- GBP in outperformance mode but may see near-term weakness.

- As Chinese Q4 and 2020 GDP sets scene at open of new week.

- Ahead of Presidential inauguration, address & central bank risks.

- GBP risks softness short-term, but break of 1.37 a matter of time.

File Image © Adobe Images. Webpage Image © Federal Reserve Bank of New York, entrance at 33 Liberty Street.

- GBP/USD spot rate at time of writing: 1.3580

- Bank transfer rate (indicative guide): 1.3208-1.3303

- FX specialist providers (indicative guide): 1.3379-1.3488

- More information on FX specialist rates here

The Pound-to-Dollar exchange rate sustained its worst decline for months on Friday as risk-aversion lifted the U.S. currency against many rivals, although as global markets stabilise in the coming days, a quicker pace of vaccination and an improving economic outlook could see Sterling retest recent highs at 1.37.

Sterling ended the week with its worst loss to the Dollar since September and its first decline for seven trading days against the Euro, with losses coming amid risk-aversion in global markets and after a UK government decision to close international borders in response to new coronavirus strains.

However, the British currency was otherwise the outperformer of the week having risen against all major rivals, although a resurgent Dollar was in close pursuit as stocks and other risk assets handed back more than half the gains notched up in the opening days of the New Year.

"Positioning analysis shows GBP resilience for the coming week, as both continuation and reversal signals point to upside risks. GBP uptrends against USD and JPY, the so-called" safe-haven"currencies, remain intact," says Vadim Iaralov, a quantitative strategist at BofA Global Research. "On the other hand, and amid a broad-based correction for the so-called"high-beta"currencies, GBP/G10 downtrends are all at medium or high risks of reversal."

Despite its resilience so far, Pound Sterling could be susceptible to further softness at the opening of the new week if China's final quarter GDP numbers are received poorly by the market given that the Pound has among the highest beta sensitivities of the major currencies to the Chinese Yuan.

Above: Sterling Vs the majors over selected timeframes. Source: Netdania Markets. Click for closer inspection.

Equally but on the opposite side of the same coin, better-than-expected figures could pick the Pound up off the floor and enable it to continue outperforming. This could be particularly likely given that a rising GBP/USD rate and the resulting uplift it would give to GBP/EUR is becoming increasingly important for keeping the EUR/USD rally going

"We suspect the dollar bear trend needs some consolidation," says Chris Turner, global head of markets and regional head of research at ING, who's colleagues say GBP/USD should find support at 1.3420 on weakness over the coming days and that it could have scope to reach 1.38 later this week. "The USD/Asia drop has slowed (helped partially by a weaker CNY fixing) and also by emerging complaints around the world over the pace of the dollar decline. Given flows into emerging markets have been a key driver of this benign dollar decline, China 4Q GDP (released early Monday) will also set the tone."

{wbamp-hide start}

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

Consensus favours a 6.2% annualised rebound for the final quarter Chinese GDP when the data is released at 02:00 London time on Monday morning, an event that will set the tone for not only Sterling, but for the U.S. Dollar, other currencies and the broader global markets too. Asian currencies including the Yen, Yuan and Indian Rupee have been strong relative performers this year and so too have stock markets including the Nikkei 225 and India's NIFTY 50 so all may be sensitive to China's numbers.

"Our research suggests that US fiscal easing and/or bear steepening in the Treasury curve should not turn the bearish Dollar trend. However, greater optimism about US growth has created a more two-way debate in FX markets about the outlook for the greenback this year," says Zach Pandl, global co-head of foreign exchange strategy at Goldman Sachs, who forecasts a Pound-Dollar rate of 1.42 by the end of March and 1.45 by year-end. "For now we remain comfortable with our optimistic global growth views and continue to expect broad Dollar weakness in 2021; we stay long CAD and AUD vs USD."

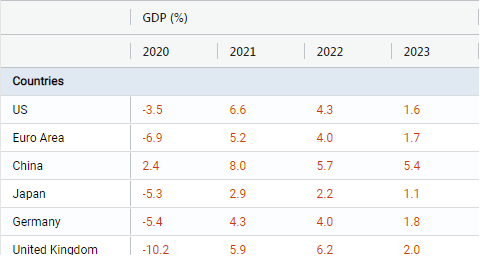

Above: Goldman Sachs Investment Research GDP forecasts for selected major economies.

