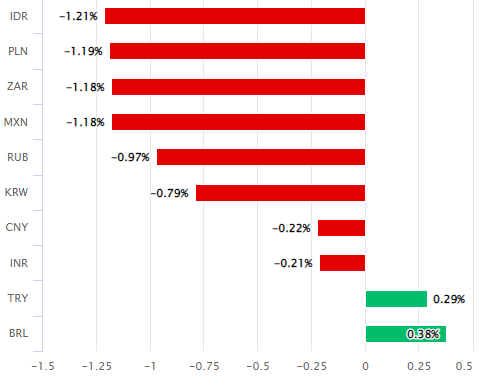

Above: Pound Sterling performance relative to G10 and G20 counterparts this week. Source: Pound Sterling Live.

Chairman Powell noted a significant slowdown in the U.S. economy last year and acknowledged a recent softening of all-important labour market conditions that are both expected to develop further and ultimately help bring inflation back to the two percent target over the coming years.

These outcomes are just some of the effects of the Fed's 475 basis point or 4.75% increase in interest rates since last March, effects that are now expected to be bolstered by recent and ongoing events in the banking system, which are driving a "credit tightening" process by reducing the availability of credit.

Hence why the Fed's forecasts were little changed with the median average projection indicating that Federal Open Market Committee members still envisage only one more increase for interest rates over the balance of the year.

This is why some analysts are now more confident in views and forecasts suggesting that Dollar exchange rates have peaked and are likely to fall further.

There are still nuances in and between these outlooks, however, some of which can be found in whole or part below.

Joe Tuckey, head of FX analysis, Argentex

"Markets will settle into the expectation that the Fed will only hike once more, signaling the start of the “Fed Pivot” that so many dollar bears have waited for."

"For the euro, the ongoing commitment to further hikes from the ECB, scope for resilient data, bullish technical chart action, and an unwind in the dollar strength point toward steady gains in 2023."

"The growing dichotomy between the euro and dollar looks to support our view toward high teens targets for EURUSD by year-end."

"The BoE hike itself is unlikely to drive significant sterling gains, but the pound remains on the front foot as it target the enormous 1.2448 upside resistance."

Jane Foley, head of FX strategy, Rabobank

"Before this month’s financial sector crises, it may have appeared that the effects of higher interest rates were being most acutely felt in countries where household mortgages rates are fixed for short period of time. Certainly, this is a factor which contributed to the pause in BoC policy and had added to talk of a forthcoming pause from the RBA. It is now clear that tighter monetary conditions are having a far greater reach."

"The jitters in the banking sector may have an impact in the lending activities of banks. However, it unlikely that this will be uniform across countries. Currently it appears as if the US banking sector could be more impacted by a tightening of credit conditions in view of the prevailing concerns about US regional banks. If this is the case, it would imply that Fed policy may be more impacted than the policies of European central banks."

"It is too early to draw strong conclusions, but if the FOMC is more concerned about a tightening in credit conditions than European central banks, there could be more impact on Fed policy. In response to the rhetoric of the Fed this week, we have revised down our expectations for the peak in policy. We now see scope for just one more rate hike, compared with a previous expectation of two 25 bps Fed rate hikes. This has negative implications for our USD forecasts."

If you are looking to protect or boost your international payment budget you could consider securing today's rate for use in the future, or set an order for your ideal rate when it is achieved, more information can be found here.

Mazen Issa, senior FX strategist, TD Securities

"An asymmetry should now form in fed funds/terminal [rate] pricing and around the data. Terminal pricing is likely to be capped especially after the Fed acknowledged less need to push it higher given recent banking events. Given the lags to show in the data, the market is likely to be more inclined to look through upside but react to the downside as confirmation bias."

"Note that the USD has seen a sharp flip in its sensitivity to both FF pricing and data surprises. Indeed, the USD is now trading with an eye to the easing cycle (late reds/early greens), not terminal. Should data soften in the near-term, the market may price in more cuts sooner."

"These are key reasons for our USDJPY short. Meanwhile, the EUR is likely to remain firm as euribors — with support from ECB rhetoric to stay the course on tightening (and claim victory over market stresses) — exercise some monetary dominance against curves where CBs have committed to the sidelines."

"Our bearish medium-term USD view should support GBP regardless of the BoE outlook. We think that relative central bank policy is more important on crosses, where we still place GBP on a lower tier relative to EUR and JPY, especially as markets are priced for a 4.5% terminal rate."

Annabel Bishop, chief economist, Investec

"The tone was seen as somewhat less hawkish than commentary coming out early in the month and in February, when market expectations were factoring in a 50bp lift at last night’s meeting, although the recent banking crisis in the US saw a more modest hike."

"Higher interest rates have added to some stresses in the US banking system amongst smaller banks, particularly in the case of SVB which had invested heavily in US treasuries, but had not hedged against changes in their value."

"The FOMC next meets in May (3rd) although the chance of another hike is currently seen around 50% for a 25bp lift, with the Fed statement reading “some additional policy firming may be appropriate”."

"The Fed funds futures have factored in implied rate cuts for H2.23, with July (26th) meeting seeing 80% chance of a 25bp cut, and factoring in a second 25bp cut the FOMC’s November meeting (1st), although expectations will likely remain volatile."

"South Africa’s monetary policy committee (MPC) meets for its interest rate decision at the end of this month, and the FRA curve (Forward Rate Agreement) curve has mostly (but not fully) factored in a 25bp lift in SA’s repo rate."

To optimise the timing of international payments you could consider setting a free FX rate alert here.

Wee Khoon Chong, senior market strategist, BNY Mellon

"The Fed backing away from forward guidance and the persistence of market pricing for a turn in the Fed's policy cycle might be sufficient to put a cap on the US dollar, or leave it to trade within this year's range in the near term. A weak to stable US dollar is likely to benefit Asia FX."

"It might also be viewed as a reason to be positive on regional risk assets. An additional supportive factor for Asia FX, and for EM currencies more broadly, is that they are underheld overall, according to BNY Mellon iFlow scored holdings data."

"While stronger Asia currencies would likely be welcomed by investors, it seems as though other conditions need to fall into place to make the argument for investing in Asia risk assets more compelling. Data from regional stock exchanges continues to point to foreign investor outflows or limited participation."

Joseph Manimbo, FX analyst, Convera

"The Fed and markets appear to be moving out of sync on the trajectory for interest rates, with the former signaling a high bar to cuts with the latter implying a lower bar to policy easing, a dollar-negative theme."

"Much uncertainty remains, however. Should America’s banking sector woes calm in a meaningful way and fade while U.S. inflation remains elevated, the Fed might have to put more dollar-positive rate hikes back on the table."