- TRY struggles after torrid week for risk currencies

- But remains undisputed global champion on yield

- Said to be an attractive 'carry trade' for the brave

- As all eyes turn to September's CBRT rate decision

Image © Adobe Images

- GBP/TRY reference rates at publication:

- Spot: 11.87

- Bank transfers (indicative guide): 11.46-11.54

- Money transfer specialist rates (indicative): 11.76-11.80

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

Turkey’s Lira was close to the bottom of the currency league table on Friday and at the tailend of an almost torrid week for risky currencies, although it’s outbidding all others with its yield offering to international investors and Credit Agricole has flagged it as the number one ‘carry trade’ out there.

The Turkish Lira fell heavily against all of its ten most frequently traded emerging market counterparts during the week to Friday, a period in which the U.S. Dollar advanced strongly against all contenders except for the Indian Rupee, Russian Rouble and Indonesian Rupiah.

Global stock markets were lower and oil prices had risen sharply, which is always a toxic cocktail for currencies of large net-oil importing countries like Turkey and may explain why other more favourable developments went overlooked by the market during the period.

Had it not been for Dollar strength and international risk aversion then Wednesday’s budget balance figures might otherwise have proven to be a boon for the Lira after Turkey’s Undersecretariat of Treasury announced a primary surplus of TRY 54.49BN for August.

This record high surplus was achieved despite a 31.6% increase in spending during the period, and was thanks to tax receipts that rose further and faster than spending; by some 35% overall.

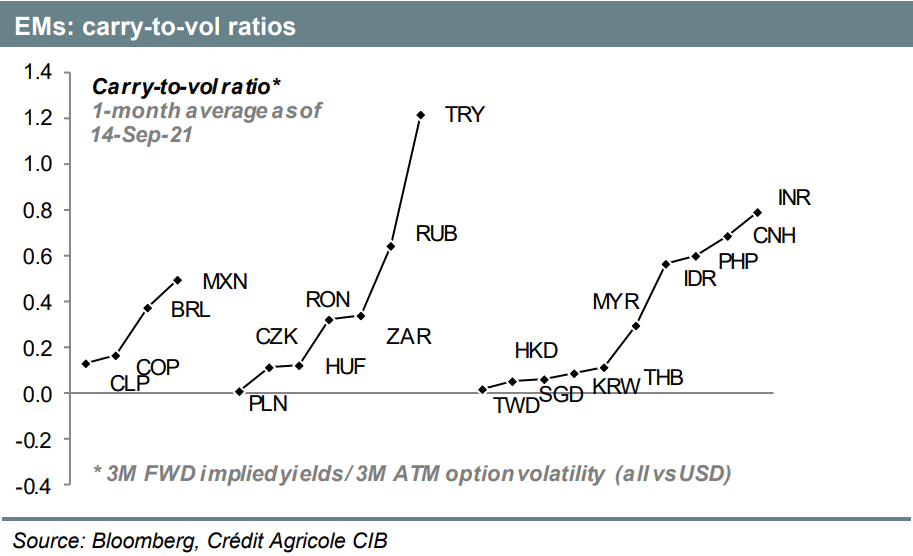

“The carry of the TRY is one of the highest in EMs. With the policy rate at 19.0%, interest rates fly way above other EM high-yielders, such as the RUB, INR and MXN. Combined with relatively low FX volatility, this makes the TRY stand out,” says Sebastien Barbe, a strategist at Credit Agricole.

Above: Credit Agricole graph ranking emerging market currencies in order of their relative yield appeal.

Barbe and colleagues cited the Lira’s carry-to-volatility ratio for rating it as an attractive income prospect for clients of the bank who have high enough levels of risk tolerance.

The ratio uses expected levels of currency volatility derived from options market pricing to qualitatively rank currencies’s yield offerings in a more accurate manner, as currency volatility can easily eat into the interest returns paid by sovereign and corporate bonds.

On this measure at least, Turkey’s Lira is the undisputed champion of the world due to both the Central Bank of the Republic of Turkey’s (CBRT) 19% cash rate and comparatively low levels of currency volatility realised and expected by the market during recent months.

“That is why we believe it is an interesting carry trade, but only one for the brave. The risk would be a large rate cut too quickly,” Barbe says. “On top of it, there have been a couple of favourable improvements in terms of the balance of payments, of late.”

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

But attractive interest return are not the only factor that has been supportive of the Lira lately either, as the CBRT’s FX reserves also grew from $49BN in May to $78BN in August after the central bank has signed currency swap agreements with the Peoples’ Bank of China and Bank of Korea.

The CBRT has also surprised its doubters under new Governor Şahap Kavcıoğlu by keeping the cash rate steady at 19%, although there are risks that this could be reduced sooner than financial markets have anticipated, which many analysts say would be negative for the currency.

