- GBP/USD recovery in prospect as global market stabilise.

- U.S. vaccination speed, spending bolster appeal of USD.

- But others' depreciation demands argue for selective bid.

- GBP/USD supported at 1.3672 on weakness, eyes 1.40.

Image © Adobe Images

- GBP/USD spot rate at time of writing: 1.3791

- Bank transfer rate (indicative guide): 1.3408-1.3505

- FX specialist providers (indicative guide): 1.3584-1.3694

- More information on FX specialist rates here

- Set an exchange rate alert, here

The Pound-to-Dollar exchange rate was recovering off two-month lows ahead of the weekend but could be likely to extend this move further over the coming days as international markets stabilise and the U.S. Dollar becomes more selective in its appreciation.

Sterling was on the rebound Friday amid an evident improvement in investor sentiment although it lagged higher-yielding commodity currencies like the Australian, Canadian and New Zealand Dollars, which also recovered following a bout of widespread weakness for risk assets and currencies.

Meanwhile, U.S. Dollars were sold more selectively and commodities as well as other risk assets were bought on Friday following a volatile period that saw investors responding to both a deterioration of the short-term economic outlook in Europe as well as improved prospects for the U.S. economy.

The Pound-to-Dollar exchange rate was a fraction higher on Friday but lower for the week, while Sterling gained on low-yielders like the Euro for both periods in a pattern of price action that could be likely to endure through the coming days.

"GBP was undermined at the start of this week by the deterioration in risk sentiment which hit other high beta G10 currencies," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG. "The recent correction lower for the GBP though does not reflect a material deterioration in positive fundamental drivers that have helped it to outperform so far this year alongside the CAD and USD."

Disruption to vaccine exports from India was widely cited for Sterling's losses, which came alongside steep falls in EUR/USD and new or prolonged 'lockdown' for several major European economies including Germany.

This and the brightening outlook in the U.S. has gotten a once-bearish market rooting for the Dollar to outperform further and helped drag GBP/USD below 1.40, although it found strong support coming from a Fibonacci retracement around 1.3672 which may limit any further losses this week.

"Sizable fiscal stimulus, the likelihood that the drag from COVID will fade significantly, and a massive pile of “excess” savings available to support consumption makes us extremely optimistic about growth in 2021 and 2022," says Kevin Cummins, chief U.S. economist at Natwest Markets. "The upcoming week’s economic calendar features the regular start-of-the-month package of the manufacturing ISM and the employment report, along with auto sales and a handful of other indicators. We expect data to have a generally strong tone, due in part to the fading impacts of harsh weather."

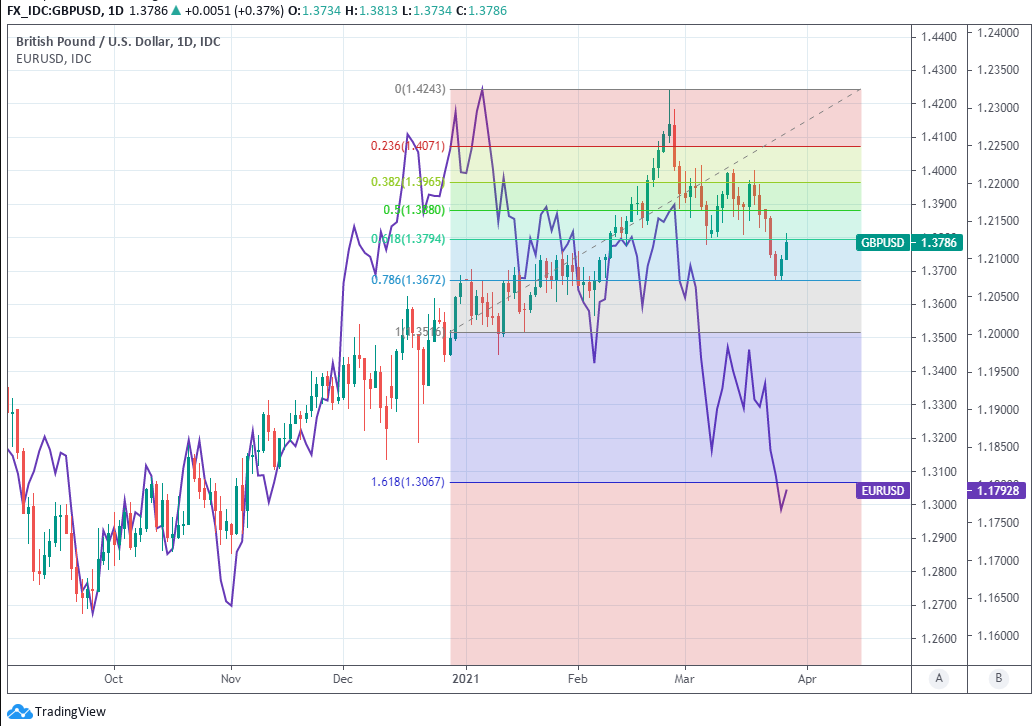

Above: Pound-to-Dollar rate at daily intervals with Fibonacci retracements of January 15 rally and EUR/USD (purple).

