- Downtrend intact but counter-signals grow

- Potential for break in either direction

- GBP to be driven by GDP data, USD by Non-Manufacturing ISM

The Pound-to-Dollar rate opens the new week at 1.2730, 0.56% higher than at the start of the previous week. Sterling actually managed to outperform the greenback last week despite much volatility centred around a mid-week flash-crash in Asian trade that saw the pair briefly decline to lows of 1.2442.

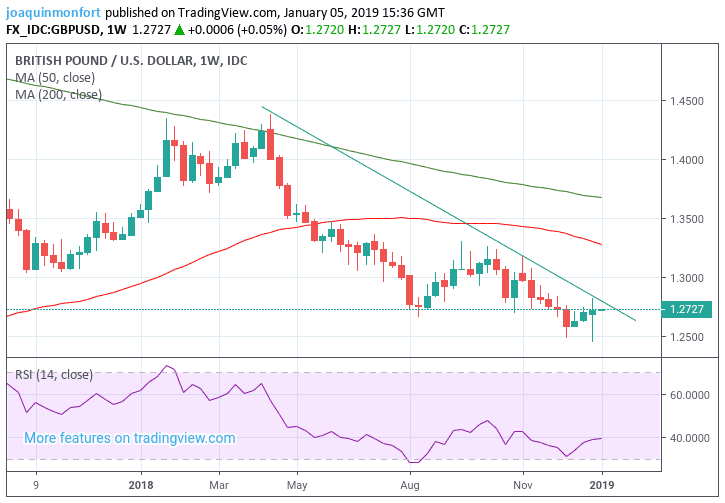

Looking at the week ahead, our technical studies suggest the pair remains caught in a broader technical downtrend, but we are starting to see some signs of bullish potential.

The ambiguous nature of the charts suggests caution is required before taking a conviction view, and there is a strong possibility the pair will actually continue trading at about its current levels, in a more sideways trend between the 1.25s and 1.27s.

The mixed technical signals are shown clearly on the weekly chart (above). The intact downtrend line suggests the bear trend will extend, whilst the Japanese hammer candlestick pattern formed last week is a bullish reversal sign, especially coming as it does at the end of a trend.

Heaping on confusion is the converging RSI momentum indicator in the lower pane. This failed to make a lower low when the market did at the last trough. The non-convergence is a bullish sign.

Whilst we have two bullish indications the trend may be changing the downtrend remains stubbornly intact and we cannot, therefore, confidently predict more upside. At the same time, it would be equally risky to forecast a continuation lower given the converging RSI and the bullish candlestick.

Ultimately the position of the market in relation to the range encompassed by the weekly hammer candlestick formed in the past week is probably the key determining factor.

If the exchange rate can break above last week's highs it will probably signify the ‘last straw’ for the bear trend, and confirm a bull reversal. The high in question is situated at 1.2815, and a break above that would see a continuation up to an initial target at 1.2905, in the coming week.

Alternatively, a break below last week's lows at 1.2442 would result in a continuation down to the next target at 1.2330.

Advertisement

Bank-beating exchange rates. Get up to 3-5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The U.S. Dollar: What to Watch

The U.S. Dollar was buoyed at the end last week by strong U.S. labour market data, which showed the economy employing a further 312k workers in December, well above expectations and the long-run average of around 200k.

The positive employment data continues to suggest underlying strength in the U.S. economy and that fears of a recession are over-egged, yet not all data is equally strong and the overall picture is mixed.

The wide variance in data may well be brought into relief again at the start of the week ahead with the first major release on the calendar, the ISM Non-Manufacturing PMI survey for December, a major sentiment survey for the services sector. It is forecast to dip to 59.1 from 60.7 in the previous month, when it is released on Monday at 16.00 GMT.

The ISM ‘Non-Manufacturing’ survey is the sister survey of the ISM Manufacturing PMI, which has already been released, and showed a considerable decline in December, last week.

The Manufacturing ISM showed growth slowing much more than expected in December to 54.1 from 59.3 in the previous month. This bodes ill for Non-Manufacturing which often follows its lead. A slowdown of a similar degree would be negative for the Dollar.

Another major factor which could move the Dollar is commentary from Federal Reserve (Fed) officials who are responsible for setting interest rates. Fed Chairman Jerome Powell is set to speak on Thursday at 17:00, Bullard at 18.30 and Evans at 19.00.

The trajectory of Federal Reserve interest rates in 2019 is a key focus not just for the Dollar but for the wider markets. Markets have greatly reduced their expectations for further interest rate rises over coming months, based on the observation that economic growth in the U.S. economy is slowing.

The Dollar tends to outperform on the expectations for further rate rises, therefore they dynamic of pricing fewer interest rate rises going forward is, on balance, negative for the currency's outlook.

To what extent will the Fed ease back on raising interest rates? Is the slowing economic activity in the U.S. seen as a mere blip, or a cause for greater concern?

Markets will be seeking answers on the above when the Fed officials speak, and therefore what is said could well prove the highlight for the U.S. Dollar this week.

The Pound: What to Watch

The UK enters a critical three week period as parliamentarians return to Westminster to debate the merits of the Government's withdrawal deal with the EU. A vote is due in the week commencing January 14.

At present, the deal is expected to be voted down by legislators amidst a lack of fresh concessions from the EU. The government is expected to bring the deal back before parliament for a second vote in the event of the first vote failing.

However, any second vote must contain some material changes, so we expect the EU to offer something in the near future as they will know only too well that the deal they worked on over the past 2 years will not pass in its current form.

Sterling will likely trade relatively subdued, range-bound levels until the point it becomes clear that either 1) May's deal will pass or 2) a No Deal Brexit is going to happen in March 2019. We will be watching the newswires for any indications that a decisive shift in either direction has occurred.

The Pound's rise on Friday was in part driven by the release of better-than-expected services sector data, but in the week ahead the focus will be more on the heavier parts of the economy with industrial and manufacturing production data for November scheduled for release, as well as, of course, GDP.

Industrial production is forecast to end a 3- month losing streak in November, when it is released at 10.30 GMT, on Friday, and forecast to show a 0.2% rise. Manufacturing is forecast to show a 0.4% gain when it is released at the same time: these would contrast with -0.6% and -0.9% respectively in October.

Monthly GDP data for November is also out at the same time on Friday and is expected to show a 0.1% rise month-on-month, the same as it did in October, and a 1.3% rise year-on-year.

Despite growth in the UK being weak, it remains about the same as in the Eurozone.

“Despite the Brexit gloom and gridlock in Parliament over the withdrawal deal, the UK economy does not seem to have slowed down anymore than its European counterparts and probably managed growth of 0.1% in November, estimates are anticipated to show.” Says Rafi Boyadjian, an analyst at broker XM.com.

The other key economic release for the Pound is trade balance data, also out on Friday.

Advertisement

Bank-beating exchange rates. Get up to 3-5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here