Barbe’s assessment and this week’s budget data came just days out from next Thursday’s CBRT interest rate decision and this is even more so than usual a landmark event for the Turkish Lira and economy.

“The lira eked out small gains vs the USD following the CBRT's decision to raise the foreign currency reserve requirement ratio by 2pp to 23% for deposits of less than a year and 17% for those over a year. A surprise rate cut by the CBRT next week could cause sentiment to turn sour,” warns ,” says Kenneth Broux, a currency strategist at Societe Generale.

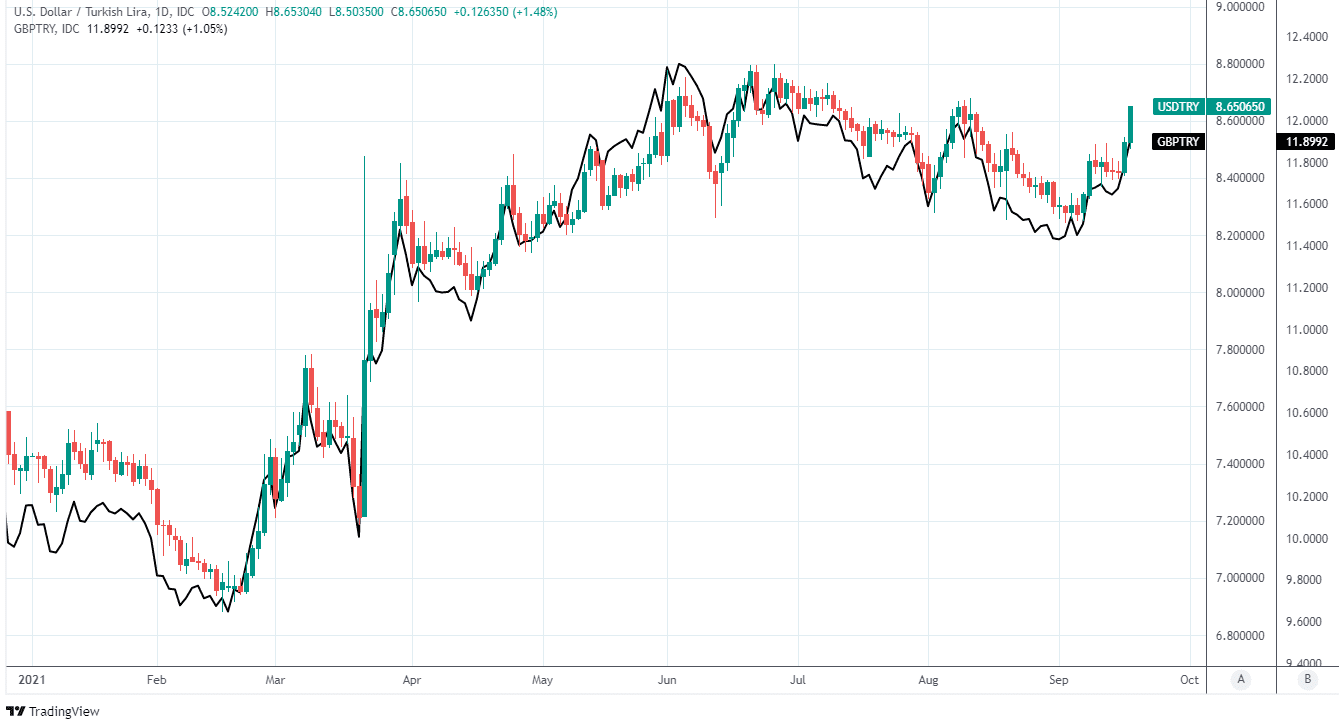

Above: USD/TRY shown at daily intervals alongside GBP/TRY.

Every central bank event is always important for a currency and its related financial markets but even more so with the Lira after the damaging cycle of apparent political intervention at the central bank in pursuit of lower interest rates seen in recent years, which has prompted repeated bouts of sharp currency depreciation and lifted inflation rates further than desired by the CBRT.

The latest sell-off was in March and came in response to Ankara’s dismissal of current Governor Şahap Kavcıoğlu’s predecessor, which led markets to fear that the bank would quickly embark on a renewed cycle of interest rate cuts before the nascent inflation surge in Turkey has been contained.

So far the bank has maintained a steady hand but the currency market will inevitably wait with baited breath next week to hear if that approach will continue, while some observers may have been discouraged from such expectations by indications that the inflation targeting strategy could change.

“Turkish Central bank Governor Sahap Kavcioglu indicated that core inflation, rather than headline, could gain importance as the CBRT sets monetary policy,” says Mathias Van der Jeugt, head of research at KBC Markets in Brussels.

“Until recently, the CBTR governor indicated that the bank intended to keep the policy rate above the inflation rate. August CPI data published on Friday printed at 19.25% Y/Y for headline CPI, but core CPI eased from 17.25% to 16.76%,” Van der Jeugt wrote in an early September note.