The New Zealand Dollar is well below what it should be according to fair-value studues, but analysts warn against expecting a recovery anytime soon.

The New Zealand Dollar is relatively 'cheap' according to studies conducted by foreign exchange analysts at UBS, but it is likely to remain that way for the forseeable future as political pressures continue to weigh.

Indeed, analysts at Switzerland's largest bank have lumped the New Zeland Dollar alongside the Pound as being the two currencies that are likely to suffer a politically-inspired risk premium in 2018 as politics trumps economic fundamentals in driving value.

Estimating a 'fair-value' for a currency by determining where it should be based on all the known variables that impact its value, and then comparing that to its actual market value, can help analysts determine the direction in which the exchange rate will go next.

If the estimate varies markedly from the market, it is assumed the market will move steadily towards the estimate, know as 'fair-value' over time.

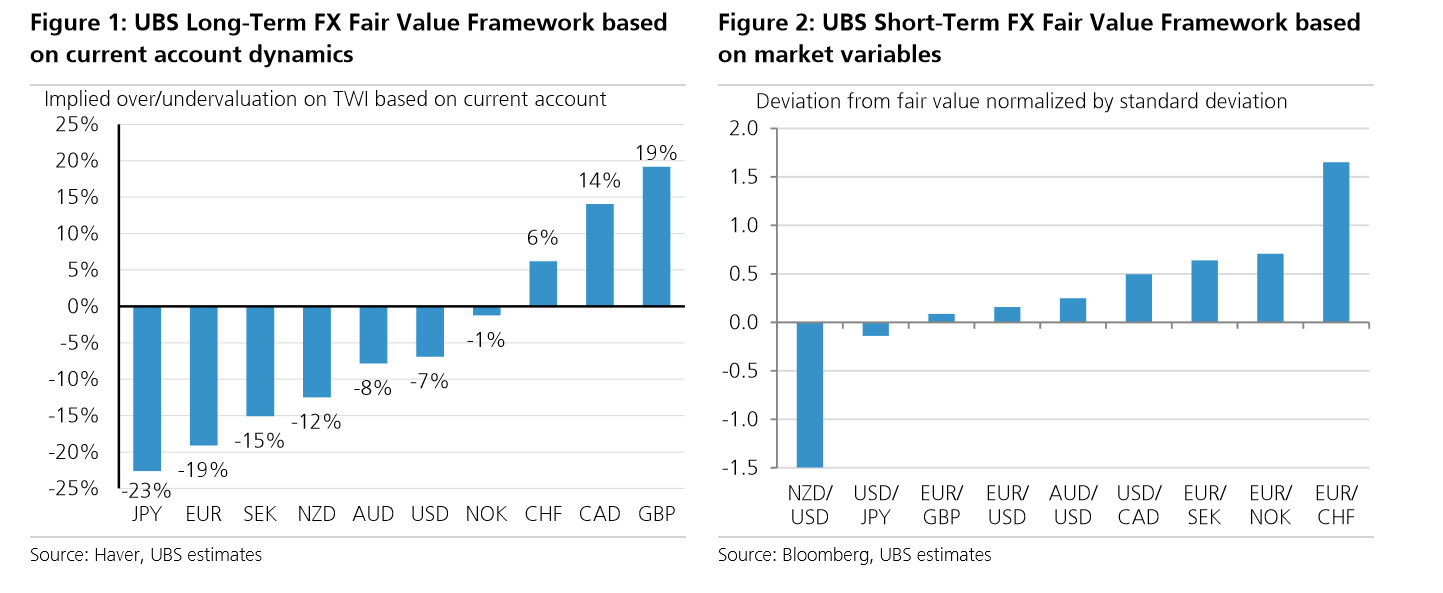

UBS find that both its long-term and short-term estimates of fair-value for the New Zealand Dollar (against a trade -weighted basket of other currencies) are above its current market value.

The long-term fair-value estimate is 12.0% higher than the actual market value; and the short-term estimate shows NZD/USD undervalued by -1.5 standard deviations from its mean.

Based on this disparity, UBS conclude that the Kiwi is 'cheap' or undervalued.

In normal circumstances the inference would then be that NZD would be expected to rise back towards its fair-value.

However, in this particular case UBS do not take that stance and expect NZD to remain under pressure instead.

The reason why is that they see political uncertainty linked to the recent general election as keeping the market level of the currency supressed below its fair value.

"In theory, the currencies of commodity exporters with solid fundamentals and higher interest rates than the rest of the world should perform well in a solid global growth environment," says UBS Strategist Lefteris Farmakis .

"Nonetheless, NZD has been held back by rising political uncertainty following the formation of the new government after recent general elections," he adds.

The market has focused on two main sources of political risk which are unlikely to go away any time soon.

The first one relates to the Reserve Bank of New Zealand (RBNZ) procedures for decision-making on altering interest rates which is a big driver for the Kiwi.

The new government wants to make it part of the RBNZ's mandate to strive for full-employment in its decision making, when previously it only had to be concerned about inflation.

A further change is the introduction of a rate-setting committee to vote on the final decision, where now only the governor decides.

All-in-all these changes are expected to keep downwards pressure on the Kiwi.

"On their own, these changes are not novel or unprecedented and in fact they may not amount to much in terms of policy.

Markets, however, may continue to worry about the preservation of the central bank's independence," says the UBS analyst.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

The other major political factor weighing on the Kiwi comes from the the cut to immigration, which could cause a 'supply-shock' due to a sudden fall in the available workers, a reduction in output and growth.

The consequences for inflation are unclears, acording to Farmakis as, on the one hand it might increase due to the reduction in the pool of avaiable jobseekers from lower migration, whilst on the other hand, for the same reason there would be less demand for goods and services, which could force prices lower.

Currently NZD has been supported by realtively high interest rates of 1.75% which has always kept inflows of foreign capital reasonably bouyant, however, if rates were cut much lower those flows would be in danger of drying up, and demand for the Kiwi with them.

"Ultimately this amounts to a negative shock for real rates and could reduce the positive rate gap that has supported NZD during the past decade," siad Farmakis.

ANZ's Uerata Reaches Similar Conclusion

Reaching the same conclusion as UBS but for different reasons, is ANZ analyst Kyle Uerata, who actually sees political risks relating to the RBNZ's mandate and decision making process as a neutral consideration, whilst weaker economic growth as the main protagonist of the weaker New Zealand Dollar.

He argues that the RBNZ already take into account the labour market in their decision-making in so far as how it relates to the amount of 'slack' there is in the economy.

When unemployment is high there is said to be too much 'slack' and the central bank usually lowers interst rates to promote growth and get people back to work.

When unemployment is low, the RBNZ rasies interst rates because more poeple are earning and spending, and this tends to push up inflation.

At the current time the unemployement level is close to a point called NAIRU which is a theoretical point at which unemployment gets so low it starts to have an upward impact on inflation.

Given its other mandate is to keep a cap on inflation it must view unemployment as at an ideal level (4.6%) and therefore the new mandate will probably not impact on its decisions in the short-term.

Uerata also dismisses the impact of committee decision making, arguing that the decision will still be based on a non-discretionary model using the same 'inputs' as are used now - by which he means economic variables - and so whether it is the governor himself or a group deciding, the result will probably be the same.

The final change the government wants to make is to the inflation target, replacing the current 'hard' 2.0% target with a softer 1.0% -3.0% range.

ANZ note that in the past when it had a range - before it set the 2.0% target - it would regularly allow inflation to extend higher before rasing interst rates compared to when it had the hard target.

This suggests it could allow interst rates to stay lower for longer, and is a reason for expecting a cheaper Kiwi as a result of the policy changes.

But it is Uerata's analaysis of failing growth which is the main driver for the lower NZD forecast.

"We are less optimistic on the outlook for growth than the RBNZ, and see housing market softness persisting. But we also acknowledge rising risks of more cost-push inflation from the labour market," concludes the analyst.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.