- GBP/USD steadier after rally off new 2021 lows

- Aided by UK growth upgrade & BoE policy shift

- Downside risks linger in big week for Fed policy

- Support seen at 1.3500 ahead of low 1.34 area

Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3552

- Bank transfers (indicative guide): 1.3178-1.3273

- Money transfer specialist rates (indicative): 1.3430-1.3484

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Pound-Dollar rate has recovered sharply from new 2021 lows but prior declines were technically significant and have gotten analysts warning that further losses could be seen in what promises to be a defining week for the Federal Reserve monetary policy outlook.

Sterling fell heavily and to a new 2021 low of 1.3411 against the greenback in the early stage of last week when disruptions to the UK fuel supply and large increases for natural gas prices on international markets had many observers suggesting the UK could be heading for a period of economic ‘stagflation.’

“GBP tends to underperform in this type of scenario for a variety of reasons, but they are rarely persistent and there are fundamental reasons to be skeptical about the odds of a prolonged stagflation,” writes Michael Cahill, a G10 FX strategist at Goldman Sachs, in a Friday research note.

Losses came alongside a widespread rally by the Dollar and heavy declines in international stock markets but around half of the Pound's fall was reversed in a Thursday and Friday recovery that enabled the Pound-Dollar rate to open the new week back up near 1.3550.

“The mid-figure zone [1.3550] will test whether the pound can counteract the strong downward pressure that emerged early last month, but firm resistance stands at 1.36,” says Juan Manuel Herrera, a strategist at Scotiabank, in a Friday note.

“Support is the 1.35 zone followed by the intraday low of 1.3434 and then 1.3400/15,” Herrera adds.

Recovery came after the Office for National Statistics’ announced a significant upward revision to its estimate of second quarter growth on Thursday, bolstering money market wagers that the Bank of England (BoE) could begin gradually reversing last year’s interest rate cuts over the coming months.

There’s scope for that rebound to continue this week if the BoE policy outlook draws a further bid for Sterling or if market appetite for the Dollar ebbs any further in advance of Friday’s non-farm payrolls report for September, with its implications for the Fed policy outlook.

Above: Pound-Dollar rate shown at hourly intervals alongside Euro-Dollar rate.

However, the Dollar’s gains and last month’s changes in the Federal Reserve policy outlook were significant developments and have together gotten many analysts warning that there’s now a risk of further declines for the Pound-Dollar rate over the coming week.

“For the shorter term, we tend to favour the dollar (GBP does not like risk aversion) and technically there is a case for a multi-day move in Cable to 1.32. Resistance at 1.3570/2620 should now be a tough nut to crack on the upside,” says Francesco Pesole, a strategist at ING, in a note on Friday.

Tuesday’s speech from BoE Deputy Governor David Ramsden is the main event in a sparsely populated UK calendar this week, while the Dollar has Tuesday’s Institute for Supply Management Services PMI survey results to navigate before market attention shifts to Friday’s job data.

“The market may need to consolidate its recent losses near term,” says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank.

“GBP/USD has recently eroded the 1.3515/04 January 2009 low and 2019 peak and this represents a big break down point for the market. The close below here introduces scope to the 200-week ma at 1.3160,” Jones wrote in a research briefing on Friday.

Friday’s payrolls are more import than usual because September’s economic forecasts and policy remarks from Fed officials have made clear that a 'strong' number would be enough to announce plans to begin winding down its $120BN per month quantitative easing (QE) programme at the November 03 meeting.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“We estimate that overall payrolls advanced by 400,000 (private 350,000) in September,” says Kevin Cummins, chief U.S. economist at Natwest Markets. ”Anything close to that result would probably be considered “decent” enough by Chair Powell.”

Chairman Jerome Powell himself said in September’s press conference that “it wouldn’t take a knockout, great, super strong employment report. It would take a reasonably good employment report” for him to become willing to join the “many” on the Federal Open Market Committee who already view it as appropriate to begin weaning the economy and financial markets off of the Fed's yield and interest rate suppressing support.

