Image © Adobe Images

- USD rises as retail sales surprise soothes economic concerns.

- Strong July sales put economy on the front foot in third-quarter.

- Provide an offset to pessimism coming from the bond market.

- ING says recession risks are being exaggerated by bond yields.

- Strong U.S. economic data makes steep rate cuts by Fed difficult.

The Dollar rose against its G10 rivals Thursday after retail sales figures surprised strongly on the upside for the month of July, boding well for growth in the third-quarter and suggesting consumers are yet to receive the recessionary memo sent by the bond market earlier this week.

Retail sales rose by a substantial 0.7% in July, according to Census Bureau data,, when the market consensus had been for only a 0.3% increase. Core retail sales, which remove large-ticket car sales from the numbers because of their distorting impact on underlying trends, rose by a barnstorming 1%.

Financial markets had been looking for the more-important core number to rise by only 0.4% in July, after a downwardly-revised increase of 0.3% in June, so the 1% outcome is positive for the outlook because it puts the economy on its front foot at the beginning of the third quarter.

"American shoppers are unaware of what the yield curve slope is supposedly telling them about their economic fate. US retail sales continued to boom in July," ays Avery Shenfeld, chief economist at CIBC Capital Markets. "Even department stores were in the mix of winners, while a certain online retailer's sale day gave a lift to that category. The retail news was joined by more modest upside surprises in the Philly Fed and Empire factory indexes."

Markets care about the data because it reflects rising and falling demand in the economy, which is key to the outlook for the consumer price pressures that central banks are attempting to manipulate when they tinker with interest rates.

Changes in rates are normally only made in response to movements in inflation, which is sensitive to growth, but impact currencies because of the push and pull influence they have over capital flows. Those flows tend to move in the direction of the most advantageous or improving returns, with a threat of lower rates normally seeing investors driven out of and deterred away from a currency.

"The consumer, in short, remains in very good shape, starting the third quarter on a very solid note," says Ian Shepherdson, chief economist at Pantheon Macroeconomics. "We see zero evidence that the consumer is being dragged down by the troubles in manufacturing. As consumption accounts for nearly 70% of GDP, this makes us comfortable expecting GDP growth to exceed 2% again."

Above: Pound-Dollar rate rises alongside Dollar Index Thursday, both being boosted by retail sales.

The Dollar index was 0.03% lower at 97.63 after paring earlier losses, but is up 2.03% for 2019. The Dollar was higher against all G10 rivals other than Sterling and the Australian as well as New Zealand Dollars.

"We got what sounded like a formal response from China around the 5amET hour this morning, calling the planned tariffs on $300bln of Chinese goods a violation of accords reached between Presidents Trump and Xi, and that China would take all necessary measures to retaliate. This saw risk assets, including oil prices, go offered once again and helped USDCAD bounce off trend-line support," says Erik Bregar, head of FX strategy at Exchange Bank of Canada.

The Pound-Dollar rate was 0.58% higher at 1.2182 following the release, although the British currency was also boosted by its own retail sales surprise and renewed hope in the market that the opposition in the UK parliament might be able to prevent a 'no deal' Brexit at the end of October.

"We’re not sure we’d get too excited here considering the BOE’s hands are still tied because of Brexit, but the headline and the positive chart development does give a reason for funds to cover some short positions," Bregar says.

