- GBP/USD facing trifecta of downside risks

- Could stymie recovery & open up new lows

- As Fed lifts USD & UK gov weighs on GBP

- Outlook for Bank Rate eyed in BoE decision

Image © Adobe Images.

The Pound to Dollar exchange rate recovered last week from losses that had pushed it into a test of major support levels on the charts although the rebound will face a trifecta of challenges over the coming days that could yet see Sterling retesting last week’s lows or beyond.

Sterling entered the new week attempting to swim while in deep water with a governmental ball and chain clasped around its ankles and could face additional downside risks this week from the Dollar and its response to a likely landmark Federal Reserve policy decision.

"Get boosted now to protect our NHS, our freedoms and our way of life," said Prime Minister Boris Johnson following Sunday’s announcement of an accelerated attempt to make a third vaccine shot available to all adults by year-end.

The new Omicron strain of the coronavirus was cited for the accelerated rollout of what are billed as booster vaccines, one which UK government dashboard figures suggest had already gotten off to almost as robust a start as the first highly successful campaign during early 2021.

Despite this the government’s supposedly irreversible roadmap to a reopened economy increasingly appears to have fallen by the wayside with Sunday’s remarks following on from last week’s move to ‘Plan B’ and subsequent suggestions that even a so-called 'Plan C' may soon be announced.

All of this leaves the UK economy and currency on the edge of a slippery slope just as the greenback stands to gain from Wednesday’s likely shift in policy at the Fed, which is widely expected to speed up the pace at which its quantitative easing programme is wound down in the months ahead.

"All in all, we see near-term weakness in the GBP toward 1.30 (on a hawkish Fed and a BoE hold next week, as well as political risks) but with gains resuming in the new year ahead of the BoE’s hiking cycle," warns Juan Manuel Herrera, a strategist at Scotiabank.