"The outcome of the September FOMC was hawkish. Barring unforeseen material labor market weakness, our baseline view is that the Federal Reserve will announce and implement tapering in November," says Athanasios Vamvakidis, head of FX strategy at BofA Global Research.

Friday’s data is all the more important because if the Fed begins winding down its QE programme in November it would be likely to have the process completed by the middle of next year, and one implication of this is the bank might then feel less inhibited about lifting its interest rate from near zero.

Recent U.S. job growth has been strong however, with more than two million jobs created or recovered from the coronavirus during the three months to the end of August; and this might mean that a soft or outright poor number is a bit more likely for September than it would be for any other month.

"The market has yet to digest the reality of Fed policy normalization over the upcoming hiking cycle, with rate forwards currently residing some 2-3 hikes below the Fed's 2024 dot. Relative monetary policy risks favor the US dollar,” Vamvakidis and colleagues warned in a note last week.

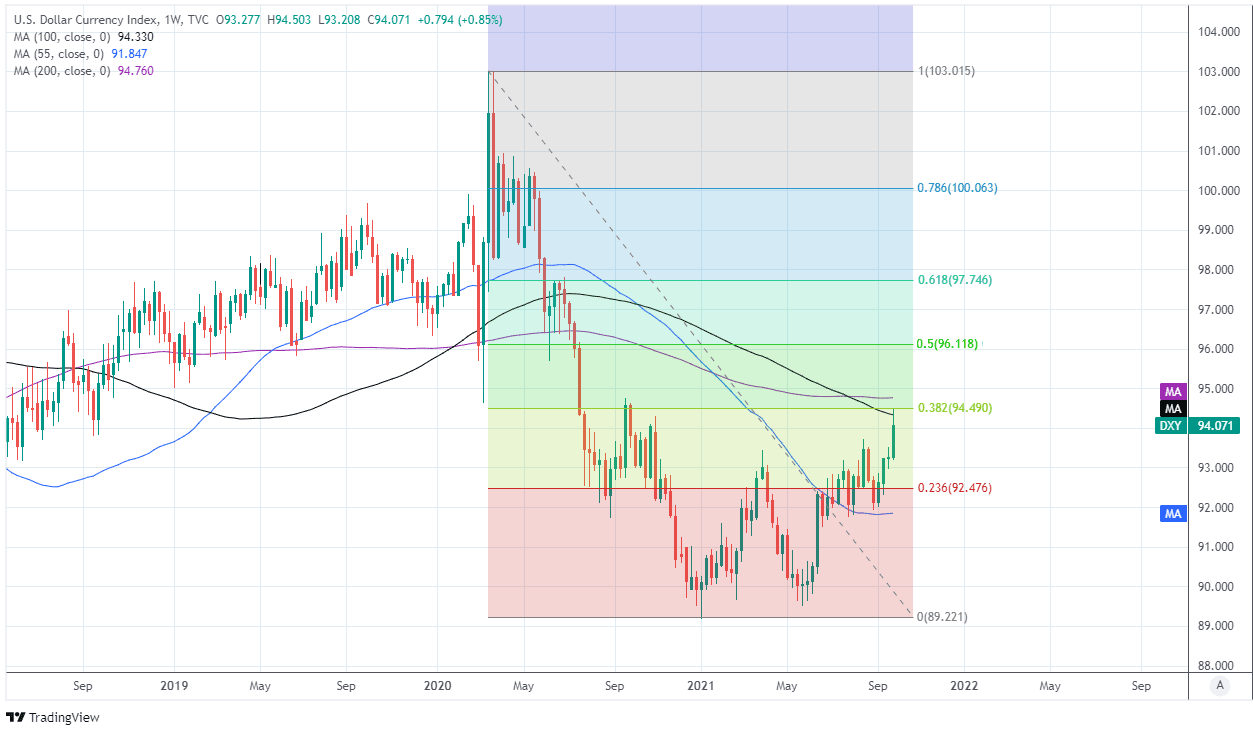

Above: U.S. Dollar Index shown at weekly intervals. Meet resistance from 38.2% Fibonacci retracement of 2020’s fall and its 100-week moving-average.