- USD outperforms major rivals after Fed shift

- Tops board among majors this week, in June

- U.S. Dollar index takes out multiple key levels

Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3997

- Bank transfers (indicative guide): 1.3607-1.3705

- Money transfer specialist rates (indicative): 1.3870-1.3899

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The U.S. Dollar outperformed all major currencies except the Japanese Yen Friday after a possibly landmark shift in monetary policy guidance from the Federal Reserve (Fed), which has helped the ICE Dollar Index overcome a series of key levels and gotten analysts contemplating forecasts anew.

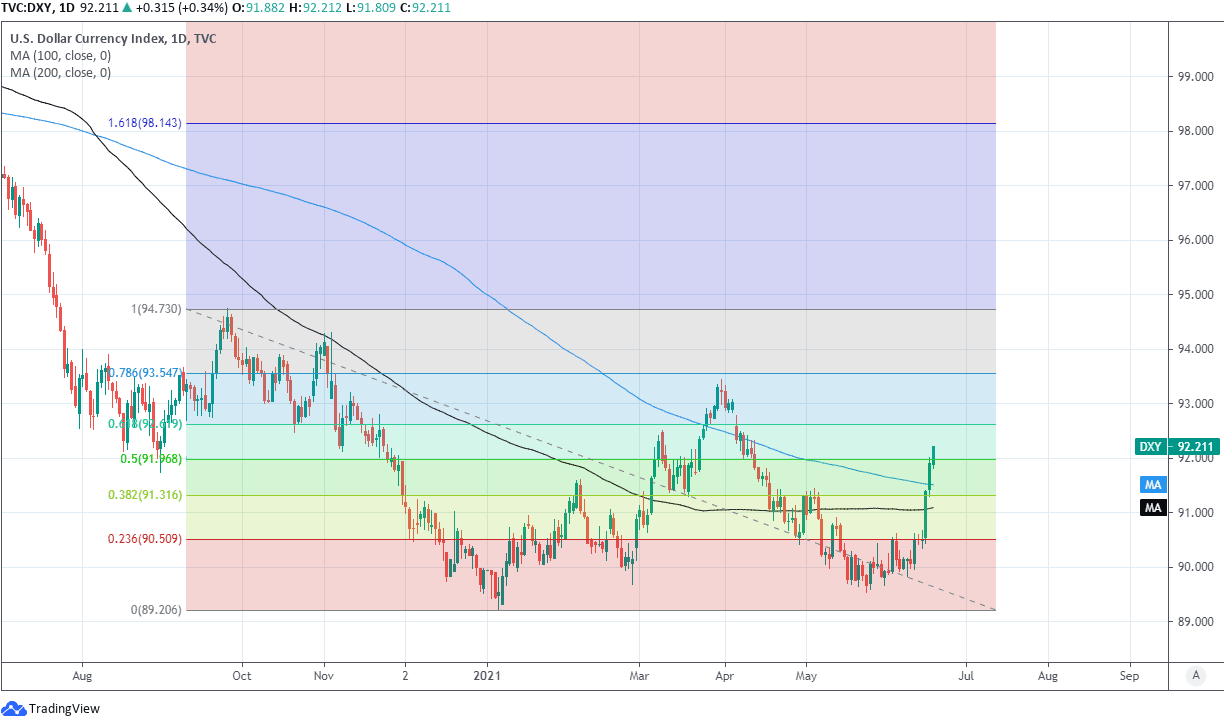

Dollars were bought heavily and against almost all counterparts this week, leading the greenback to the top of the performance rankings among so-called G10 currencies while enabling the ICE Dollar Index to rise above both 100 and 200-day moving-averages, while also taking out a hat-trick of Fibonacci retracement levels.

It cannot be said for certain at such an early stage, but it’s certainly possible the bounce is being driven by a two-pronged tailwind including new money which has been lured by tentative signs of a policy shift at the Federal Reserve as well as capitulation by punters who’d been wagering against the Dollar.