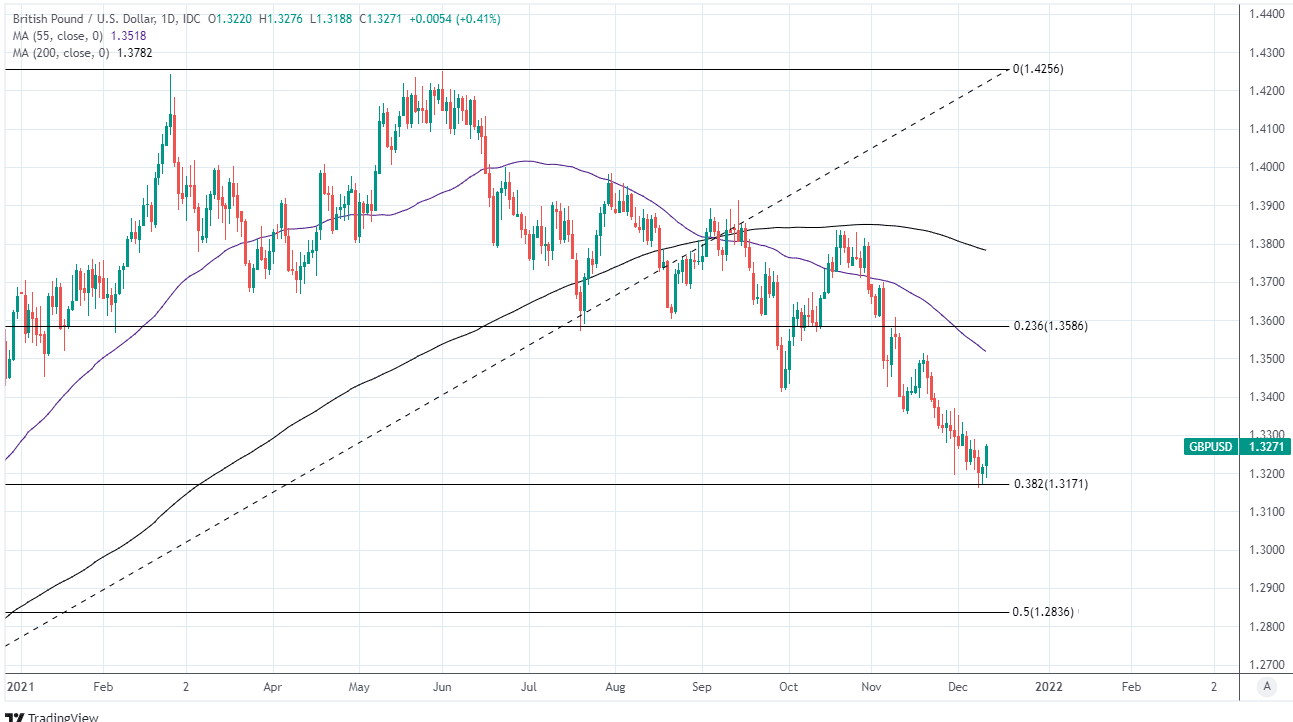

Above: Pound-Dollar rate shown at daily intervals, rebounding on Friday from a test of the 38.2% Fibonacci retracement of 2020’s recovery.

- GBP/USD reference rates at publication:

Spot: 1.3230 - High street bank rates (indicative band): 1.2866-1.2959

- Payment specialist rates (indicative band): 1.3110-1.3163

- Find out about specialist rates, here

- Set up an exchange rate alert, here

- Book your ideal rate, here

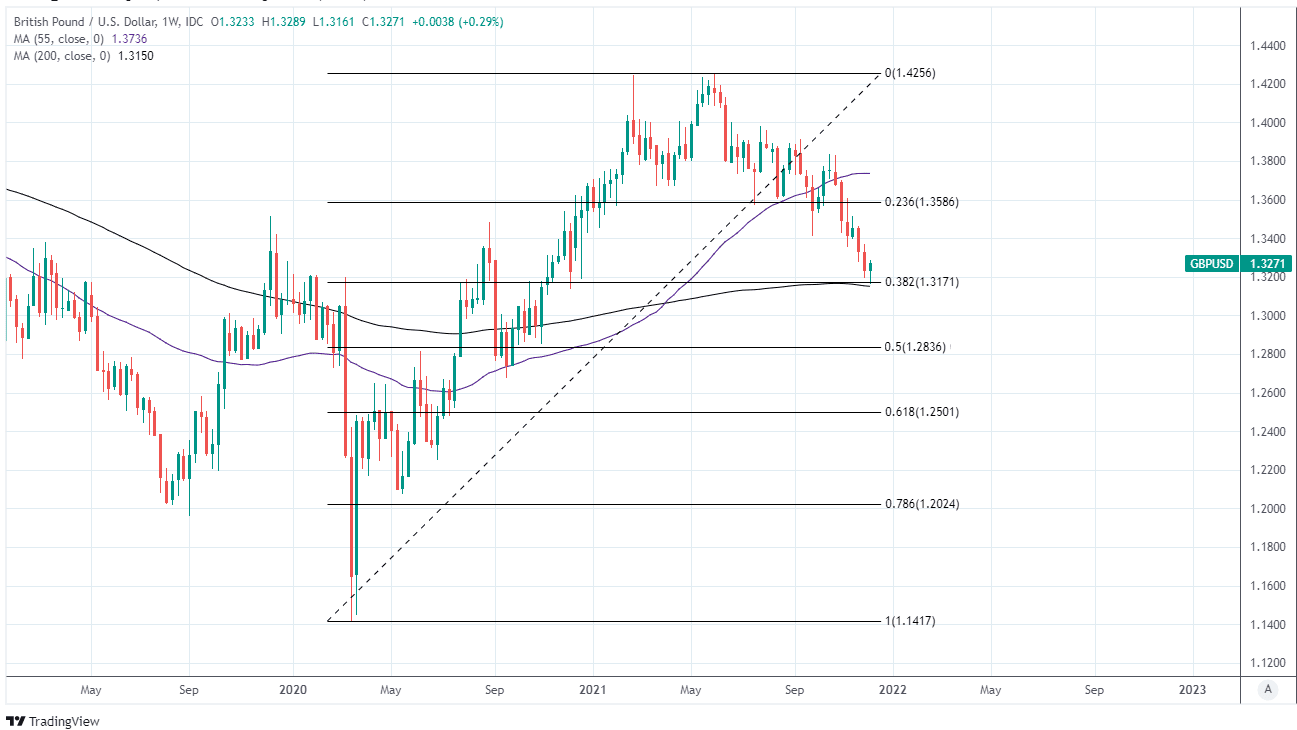

“Cable faces support at 1.3160/70 and its 200-week MA at 1.3152 (the mid-figure zone broadly). The 1.33 area is firm resistance where its 100-week MA of 1.3294 also stands,” Herrera and colleagues also said, writing in a Friday research note.

The Fed’s likely accelerated tapering of its bond buying programme creates room for its interest rate to be lifted sooner than was previously thought by the market and Wednesday’s updated economic forecasts will provide a loose guide to how much sooner the bank’s rate setters expect this will be.

No less than 10 voting members of the Federal Open Market Committee - which is a decisive majority - have indicated in recent weeks that they could support a decision to end the $120BN per month QE programme sooner than the June 2022 date that was envisaged and announced in November.

“The risk is an even faster taper of $US30/bn or more given high and widespread underlying inflation that pushes the USD higher. We also expect the median ‘dot plot’ will show the majority of members now expect two rate hikes in 2022. In September, roughly half of the FOMC members expected one 2022 hike,” says Kim Mundy, a senior currency strategist at Commonwealth Bank of Australia.

“GBP/USD will remain under modest downside pressure because the Bank of England (BoE) may take longer to turn hawkish. The money market has slashed the probability of a 15bps increase in the BoE’s policy rate hike on Thursday because of the potential for a negative growth shock from Omicron. Our base case remains for the BoE to begin a tightening cycle in February 2022,” Mundy and colleagues said on Sunday.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The Fed decision is out on Wednesday evening at 19:00 and comes ahead of Thursday’s update from the Bank of England, which is the highlight of the week in the UK calendar and will also be an important influence on the outlook for the Pound-Dollar rate heading into the new year.

BoE policymakers are widely expected to leave Bank Rate at 0.10% following a weeks-long market rethink of the outlook for UK interest rates that has seen investors shift to favouring February 2022 as the most likely timing of an anticipated decision to begin reversing last year’s interest rate cuts.

The catalyst for this was the late November discovery of the latest coronavirus strain, which even the most hawkish member of the BoE’s Monetary Policy Committee - Michael Saunders - has cited as a reason for the bank to be more cautious about withdrawing monetary support for the economy.

“Despite two members of the committee having voted to raise Bank Rate by 15bp in November (M Saunders and D Ramsden), at next week's meeting, we expect a 9-0 vote to maintain Bank Rate at 0.1% given the uncertainty with the public health situation,” says Fabrice Montagne, chief UK economist at Barclays.

“However, we believe that hawkish members will make their voices heard in the minutes, possibly with a conditional argument stating that should it quickly become clear that the Omicron variant is unlikely to be a significant threat to public health, the Bank may need to adopt a steeper hiking path than it otherwise would have done,” Montagne and colleagues wrote in a Friday research note.

Above: Pound-Dollar rate at weekly intervals with 200-week average and support from 38.2% Fibonacci retracement of 2020 recovery under pressure.

With the prospect of a rate rise to 0.25% having been written off already by the market there’s a chance that Sterling could go relatively unaffected by any decision on Thursday to leave the benchmark unchanged at 0.10%, although much still depends on what the BoE says about the outlook.

“Uncertainty about the near-term outlook is elevated enough to suggest that the MPC likely will vote unanimously to keep Bank Rate at 0.10% next week, even though employment and CPI inflation outturns have topped its expectations since its last meeting,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

“We now expect the Committee to wait until March to begin to raise Bank Rate, given that the economic situation likely will not be any brighter by the time of its next meeting at the beginning of February,” Tombs and colleagues said on Friday.

The BoE has said repeatedly in recent months that it would need to begin withdrawing the interest rate cuts that were announced at the onset of the pandemic if inflation is to return to the 2% target in an acceptable time frame, although the bank wanted confirmation that unemployment had not been lifted by the end of the UK government’s furlough scheme in September.

The latter point could potentially be confirmed when October’s labour market data is released this Tuesday while Wednesday’s inflation number could potentially reveal an ongoing acceleration of price pressures that would vindicate the BoE’s thinking about lifting interest rates, although it’s the bank’s Thursday commentary on the outlook for Bank Rate that is likely to matter most for Sterling over the coming weeks and months.

The BoE took issue in November with the market’s then-expectation for Bank Rate to rise as far as 1.25% next year and by Friday the expected rate for December 2022 had fallen to 0.89% although Sterling may be particularly sensitive to whether that message is repeated on Thursday as it would suggest that expectations have further to fall in the weeks and months ahead.