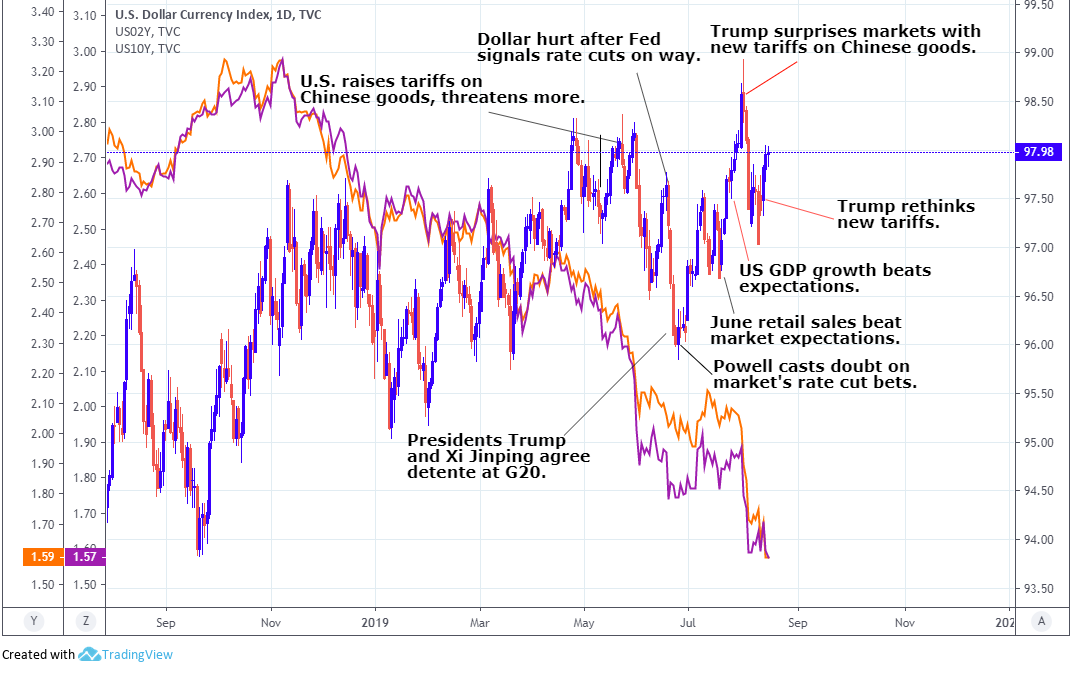

Above: Dollar Index at daily intervals alongside 2-year (purple) and 10-year (orange) bond yields.

Thursday's data and price action comes hard on the heels of a fierce sell-off in risk assets that saw the S&P 500 index post its largest daily decline for 2019, while also hurting stock markets the world over and driving most currencies other than the 'safe-haven' Yen, Swiss Franc and Dollar to intraday losses.

Markets slumped Wednesday after the U.S. yield curve, which represents the cost of government borrowing over maturities that range from one month to 30 years, briefly became downward sloping, in a process known as inversion. This was after the yield on the 10-year government bond fell below that of the two-year bond, which is rare because longer term debts are normally perceived as more risky that short-term ones and so often offer a higher yield.

Inverted yield curves are widely believed to be harbingers of recession further down the line, although the U.S. inversion came in the wake of Chinese industrial production and retail sales figures that suggested the world's largest economy struggled during July. The curve then inverted again during the London morning when the German economy was revealed to have contracted during the recent quarter, for a second time in the last year.

"In our view the signalling effect of an inverted curve is different today to what was the case 10-20 years ago when central banks did not engage in QE (which has now a clear flattening effect). Hence, concerns about imminent global recession may be exaggerated," says James Knightley, chief international economist at ING.

Chinese and German growth is weakening amid the U.S.-China trade war, which has hurt the export side of both economies. China is a significant market for German car manufacturers, but the world's second largest economy has been under relentless pressure from President Donald Trump's trade tariffs.

Chinese firms sell more than $550 bn of goods to American companies and consumers each year but these products are becoming less attractive because around $250 bn of them now incur a 25% tariff charge when they enter the U.S. Most of the other $300 bn of goods not yet subject to a tariff are now due to incur levies between September 01 and December 15, according to a notice published by The Office of the United States Trade Representative this week.

"An inverted yield curve has given false signals in the past on possible US recessions (around the Russia/LTCM crisis in 1998 for example), while other countries have experienced prolonged yield curve inversion in the past without recession – the UK for example through much of the 1990s. As such it is important to emphasise the obvious point there is no inevitability of recession," says ING's Smith. "For now the US economy remains in decent shape and recession is certainly not our base case."

The Federal Reserve (Fed) has already cut the Fed Funds rate once this year, by 25 basis points to 2.25% in July, although the consensus in financial markets is for it to slash U.S. borrowing costs twice more before the year is out. In more ordinary times that would have undermined the Dollar by eating away at the extra yield investors earn by owning the greenback instead of other currencies, but the Dollar has actually strengthened in August.

Rates were cut in July due to fears of what a weak global economy might eventually mean for the U.S., which explains why investors have been reluctant to sell the Dollar and buy other currencies. U.S. interest rates are still the highest in the devloped world and official data released Wednesday showed inflation rising back toward the Fed's 2% target, which could mean the bank finds it difficult to justify many more reductions to U.S. borrowing costs.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement