- GBP/NZD rudderless for now, longer-term Sterling still favoured

- Watch UK wage numbers for guidance on Sterling

- Labour-NZ First budget in focus

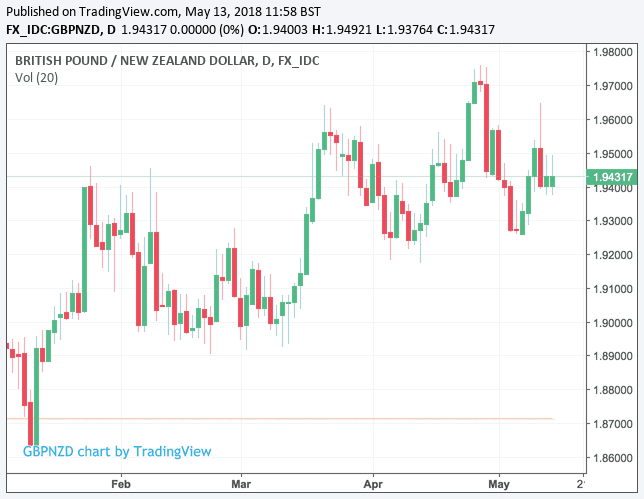

Pound Sterling will open the new week at 1.9431 against the New Zealand Dollar.

While the Pound-to-New Zealand Dollar exchange rate has come off its 2018 highs, just shy of 1.98, we don't see any danger of the exchange rate slipping into a sizeable downtrend at this stage.

But, for now there is a decidedly rudderless feel to this market and our near-term call is more sideways action centred around a fulcrum at 1.94.

Indeed, if pressed, we would say longer-term prospects still favour Sterling.

The New Zealand Dollar is certainly an underperformer if we consider medium-term timeframes - over the course of the past trading month we can see the NZD is the worst-performing major currency.

The currency is therefore subject to downside pressures which, if they were to extend, could afford GBP/NZD some upside.

In 2018, the Pound still holds a 2% gain on the New Zealand Dollar with a 0.8% gain coming during the previous week. If Sterling were to suffer further weakness we would expect some solid bidding interest to come into the market and arrest declines at 1.92.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

NZD: What to Watch this Week

Domestically, for the New Zealand Dollar, the domestic highlight will be the government's budget, the first under the new Labour-NZ First regime, and it should therefore attract much attention.

Economists at New Zealand lender ABS expect a prudent first-up effort from new Minister of Finance, Grant Robertson.

They expect Budget 2018 to show small operating surpluses and a declining net debt profile, mixed with modestly higher spending and investment. They expect net government debt will still fall below 20% of GDP for the 2022 fiscal year, and that any additions to the bond tender programme will be modest i.e. an extra $1 billion in total.

At present, it is hard to predict how the budget might influence currency markets owing to the number of moving parts.

We would therefore simply flag up the potential for volatility in NZD around this time.

GBP: What to Watch

Data is back to the forefront for Pound Sterling now that markets are trading the currency on expectations for future interest rate moves at the Bank of England. Indeed, we saw Sterling come under pressure on Thursday May 10 after the Bank chose not to raise interest rates at their May policy event, despite clear signals over preceeding months that they were likely to do so.

What we do know is that the Bank will only deliver a Sterling-supportive interest rate rise should UK data show signs of a strong recovery from a soft start to the year, and this week's data releases will therefore be key.

Tuesday May 15

Foreign exchange markets will be eyeing labour market statistics for March and April at 09:30 AM B.S.T.

The claimant count for April is forecast to have risen to 7.5K from 11.6K previously, while the unemployment rate is forecast to stay unchanged at 4.2% in March.

The three-month-on-three-month change in employment will be key, but we are yet to see market forecasts for the outcome.

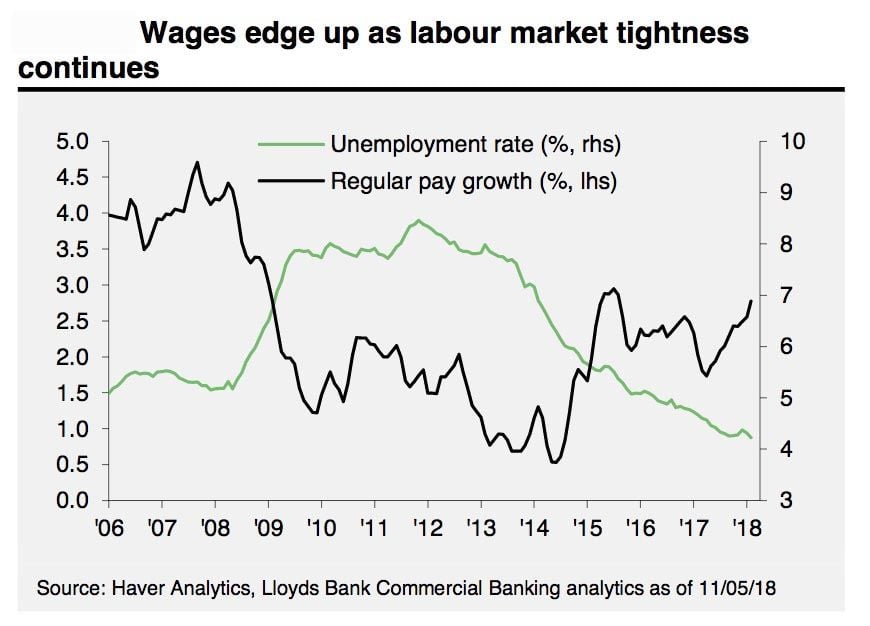

Analysts at Lloyds Bank Commercial Banking are looking for a rise in employment of 150K, saying "the employment gain for the three months to March will provide a measure of the underlying strength of the economy." A rise if 150K "would be a substantive increase for the quarter, consistent with the view that the slowdown in output was most likely temporary."

For Sterling the most important release of the day is however likely to be the wage data - the average earnings index + bonus for March is forecast to have registered growth of 2.6%, down from the previous month's 2.8%.

Should wages beat expectations we would expect Sterling to rally as it suggests there is a real risk of domestically-generated inflationary pressures rising in coming months. Such an observation would likely steer the Bank of England's hand towards delivering an interest rate rise in August.

At 10:00 AM Mark Carney and some of his lieutenants will be under the spotlight when they are questioned by the Treasury Select Committee in Westminster on their current guidance for interest rates and expectations for the UK economy.

Expect some criticism from MPs on the apparent u-turn performed by the Bank of England when they opted to not raise rates in May, despite having dropped some significant hints that such an outcome was likely over preceding months.

The Bank will no doubt point at the data. What could move markets is any strong hint on future rate prospects for the economy, so keep an eye on the newswires.

"The market now assigns a greater-than-even chance that the MPC will be on hold for the rest of the year. We are not so sure, because we look for GDP growth to rebound in coming quarters. We acknowledge the downside risks that Brexit uncertainty imparts to the economic outlook, but we still forecast that the MPC will raise rates 25 bps at the August 2 policy meeting. After that rate hike, we then look for the MPC to remain on hold through the end of the year," say analyst at global investment bank Wells Fargo in their latest assessment on the future of UK interest rates.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.