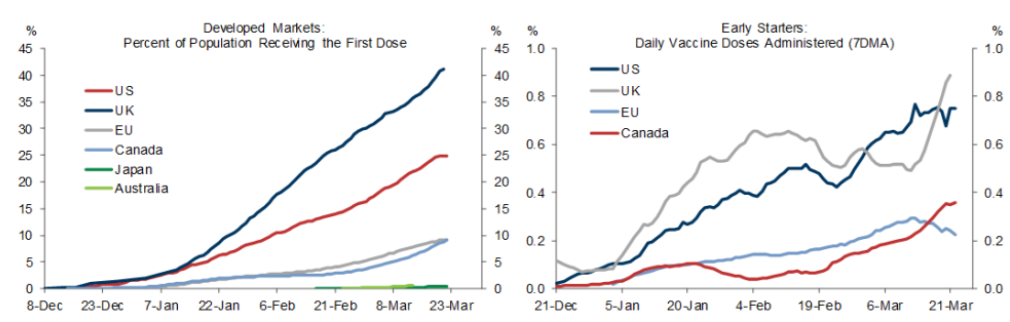

Washington's ramped-up vaccination programme has seen the U.S. begin to rival the UK in terms of the percentage of population receiving a shot each day and although the ink is barely dry on legislation authorising President Joe Biden's $1.9 trillion fiscal support package, the White House is already reported to be drafting an even larger infrastructure-focused bill. This could bolster investor and economists' expectations for U.S. growth, which have already risen notably of late and lifted the Dollar.

"With greater clarity on the Fed’s reaction function, the main risk to our bearish Dollar outlook now relates to non-US growth. Significant downside surprises to either Euro Area or Chinese growth could warrant upward revisions to our forecasts for USD crosses. At the same time, increased confidence in our upbeat European growth forecasts (e.g., due to accelerating vaccine distribution) would be reason to lean in to Dollar shorts," says Zach Pandl, global co-head of FX strategy at Goldman Sachs.

Rising U.S. growth expectations have had investors wagering the Federal Reserve (Fed) will be compelled to lift its interest rate sooner than the 2023 time its most recent forecasts have implied, and helped lift U.S. bond yields as well as the Dollar but the Fed itself still insists that rates are likely to remain at current levels at least for as long as that, while the Goldman Sachs research team said last week that investors have already taken the pricing-in of a more 'hawkish' outcome almost as far as is possible.

"The pure relative vaccine-bet (being short EUR vs. Anglo-Saxon peers) has been a tremendous 2021 bet, and due to the third wave in countries like Germany, Italy, France and partly Spain, the virus spread is now WORSE in continental Europe compared to the UK and US for the first time during the pandemic," says Martin Enlund, chief FX strategist at Nordea Markets. "The vast amount of year-end USD selling (due to unwinds of USD asset positions) by Japanese accounts is likely already behind, and USD/JPY usually bottoms around 23rd or 24th of March as fast-money accounts try to front-run the flow-picture. USD/JPY has more upside potential."

Source: Goldman Sachs Global Investment Research.

Europe's vaccine procurement troubles have also been a boon for the Dollar having pulled the rug from under the Euro, Swiss Franc and others. But these moves combined with 2021's declines in the Japanese Yen and Chinese Yuan mean the Dollar has now risen strongly against most large U.S. trade partners' currencies, which is in some ways an argument for an offsetting recovery in the likes of GBP/USD, CAD/USD and MXN/USD, which are the other large components of the trade-weighted Dollar.

"Ending the week, there are very few signs yet that what we see as a corrective dollar bounce has run its course. On the agenda next week are a few inputs which on paper look dollar positive. The first is the US macro data where the March employment numbers (ADP on Wednesday and NFP on Friday) should be strong," says Chris Turner, global head of markets and regional head of research at ING. "Markets continue to see the UK Government’s timeline to re-open the economy as realistic and therefore sterling is retaining some better resilience than other G10 currencies to USD appreciation. We can expect that same resilience to last next week."

The trade-weighted Dollar rally, which is as much a function of necessary depreciation elsewhere as it is investors' interest in the greenback, could encourage the Dollar's appreciation to become more selective in the weeks ahead and this would likely be supportive of Sterling. The UK's vaccine rollout has put the economy on course for one of the fastest recoveries in the developed world this year, enabling British bond yields to rise alongside those of the U.S. This means among other things that if there are any major currencies at all which are likely to rise against the Dollar in the current market, the Pound is eligible to be one of them.

"We see initial resistance now at 1.3790 and think that Cable regaining a 1.38 handle should provide the basis for some technical stabilization in this market, if not a more significant recovery. We rather favour a rebound developing from the low 1.37s; the sharp move lower leaves the GBP looking oversold and prone to snap higher (potentially towards 1.40) over the next week or so," says Juan Manuel Herrera, a strategist at Scotiabank.

Above: Pound-to-Dollar rate at weekly intervals with 10-year U.S. (black) bond yield and 10-yar UK yield (yellow).