- GBP/NZD rises in wake of NZ inflation

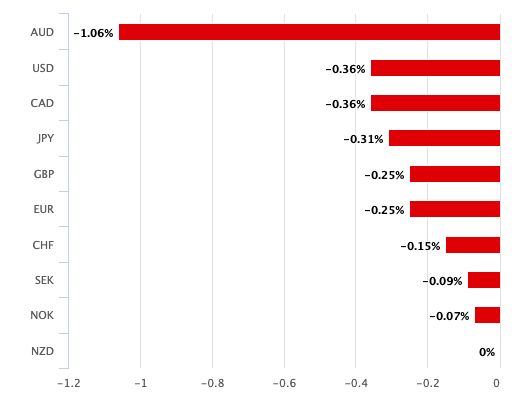

- NZD is weaker across the board

- Inflation undershoots RBNZ forecasts

- Lowering bets for 75bp hike in Feb.

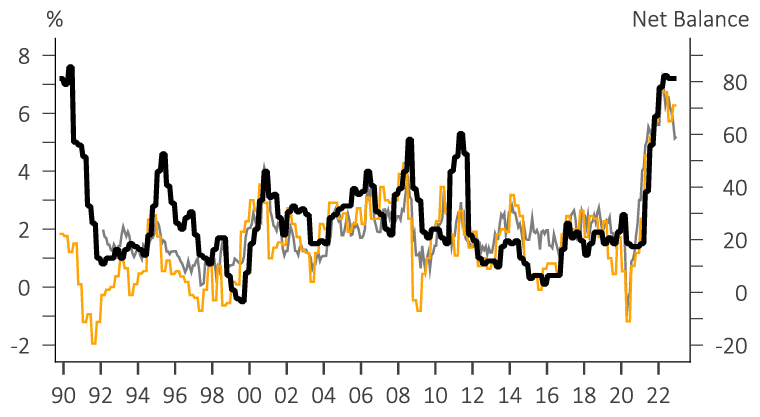

Above: NZ CPI inflation and pricing intentions. (CPI in black, % + Avge. selling prices net balance for next 3M from QSBO in yellow + pricing intentions from ANZBO in grey, also RHS. Image: ASB.

The New Zealand Dollar traded at the bottom of the G10 pack midweek after local inflation figures revealed little reason for the Reserve Bank of New Zealand (RBNZ) to pursue further aggressive interest rate hikes.

The New Zealand currency ceded a percent of its value to the Australian Dollar and was a quarter of a percent lower against the Pound and U.S. Dollar after StatsNZ said inflation read at 7.2% in the year to the final quarter of 2022.

This is unchanged on the previous quarter but a touch higher than analyst forecasts for 7.1%.

It was nevertheless lower than the level the RBNZ had expected in its most recent set of forecasts, questioning whether the central bank needs to proceed with a 75 basis point hike at its next meeting.

"The Australian and NZ inflation data both came out above investor expectations, but engendered different markets reactions. The reason for these different reactions were the outcomes relative to central bank expectations. NZ’s headline inflation data looks as though it has plateaued at a bit above 7.0% vs RBNZ expectations for a plateau at 7.5%," says Valentin Marinov, Head of G10 FX StrategyCrédit Agricole.

For the New Zealand Dollar, this is a soft development.

"The RBNZ’s hawkish rhetoric from its November MPS suggested the central bank would consider a super-sized rate hike of 75bp at its February meeting. NZ inflation peaking below the central bank’s forecast makes this unlikely and is weighing on the NZD as the market pares back its expectations for the February meeting," he adds.

The Pound to New Zealand Dollar exchange rate rose a quarter of a percent to 1.90 in the hours following the release, nudging bank transfer rates to around 1.8450, cash and holiday money rates at competitive providers to around 1.8830 and rates at competitive payment providers to around 1.8940.

The Kiwi was lower against the U.S. Dollar at 0.6483 and was down 1.10% against the Australian Dollar at 1.0940.

"Widespread NZD falls, a close to 10bp fall in the NZ swap yield and a trimming of OCR rate hike expectations – suggest that the market thinks the RBNZ will pare back the 125bps of rate hikes it had signalled for the next few months and join other global central banks in cutting rates before the end of this year," says Mark Smith, Senior Economist at ASB.

Markets and analysts are in the process of lowering their expectations for future RBNZ action following the inflation data.

"We have revised down our forecast for Official Cash Rate hikes from the RBNZ. We now expect a 50 bp rise in the OCR at the February policy meeting previously we expected a 75 bp rise)," says Michael Gordon, Acting Chief Economist at Wetpac.

Westpac continues to expect another 50bp increase in April, but that will be dependent on the strength of economic conditions.

"Inflation pressures have remained strong. However, the acceleration in inflation that the central bank was forecasting has not eventuated," says Gordon.

However, analysis from Kiwi lender ASB finds the central bank might still have reason to pursue a strident policy of rate hikes.

"There is still a large bow wave of inflationary pressure in place, with widespread price increases and very high rates of core and non-tradable inflation evident," says Mark Smith, Senior Economist at ASB.

Smith says the market appears to be anticipating the RBNZ will be inclined to start cutting interest rates later in 2023 as the economy slows and inflation falls.

But ASB tells clients that although downside risks to the medium-term inflation outlook have grown, "the RBNZ must press forward with OCR hikes for now. OCR cuts still look a long way off."

"The problem facing the RBNZ at present is that annual inflation has remained stubbornly high, with increasingly widespread price increases evident and with domestic pricing pressures pronounced. This suggests that the RBNZ should not declare victory on inflation just yet and will push ahead with OCR hikes," says Smith.

ASB continues to expect a 75bp hike in February but acknowledges the risk of a more moderate pace of RBNZ hikes (including 50bp in February).

Economists at ANZ bank have meanwhile revised their RBNZ call on the back of today's CPI data and weaker activity indicators.

They now expect a 50bp hike in February and two 25bp follow-up hikes taking the OCR to a peak of 5.25%.

"Inflation is clearly still far too strong, but the stabilisation in non-tradables inflation is a welcome development. The inflation numbers clearly weren’t as bad as the RBNZ feared in November, and signs that inflation will ease meaningfully over 2023 are becoming increasingly clear," says Finn Robinson, an economist at ANZ.