The resulting Dollar gains were as steep as they were broad, leading the ICE measure of the U.S. currency against its most frequently traded counterparts to rise by 2.3% for the week to Friday along, which had the effect of lifting the benchmark to a 2021 gain of 2.48%.

Above: U.S. Dollar Index shown at daily intervals with key averages and Fibonacci retracements of September 2020 move lower.

Previously, by mid-June, the Dollar Index had been sitting largely unchanged for 2021 after a fortnight spent creeping back from low single-digit losses for the year.

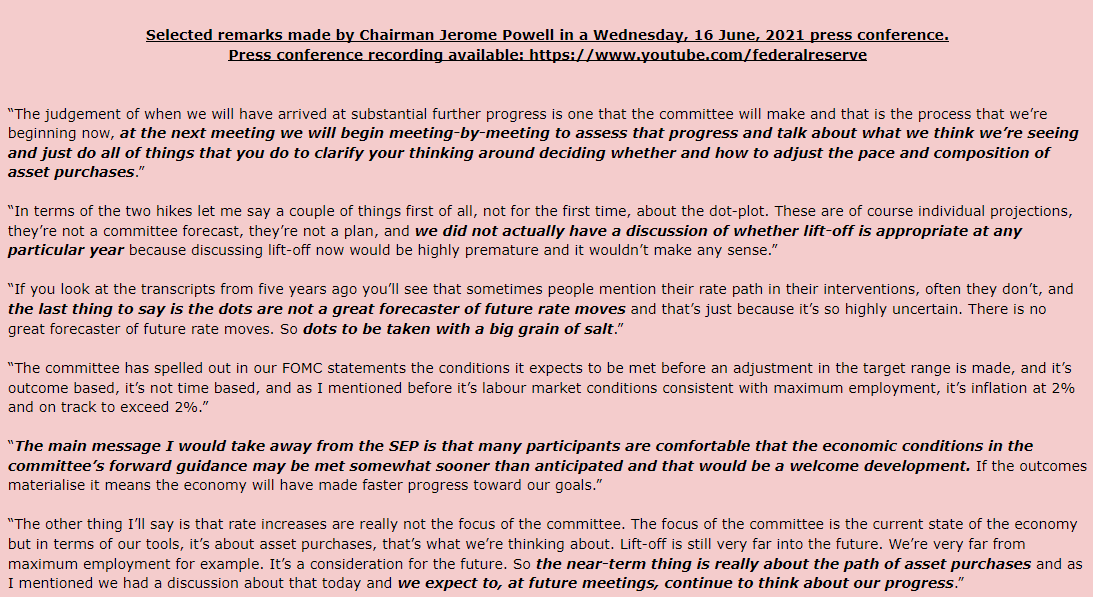

This comes after the Federal Open Market Committee of the Fed indicated on Wednesday, using its so-called dot-plot of policymaker expectations for the Federal Funds interest rate range, that rate setters now see current economic conditions as warranting an initial interest rate rise in 2023 rather than 2024.

That has gotten markets moving and analysts mulling forecasts or otherwise contemplating what the latest Fed guidance could mean for various markets going forward, while there’s plenty of fodder for debate out there.

For instance, Friday’s gains in gold and silver prices - which normally tend to move in the opposing direction to the Dollar - could indicate limited investor confidence in the rebound, while USD/JPY price action throughout this week is a potential indication of the overall Dollar move’s limited scope.

Above: Transcribed remarks made by Chairman Powell in June 16's press conference, a recording of which is available here.

What the Analysts Say

Neil Wilson, chief market analyst, Markets.com

“10yr yields have slipped back under 1.48%. Stocks have come off their record highs since the Wednesday meeting, but yesterday the Nasdaq Composite – composed of tech and growth companies that ought to do less well in a rising rate environment - gained 0.87%.”

“Dollar strength continues to dominate the FX narrative in the wake of the Fed. GBPUSD is lower again with a break of the 100-day moving average to 1.3860. The washing out of longs maybe has some way to go yet and a test of the April double bottom at 1.3660 may be on if there is further for this to correct. Fairly stretched GBP longs and shorts on the USD mean this could have further to unwind.”

Derek Halpenny, head of research & global markets EMEA, MUFG

"Our current end-Q1 2022 forecast for EUR/USD is 1.2400 so we would make the point that prior to Wednesday’s FOMC we were not uber-USD bears. We do also have an end-2021 forecast of 1.2600 however, and that now seems too high and some adjustment to our levels is required."

"From a technical and momentum perspective there is certainly further scope in the near-term for the dollar to advance. The DXY trendline resistance from the highs in March this year and March last year was broken yesterday at 91.430 providing the catalyst for the gains yesterday after the 1.0% advance on Wednesday."

Steen Jakobsen, chief investment officer, Saxo Bank

“The USD is very strong here as the market reprices Fed expectations after the Wednesday FOMC meeting this week. Together with the strong JPY it is the primary focus in FX right here, as EURUSD has become fully unglued and closed yesterday below a key retracement level that suggests a possible run to the interesting 1.1750 area, a kind of “head-and-shoulders" neckline.”

“AUDUSD has broken below major support around 0.7550, etc. The move looks incredibly sharp and may be overdone in the very short-term, but it would take a huge countermove now to shift expectations of more USD strength.”

“Having sliced through several key support levels, gold is currently looking for support at $1769, a level that represents a 61.8% correction of the April to June rally. The road back to relative safety is currently quite long with focus on $1825 followed by $1,838, the 200-day moving average.”

“Silver meanwhile has bounced ahead of key support in the $25.68-73 area.”

{wbamp-hide start}

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

Athanasios Vamvakidis & Claudio Piron, strategists, BofA Global Research

“We see rising risks of sustained US inflation. As FX is mostly driven by central banks this year, the Fed reaction matters. Fed dovishness has been keeping the USD down, but normalization to address inflation risks will support the USD.”

“June has not been kind to GBP as the next phase of easing is delayed. But data continues to print strongly. Longer-term GBP anchors have not deteriorated, suggesting current decline is merely position/hedging related.”

“EUR/GBP has been a favored GBP long, but the cross has found a base as EZ vaccine accelerates.”

Nema Ramkhelawan-Bhana, head of research, Rand Merchant Bank

“Regional FX is weaker with only the CNH and JPY managing to sustain gains. Asia’s FX performance has dragged on the broader EM complex, although weakness is far more measured than yesterday.”

“The Brazilian real is the only EM currency to have recorded positive results over the last five days relative to the Columbian peso which shed the most value among its developing markets peers. Spot rand struggled to hold its own this week, although it remains up on a year-to-date basis.”

“Having tested 14.16 against the greenback, the local unit has pulled back to 14.07.”

Praveen Korapaty, global macro and markets economist, Goldman Sachs

“Going forward, interest rates could display greater sensitivity to labor market and inflation data (in that order).”

“As noted, the future inflation bar for liftoff would be lower, and markets could plausibly impute that a rapid improvement in the labor market may more clearly translate into an earlier liftoff.”

Mikael Olai Milhøj, chief analyst, Danske Bank

“The meeting most likely marked the first step of the Fed taking the foot off the gas. The Fed is now signalling two rate hikes by end-2023 and that the FOMC members will continue discussing tapering at upcoming meetings.”

“US Treasury yields rose significantly (especially 5yr) and EUR/USD has declined from above 1.21 to below 1.20.”

Joshua Mahony, senior market analyst, IG Group

“The weak pound has done little to lift the FTSE, with markets continuing to feel the residual effects of Wednesday’s FOMC meeting.”

“The pound has been hit hard in the wake of Wednesday’s FOMC meeting, but a bout of disappointing retail sales figures has further increased the pressure on sterling this morning. Nonetheless, the decline in May retail sales is perhaps more indicative of a shift in spending habits rather than decline, with consumers opting to cut back on food purchases (-5.7%) in favour of eating out.”