- USD no longer just a yield story

- Safe haven bids are back

- Delta variant is a key driver of investor anxiety

- Falling oil prices benefit USD

Image © Adobe Stock

- GBP/USD reference rates at publication:

- Spot: 1.3802

- Bank transfers (indicative guide): 1.3420-1.3517

- Money transfer specialist rates (indicative): 1.3679-1.3706

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Dollar is finding support amidst renewed investor anxieties over medium-term global growth according to new research, suggesting those watching this currency will have more than just the U.S. Federal Reserve and inflation expectations to consider.

The U.S. Federal Reserve's 'hawkish' shift at their June policy meeting is said by Credit Suisse to be a driver of mid-year U.S. Dollar outperformance, but so too is the rise of the Delta variant of Covid-19.

Foreign exchange researchers at Credit Suisse say the Dollar is now likely benefiting from investor demand for 'safe-haven' assets as developments in U.S. bond markets have hardly been constructive of late.

"A number of more broadly risk-negative factors might allow to interpret USD strength in 'safe haven' terms, pointing to simmering investor concerns about a less constructive medium-term growth outlook," says Shahab Jalinoos, Global Head of FX Strategy at Credit Suisse.

The shift in interest rate expectations in the U.S. - the Fed now sees interest rates as likely in 2023 as opposed to 2024 - is widely cited by analysts as being behind increased demand for the Dollar, reflected upon widely in this publication.

The understanding is that expectations for higher rates in the U.S. delivers higher yields on bonds which in turn attracts overseas investor interest, thereby supporting the Dollar.

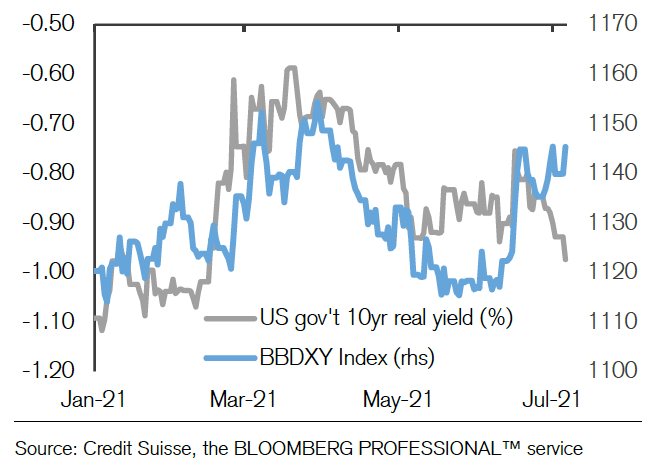

But data shows U.S. yields have come down since the Fed meeting, which is hardly supportive of the Dollar appreciation story:

Above: USD and US real yields moved in opposite directions in recent weeks. Image courtesy of Credit Suisse.

Credit Suisse observes the shift in interest rate differentials in favour of the USD has not extended further.

"Viewed in this context, the USD’s resilience appears less at odds with the traditionally USD-negative price action associated with declining nominal US yields," says Jalinoos.

The Pound-to-Dollar exchange rate (GBP/USD) has been in decline since peaking at 1.42 back in early June and is quoted at 1.3797.

The Euro-Dollar rate is meanwhile witnessing a similar pattern of short-term depreciation consistent with a strengthening Dollar and is at 1.1817.

Observing U.S. Dollar resilience, in the absence of yields support, Jalinoos says "something different might be afoot".

{wbamp-hide start}

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

The analyst says simmering investor concerns about a less constructive medium-term growth outlook are emerging.

One area of concern involves the spread of the Delta variant of Covid-19, a more transmissible variant that means the threshold for herd immunity is potentially higher than current vaccination targets would achieve.

"Herd immunity via vaccinations will not be possible for many countries including the UK, given the vaccine portfolio and high transmissibility of the delta variant," says Shreyas Gopal, Strategist at Deutsche Bank.

This is exemplified by Israel where cases are rising despite 65% of the entire population receiving a vaccination.

The UK is seeing a third wave of infections despite having now given at least one dose to 66% of the population.

"In reality we are all due to suffer a fourth wave of Coronavirus infections, the difference is that much of the UK and US population will experience relatively mild symptoms," says John Meyer, head of research at brokerage SP Angel. "Sadly, unvaccinated populations will, in all probability, continue to suffer higher levels of critical sickness and mortality."

The UK is seeing an exponential growth in cases that saw Prime Minister Boris Johnson warn 50K new daily positive cases could be reported in coming weeks, a figure put as high as 100K by Health Secretary Sajid Javid.

If such an outbreak can occur in a highly vaccinated population such as that of the UK, it can almost certainly prove more serious in populations with lower rates of vaccine penetration.

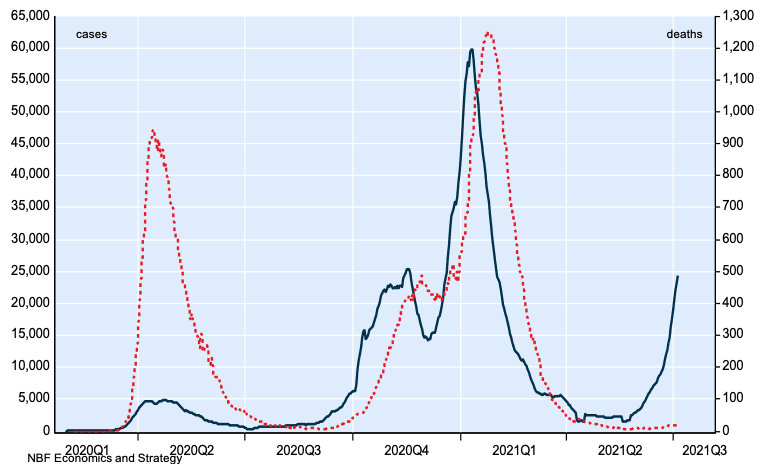

Above: UK Covid cases (black) vs. deaths (red). Image courtesy of NBF Economics.

"While the still low level of hospital admissions argue against a major downgrade in growth expectations, markets might view this development as supporting the idea that some Covid restrictions might persist for longer even amid very high rates of inoculation, in countries that have shown an asymmetrically higher tolerance for lockdowns," says Jalinoos.

Credit Suisse identify softer Chinese data, linked to the Delta variant, as a potential additional contributor to investor worries.

They note Chinese June non-manufacturing Caixin PMI data released on 5 July showed a sharp decline in growth in the services sector, largely attributed to a Delta variant Covid-19 outbreak in the Guangdong region.

A fall in oil prices over the past 24 hours is also identified by Credit Suisse as a negative factor for commodity-linked currencies; one only has to look at the performance of the Canadian Dollar.

The OPEC squabbles over production levels are identified as the primary driver of recent rises and subsequent falls in the value of crude; should further weakness ensue the Dollar would inevitably be a beneficiary.

"While the initial USD rebound from the mid-June lows can be easily ascribed to the hawkish turn in US monetary policy expectations, more recent price action seems to be the product of a wider range of factors," says Jalinoos.

So what does this pose for the U.S. Dollar outlook?

Credit Suisse envisage a "dispersed outlook" for the Dollar and anticipate the currency will likely trade stronger in a range against low yielders such as the EUR and JPY, but more idiosyncratically and less on a trending basis against other currencies.