Beyond the opening of the week, focus will likely shift quickly back to U.S. bond yields and Wednesday's inauguration of President Elect Joe Biden, who's anticipated speech will be listened to closely for clues on how soon the administration expects to make vaccinations widely available and how else it might support the U.S. economy. The inauguration comes after global markets fell broadly on Friday as investors worried about whether a proposed $1.9 trillion aid package will make it through Congress, which offset the impact of a speech from Federal Reserve Chairman Jerome Powell that had reigned in an earlier Dollar-supportive surge in bond yields during the overnight session.

"It is already clear that Biden’s key focus following inauguration will be tackling the pandemic. Elevated optimism on vaccine roll-outs will support risk assets and assuming the Fed keeps yields in check, should keep the US dollar weaker," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG. "The next 12-18mths are perhaps one of the most important periods in Federal Reserve history with no room for communication error given the consequences it would likely have on inflation expectations and the Fed achieving its goals. We assume the Fed does it job this year and hence the dollar weakens."

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The Dollar could also draw further support this week if the European Central Bank and Bank of Japan use Thursday policy announcements as an platform to attempt to persuade their currencies out of further advances on the Dollar, although this may be unlikely to effect Sterling by much. The Pound is insulated from U.S. yield and growth pressures after Bank of England (BoE) Governor Andrew Bailey suggested negative interest rates are now unlikely, leading British yields to also rise.

"GBP may struggle for now to cross above 1.37 with markets still anxious over the ongoing spread of the virus worldwide, but the UK’s aggressive vaccination plans should begin to lift sentiment in the currency," says Juan Manuel Herrera, a strategist at Scotiabank. "Still, technical signals are aligned for an eventual breach of the figure—that would point to a push to 1.40."

Above: GBP/USD at daily intervals with U.S. Dollar Index (orange) and EUR/USD (blue).

Another factor supporting Sterling is Britain leading ahead of the U.S. and other major economies in vaccinating its population against coronavirus.

"GBP looks increasingly like a notable “Covid goes away” play," says Shahab Jalinoos, head of FX strategy at Credit Suisse, who sees Sterling at 1.40 later this year if the UK continues leading on vaccinations. "If the UK is successful in muting the current Covid spike and meeting its aggressive vaccination targets, it could yet emerge among the quickest countries to reach herd immunity, perhaps as soon as by the summer. If so, the prospects for H2 2021 would look very strong, especially as house prices are already buoyant and could remain so with the right tax policy at the 3 Mar budget."

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

The Telegraph reported this weekend that all over-18's will have had an opportunity to be vaccinated by the end of June, barely more than a week after Prime Minister Boris Johnson said that 15 million people would be vaccinated by February 15. When combined with the three million who've already tested positive for the virus, the latter would see to it that more than a quarter of the population have been vaccinated or diagnosed before March.

"We are not convinced that we will see resumption of the up move just yet and note the 13 count on the 240 minute chart plus TD resistance at 1.3800. We still cannot rule out losses to the 1.3350 late December low, the 1.3189 December 21 low and also the 1.3210 7 month uptrend. Currently, the Elliott wave count is implying a slide to 1.3370/1.3275," says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank. "Only a rise above 1.3712 on a daily chart closing basis would push the 1.3836 February 2016 low to the fore. Longer term the 2018 peak at 1.4377 is being targeted."

Above: GBP/USD at daily intervals with Fibonacci retracements of October extension higher and EUR/USD (orange).

With vaccinations and all of the international data or other drivers aside, Bank of England Governor Andrew Bailey will address online audiences on Monday at 13:30 and on Thursday at 17:00 London time, with both being addresses that will likely garner attention given recent comments on negative interest rates.

Once through the BoE's speeches, financial markets and Pound Sterling traders may scrutinise Friday's retail sales report for December, which is due out from the Office for National Statistics at 07:00, and IHS Markit flash PMI surveys for the manufacturing and services sectors for January.

The latter are due out later at 09:30 and will be important given the national 'lockdown' announced at the beginning of the month while retail sales could come in for addtional scrutiny after GDP data suggested last week that the economy was more resilient to November's new restrictions that had closed down the hospitality sector than it was in the initial lockdown during early 2020.

"Data next week will give us a sense how much of a recovery we can expect in December as well as how much of a fall we should anticipate in January," says Sanjay Raja, an economist at Deutsche Bank. "One of the main highlights of next week will be the PMIs, which should give us an initial sense of the January drop. We're expecting falls in both manufacturing and services activities with the former slipping to 49.9 (on the back of an unwinding in stocks) and the latter down to 44.5 as a result of the third lockdown. Our models point to some (marginal) downside risks to consensus estimates."

Above: Pound-to-Dollar rate shown at weekly intervals alongside U.S. Dollar Index (orange).